ML Evaluation Infrastructure for Fraud Detection

Ugo Chukwu

IOS Risk Eval Harness

ML Evaluation Infrastructure for Fraud Detection

Domain: Fintech / Risk Intelligence

Stack: Python, scikit-learn, XGBoost, imbalanced-learn, Pandas, NumPy

Duration: 7 days

Result: 21% improvement in fraud detection performance across three model architectures

The Problem

Credit card fraud detection sounds simple until you look at the data.

In a real-world dataset of 284,807 transactions, only 492 are fraud. That is 0.17%. A model that predicts "not fraud" for every single transaction would be correct 99.83% of the time — and completely useless.

This is the class imbalance problem, and it breaks every standard machine learning metric. Accuracy tells you nothing. You need precision, recall, F1, average precision, and threshold analysis to understand whether your model is actually working.

Most fraud detection projects jump straight to building models. This project started differently: build the measurement infrastructure first.

The Approach

Phase 1 — Build the Evaluation Harness

Before training a single model, I built

metrics.py — a reusable evaluation module with three functions:compute_core_metrics(y_true, y_pred, y_prob)

compute_core_metrics(y_true, y_pred, y_prob)Calculates every relevant metric from the confusion matrix up:

Precision, Recall, F1, and FPR from raw TP/TN/FP/FN counts

ROC AUC and Average Precision from probability scores

Zero-division guards throughout for production safety

evaluate_threshold_range(y_true, y_prob)

evaluate_threshold_range(y_true, y_prob)Sweeps thresholds from 0.0 to 1.0 in 0.05 steps and returns a full DataFrame showing how precision and recall trade off at every cut point. This is how you make an informed threshold decision instead of defaulting to 0.5.

find_optimal_threshold(y_true, y_prob, metric='f1')

find_optimal_threshold(y_true, y_prob, metric='f1')Automatically selects the threshold that maximises a given metric. It is parameterised, so it can optimise for F1, recall, or any other metric in the output dictionary.

Why build this first: Every model trained in this project, and every model trained in future projects, runs through the same evaluation functions. Results are comparable by design.

Phase 2 — Data Pipeline

Built

data_loader.py with a single function, load_and_prepare_data(), that handles:Dropping the

Time column (a recording artifact, not a transaction property)StandardScaler on the

Amount column to match the scale of PCA-transformed features V1–V28Stratified train/test split to preserve the 0.17% fraud ratio in both sets

Returning clean NumPy arrays ready for any scikit-learn compatible model

Critical detail: scaling happens after splitting. Fitting the scaler on the full dataset before splitting would leak test set information into the training process.

Phase 3 — Three Models, Increasing Sophistication

Model 1 — Logistic Regression (Baseline)

A simple linear model with

class_weight='balanced'. This establishes the performance floor. Every subsequent model must beat it.Model 2 — SMOTE + Random Forest

SMOTE (Synthetic Minority Oversampling Technique) generates synthetic fraud examples by interpolating between real fraud cases. This balances the training set from 394 fraud vs 227,451 legitimate transactions to 227,451 vs 227,451. A Random Forest was then trained on this balanced dataset with 100 trees and

max_depth=10.Model 3 — XGBoost

A sequential boosting model where each tree corrects the errors of the previous one. It uses

scale_pos_weight=577 (the legit-to-fraud ratio) instead of SMOTE, handling imbalance natively. Configuration: 200 trees, max_depth=6, learning_rate=0.1.The Results

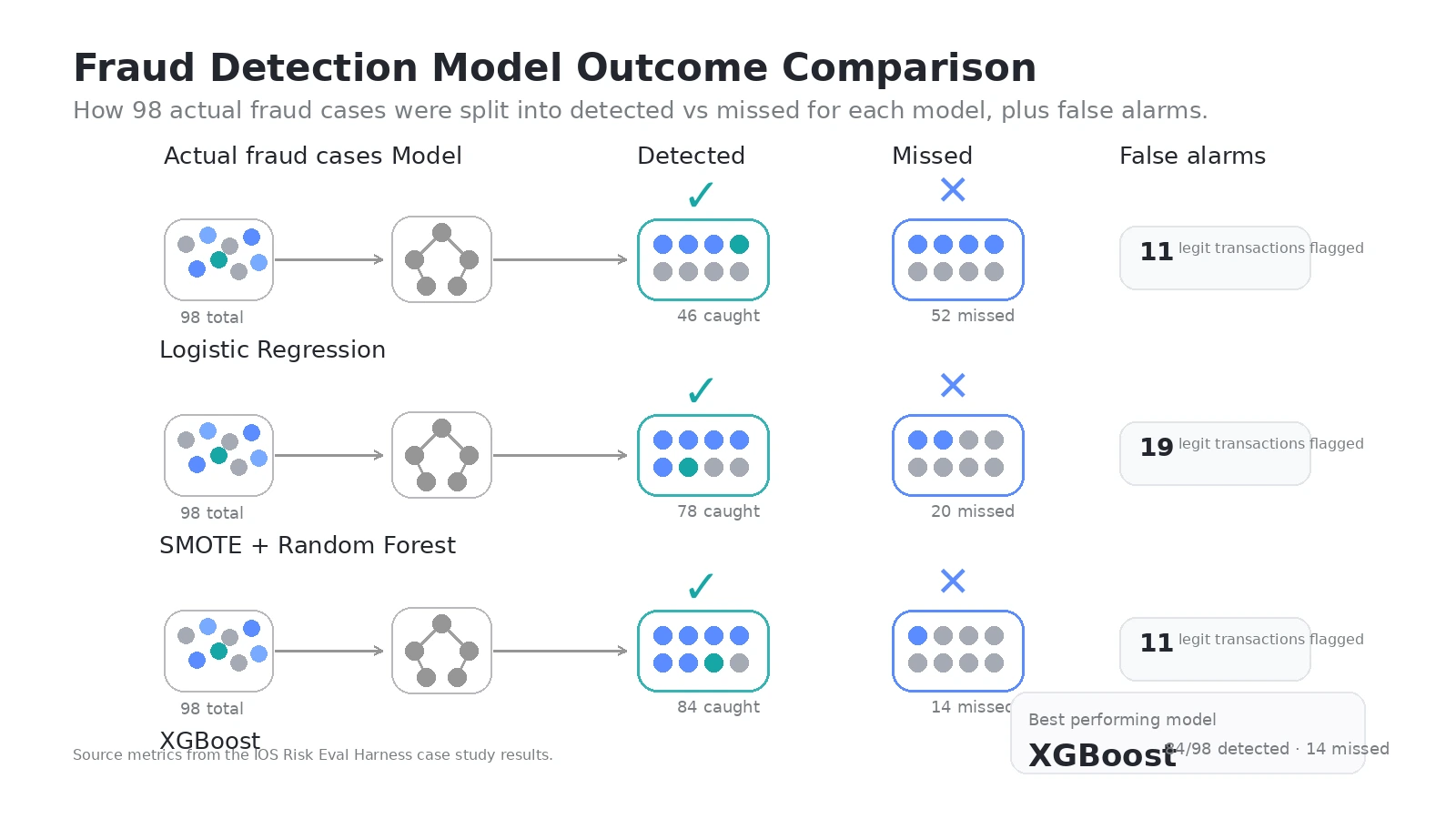

What These Numbers Mean in Practice

Across 56,962 test transactions, including 98 actual fraud cases:

Metric Logistic Regression Random Forest XGBoost Fraud caught 46/98 78/98 84/98 Fraud missed 52 20 14 False alarms 11 19 11 Avg Precision 0.716 0.829 0.869

XGBoost catches 84 out of 98 fraud cases while raising only 11 false alarms. That is 85.7% of all fraud detected, with a false positive rate of 0.019% — less than 2 in every 10,000 legitimate transactions flagged incorrectly.

The baseline Logistic Regression missed 52 fraud cases. XGBoost missed 14. That is 38 additional fraud cases caught — each one representing real financial loss prevented.

Key Engineering Decisions

Evaluation-first architecture

The evaluation harness was built before any model. This is the correct order: you cannot improve what you cannot measure, and you cannot trust improvement claims without consistent measurement.

Threshold as a business decision

The optimal threshold varies by model (

1.00 for Logistic Regression, 0.85 for Random Forest, 0.35 for XGBoost) and by business priority.A bank prioritising fraud prevention optimises for recall

A bank prioritising customer experience optimises for precision

The

find_optimal_threshold() function supports both by parameterising the target metric.Reproducibility by design

Every random operation uses

random_state=42. The stratified split preserves class ratios. The same data pipeline runs identically every time. Results are reproducible without notebooks or manual steps.Production-safe code patterns

Zero-division guards on every metric calculation

Python-native float and int casting before logging to avoid NumPy serialisation bugs

Modular functions with explicit type signatures

What This Enables

This evaluation harness is domain-agnostic. The same

metrics.py and data_loader.py pattern applies to:Insurance claim fraud

Anti-money laundering transaction monitoring

Credit underwriting risk scoring

Any imbalanced binary classification problem in fintech

The infrastructure built here is the measurement layer that every subsequent model, agent, or system gets evaluated against.

Services Available

ML Evaluation Framework Design — build measurement infrastructure before models

Fraud Detection System Development — end-to-end pipeline from raw data to evaluated model

Imbalanced Classification — SMOTE, threshold tuning, cost-sensitive evaluation

Model Comparison & Selection — systematic benchmarking across model families

Production-Ready ML Code — clean, documented, reproducible Python

Built as Project 01 of IntelligenceOS — a 12-project AI platform build across 12 months.

Like this project

Posted Mar 25, 2026

Developed ML evaluation infrastructure for improved fraud detection in fintech, boosting model performance by 21%.

Likes

0

Views

7

Timeline

Mar 15, 2026 - Mar 22, 2026