Supply Chain Evaluation

Harsh Modi

This project compares the supply chains of the cement and pharmaceutical industries, focusing on key metrics such as Days in Raw Material (DRM), Work in Progress (DWIP), and Finished Goods (DFG). It also examines cost breakdowns, productivity, and the handling of payables and receivables. The analysis highlights significant differences between the two industries in terms of supply chain efficiency and cost management.

Key Findings

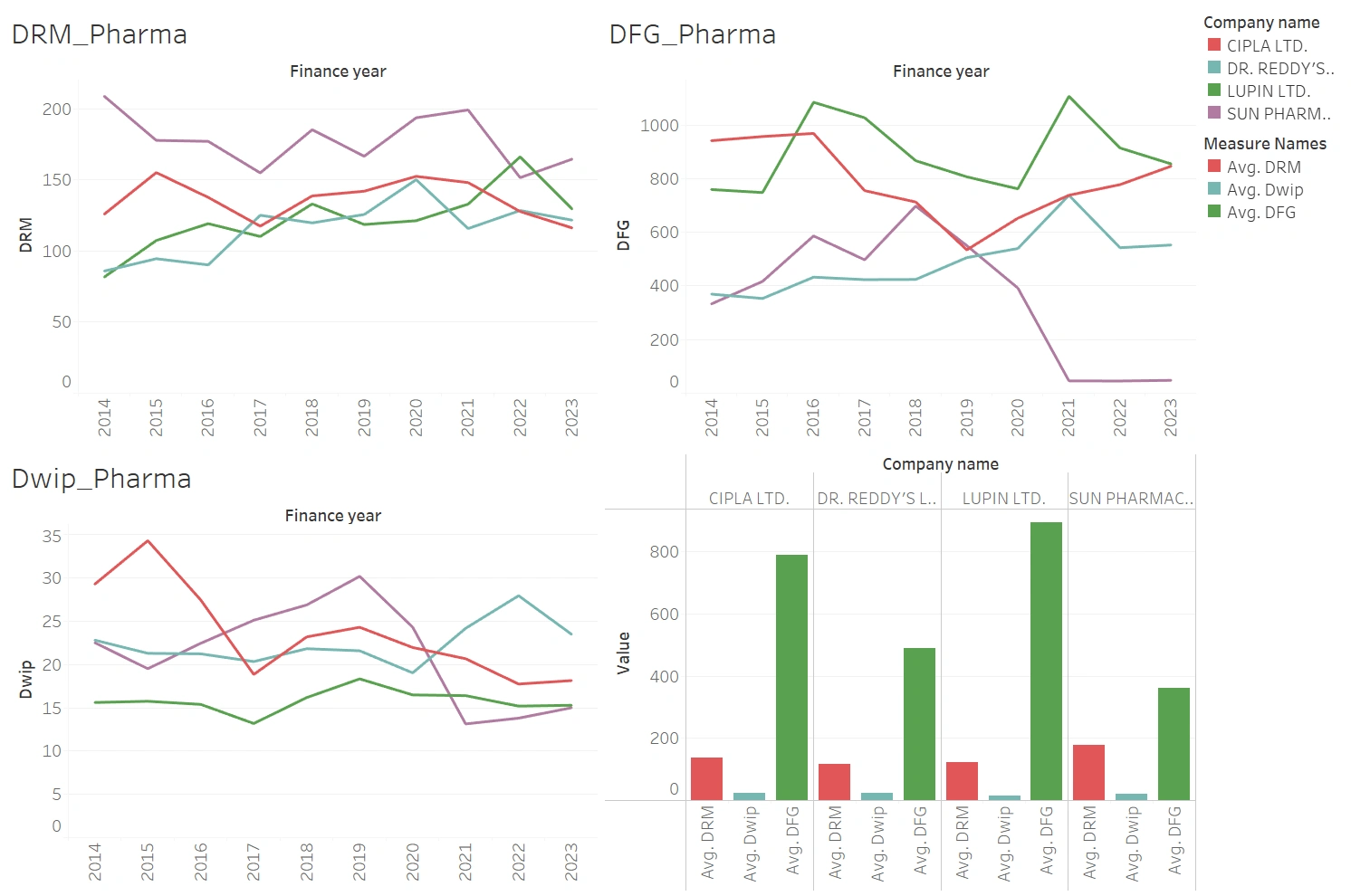

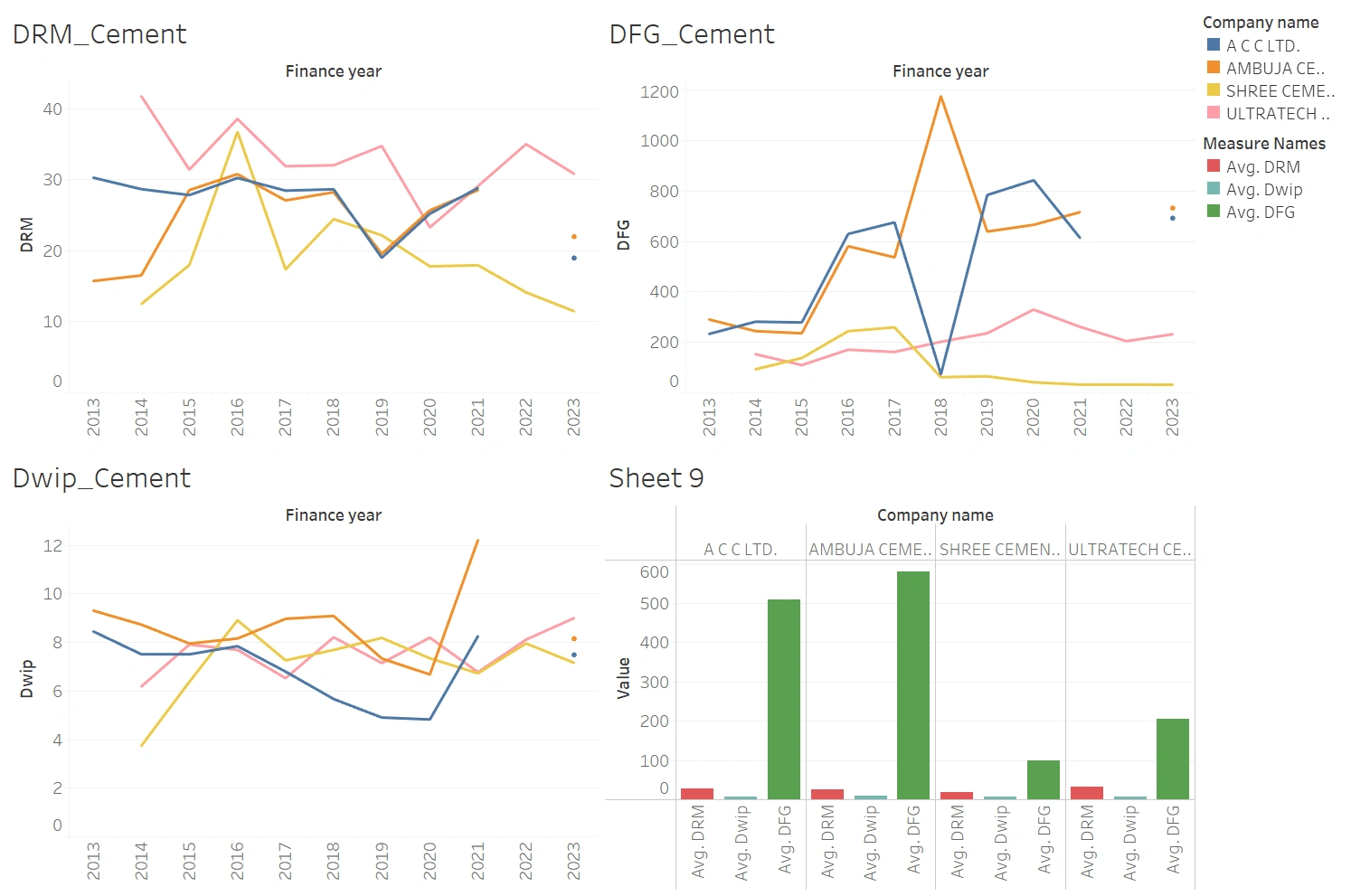

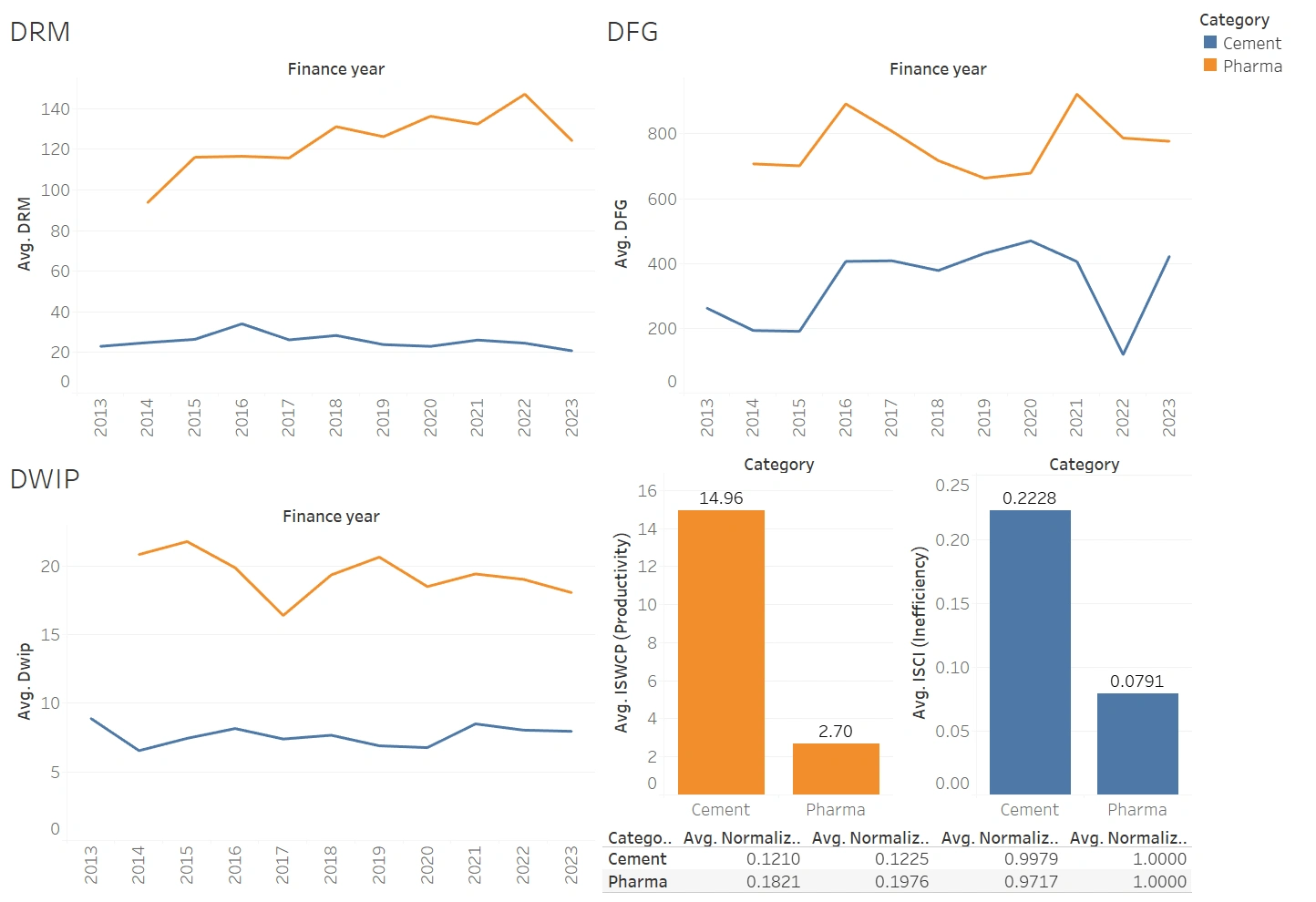

Days in Raw Material (DRM), Work in Progress (DWIP), and Finished Goods (DFG):

Cement Industry:

Lower DRM due to locally sourced raw materials.

Shorter DWIP due to simpler production processes.

Lower DFG due to quick dispatch to meet constant construction demand.

Pharma Industry:

Higher DRM due to global supply chains and regulatory delays.

Higher DWIP due to rigorous testing and multi-stage production.

Higher DFG due to stringent quality standards before release.

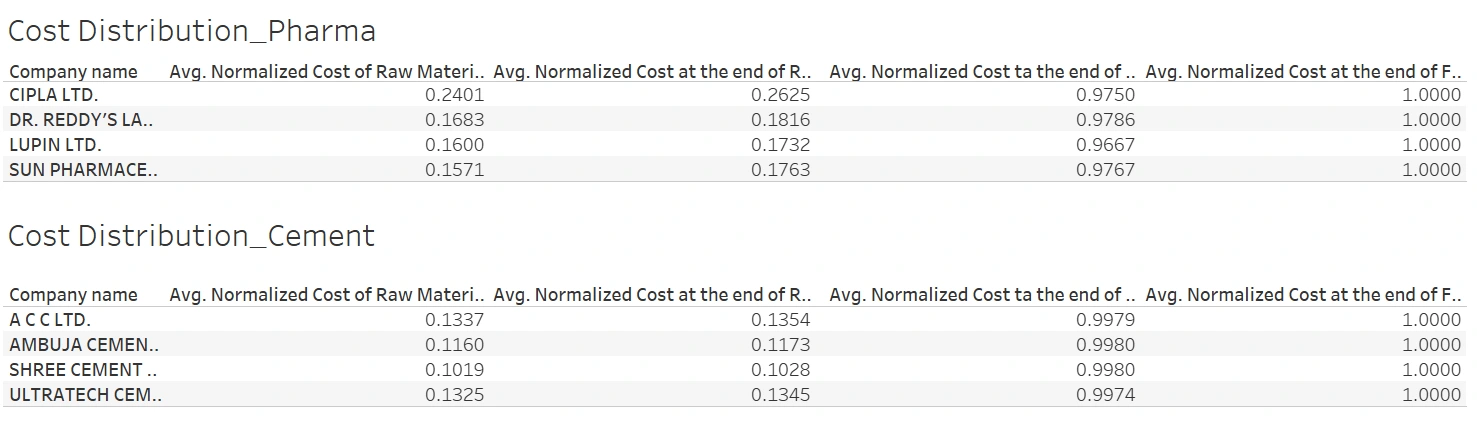

Cost Breakdown and Productivity:

Cement: Lower costs in raw materials (12%) and production processes, with no post-manufacturing costs.

Pharma: Higher costs in raw materials (18%) and production processes, with additional post-manufacturing costs due to regulatory compliance and surveillance.

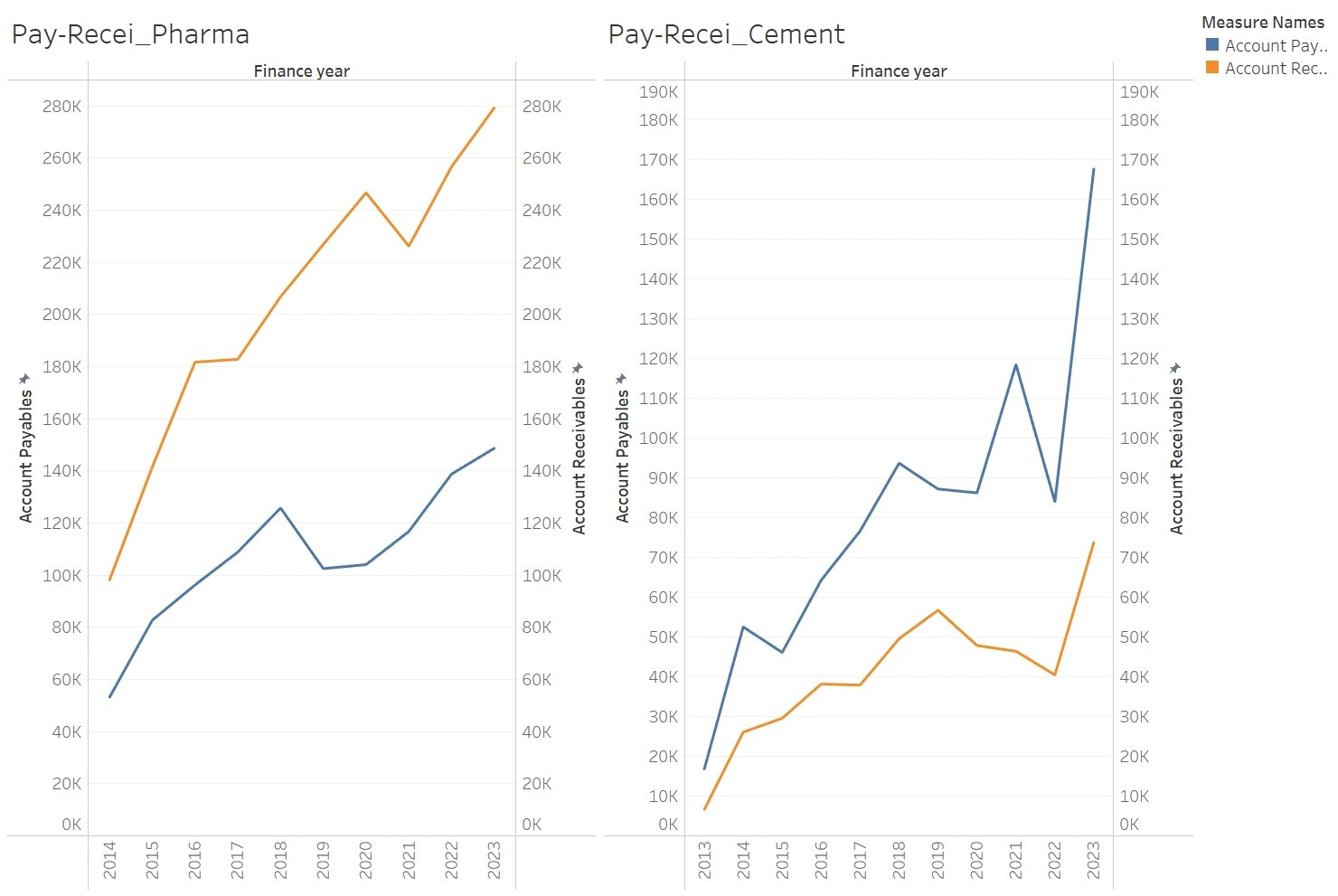

Payables vs. Receivables:

Pharma: Receivables exceed payables, leading to slower customer collection cycles.

Cement: Payables exceed receivables, allowing for leveraging supplier credit and faster product turnover.

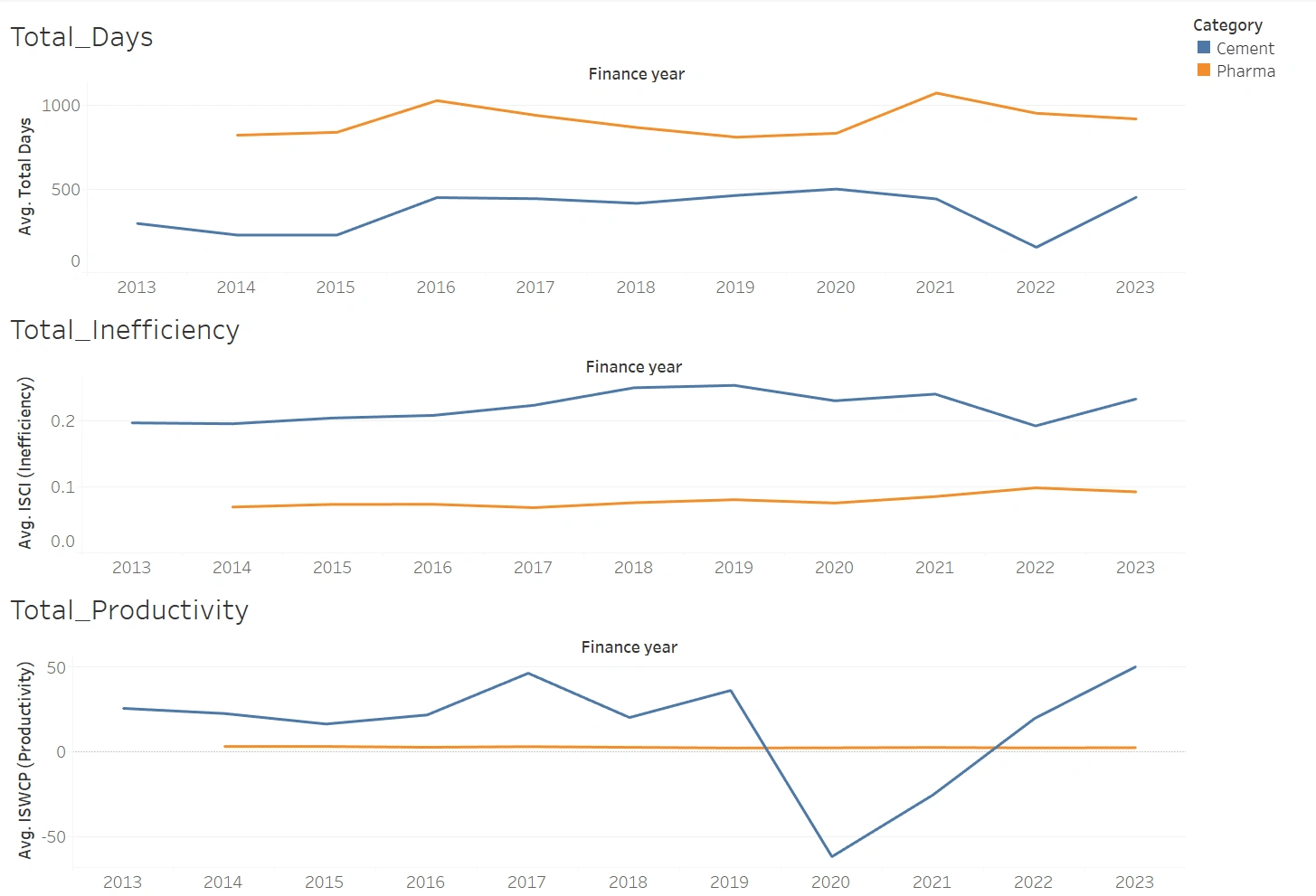

Industry Conclusions:

Total Supply Chain Length: Cement shows a decreasing trend post-2021, while pharma maintains a consistently higher length due to complex global sourcing and regulatory processes.

Supply Chain Inefficiency: Cement's inefficiency is increasing despite a shorter supply chain, while pharma maintains stable inefficiency levels.

Working Capital Productivity: Cement shows variability with a strong recovery post-2021, while pharma remains stable but could improve working capital utilization.

Company-Level Analysis:

Pharma: Sun Pharma demonstrates the most efficient supply chain management, while Cipla and Dr. Reddy’s have room for improvement. Lupin is showing steady improvement.

Cement: UltraTech Cement is the market leader in efficiency, with recent improvements. Ambuja Cements shows superior efficiency, while ACC and Shree Cement need to focus on reducing DFG.

Recommendations

For the Pharma Industry:

Reduce DRM: Diversify suppliers and explore near-shoring strategies to mitigate global supply chain risks.

Minimize DWIP and DFG: Adopt lean inventory practices and just-in-time production.

Improve Post-Delivery Cost Efficiency: Invest in digital supply chain solutions for real-time product tracking and streamlined regulatory reporting.

Stricter Receivables Management: Shorten collection periods and negotiate better terms with large customers. Utilize financial instruments like factoring.

For the Cement Industry:

Maintain Supplier Credit Leveraging: Continue leveraging supplier credit but manage liquidity risks.

Reduce Supply Chain Inefficiencies: Address bottlenecks and delays despite shorter supply chain lengths.

Like this project

Posted Dec 11, 2024

Compared supply chains of cement and pharma industries, analyzing key metrics and cost breakdowns, identifying inefficiencies, and recommending strategies.