its-Adarsh2003/Portfolio-Optimizer

Adarsh Dubey

Portfolio Optimization

This project demonstrates Modern Portfolio Theory in Python. Using historical stock data, it calculates expected returns, volatility, and the covariance matrix of assets to construct the efficient frontier and find the optimal allocation of assets."

🔧 Tools & Libraries

Python 3.x

Pandas, NumPy

Matplotlib, Seaborn

SciPy Optimizer / PyPortfolioOpt

🚀 Features

Import and process historical stock data

Calculate daily & annual returns

Compute risk, volatility, and Sharpe Ratio

Construct the Efficient Frontier

Identify the optimal portfolio weights

Visualize results with clear charts

📊 Example Outputs

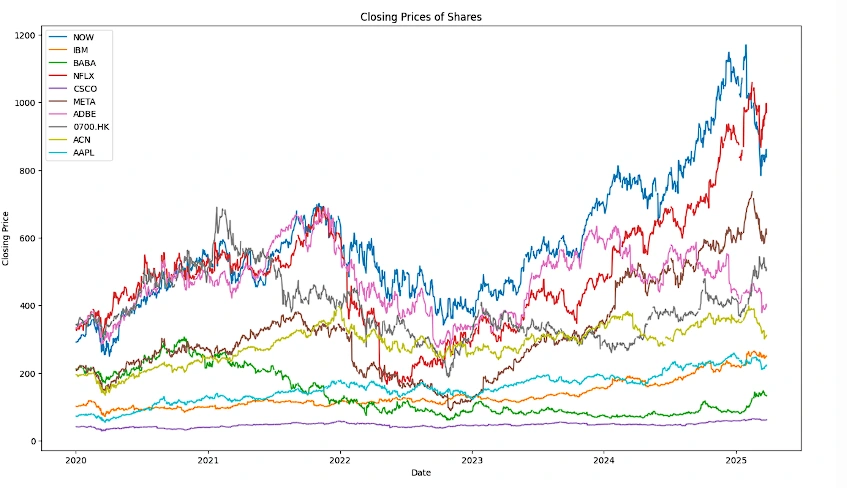

Closing Prices of Stocks

Portfolio Weights Distribution

This bar chart displays the optimal percentage allocation of each stock in the portfolio. These weights are determined by the optimizer to achieve the best balance between risk and return.

Distributed stocks

This visualization shows how different stocks are distributed across the portfolio. By analyzing the spread of stocks, investors can understand diversification and exposure to different assets. A well-distributed portfolio reduces risk by avoiding over-concentration in a single stock.

Like this project

Posted Sep 2, 2025

Contribute to its-Adarsh2003/Portfolio-Optimizer development by creating an account on GitHub.

Likes

0

Views

3

Timeline

Feb 23, 2025 - Apr 2, 2025

Clients

Personal Project