Researching financial markets through WSJ & Factset.

Altaf Safi

Financial Analyst, Altaf Safi

Company Background

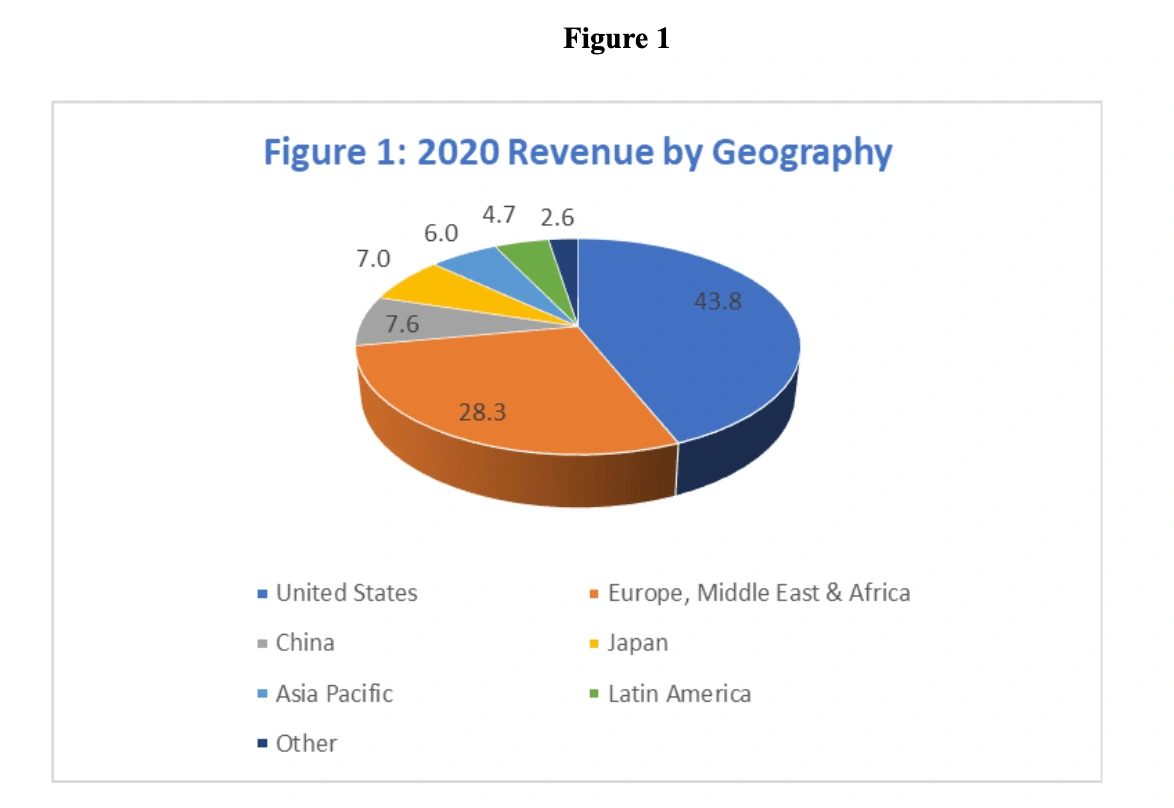

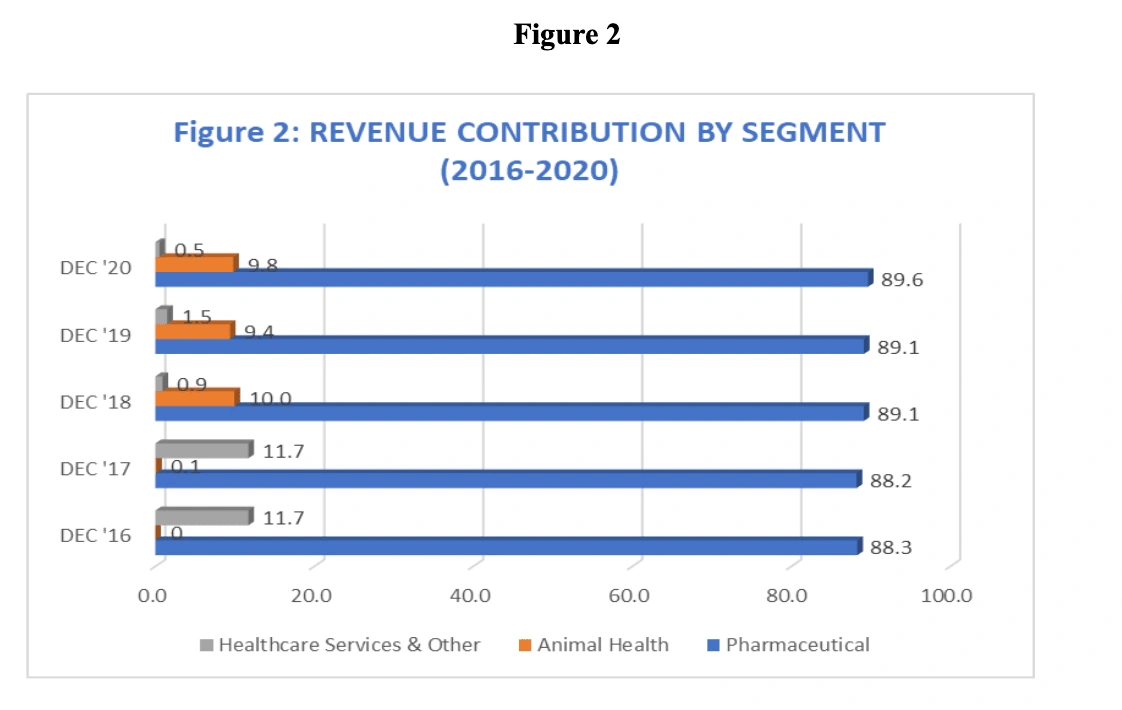

Merck and Co. (NYSE symbol: MRK but also known as MSD in markets outside of the US and Canada) is a leading science and technology company, active in Healthcare, Life Science, and Performance Materials. For more than 130 years, this pharmaceutical giant has been developing drugs and vaccines for many of the world's most challenging diseases. Merck & Co. has branches in more than 140 countries around the world (see Figure 1), with more than 80,000 employees. The company’s annual sales are among the top in the pharmaceutical and healthcare industries. Merck also holds a dominant position in the domestic specialty health industry across the following segments: Pharmaceutical, Animal Health, Healthcare Services, and Other (see revenue mix in Figure 2) with the highest revenue coming from Pharmaceutical. With this potential, Merck sells its human health pharmaceutical products (Figure 3 gives details on Merck’s products) to wholesalers, distributors, retailers, hospitals, government agencies, and managed healthcare providers such as health maintenance organizations, and other institutions. Merck's entity structure is very diverse and has more than 450 subsidies, but there are three outstanding branches. The branches are EMD Serono in the Biopharma business, MilliporeSigma in the Life Science business, and EMD Performance Materials in the materials business.

EMD Serono, Inc. discovers and develops biopharmaceutical products. The company is based in Rockland, Massachusetts. EMD Serono, Inc. operates as a subsidiary of Merck Serono. It focuses on specialized areas, such as neurodegenerative diseases, fertility, and metabolic endocrinology, as well as oncology. The company also provides Saizen for growth hormone deficiency in children and adults; Serostim for HIV-associated wasting; Zorbtive for short bowel syndrome; and Rebif for the treatment of relapsing-remitting multiple sclerosis (MS). In addition, it offers Fertility LifeLines, an educational service that offers customized information and support to individuals at various stages of the patient journey.

MilliporeSigma is a Life Science and High Technology company. The company’s chemical and biochemical products and kits are used in scientific research, including genomic and proteomic research, biotechnology, the diagnosis of disease and as key components in pharmaceutical and other high technology manufacturing. MilliporeSigma operates in 40 countries and has 7,600 employees providing excellent services worldwide. MilliporeSigma is committed to accelerating customers' success through innovation and leadership in life science, high technology and service.

EMD Performance Materials Corp. is the North American high-tech materials business of Merck KGaA in Darmstadt, Germany. It comprises a portfolio of applications in fields such as consumer electronics, semiconductors, lighting, coatings, printing technology, plastics, and cosmetics. Key products include high-purity specialty chemicals for the electronics and semiconductor industry, display materials, LED materials for lighting as well as OLED materials for lighting and displays, functional materials for solar panels and energy solutions. The business has about 500 employees around the country with main operations in Philadelphia.

Merck and Co in the News

Merck and Co. took advantage of the amount of news coverage focused on the COVID- 19 pandemic and the business opportunity that the deadly virus presented to the pharmaceutical industry. Merck was one of the first companies to develop a COVID-19 antiviral pill called Molnupiravir. On November 4th of this year, Merck announced that the United Kingdom Medicines and Healthcare products Regulatory Agency had granted authorization in the United Kingdom for Molnupiravir as the first antiviral medicine to treat mild to moderate COVID-19 in adults with a positive SARS-CoV2 diagnostic test, according to an article published by Merck (“Merck and Ridgeback’s”, 2021). Additionally, Merck has also submitted an application to the U.S Food and Drug Administration for Emergency Use Authorization of Molnupiravir and it is currently under review. Unfortunately, Merck’s competitor Pfizer has also developed an oral antiviral pill called paxlovid and has applied to the FDA for Emergency Use Authorization to treat people with COVID-19 who are at high risk. In clinical trials paxlovid was found to sharply reduce the risk of hospitalization or death and appears to be more effective than Molnupiravir, according to an article in The New York Times (Robbins, 2021). Recently on CNBS News, it was reported that President Biden announced that the U.S has signed a $5.9 billion deal with Pfizer to purchase 10 million courses of paxlovid (Kimball, 2021). This deal can potentially affect Merck’s projection of sales, which range between $5 billion and $7 billion in 2022, for Molnupiravir and with that benefiting Pfizer, its competitor.

The recent U.S FDA approval of Merck’s top product Keytruda is a significant win for the pharmaceutical company. “Keytruda is now the first immunotherapy approved for the adjuvant treatment of patients with renal cell carcinoma...,” (“FDA Approves Merck’s Keytruda”, 2021). This approval gives Merck an advantage over its competition and has positively impacted the company financially. Merck’s second quarter financial results indicated that Keytruda sales grew by 23% to $4.2 billion and significantly contributed to the company’s growth in its oncology portfolio (“Merck Announces Second-Quarter”, 2021).

It is important to note Merck’s recent acquisitions along with their future plans for acquisitions as this can have a huge effect on the future success of the company. On April 1st of 2021, Merck completed its acquisition of Pandion Therapeutics in which Pandion became an owned subsidiary of Merck for a total value of $1.85 billion (Nawrat, 2021). Pandion’s TALON technology that is used to re-balance the immune response in patients with an autoimmune disease is what sparked Merck’s interest in acquiring the company. The acquisition of Pandion will help diversify the company’s already broad portfolio.

In addition, Merck plans to expand its cardiovascular portfolio with their recently signed agreement to acquire Acceleron Pharma for $11.5 billion total equity value. Under the agreement, Merck, through a subsidiary, will initiate a tender offer for the acquisition of Acceleron shares. The acquisition will allow Merck to gain access to Acceleron’s lead therapeutic candidate, sotatercept, that is a new therapy mechanism to potentially boost short term or long-term clinical results in pulmonary arterial hypertension patients (PAH)(''Merck agrees to acquire Acceleron”, 2021). This acquisition can strengthen and grow their cardiovascular portfolio as sotatercept is currently being analyzed in Phase 3 clinical trials as an add on therapy to treat PAH patients. Acceleron’s portfolio also includes Reblozyl that has been approved for use in the U.S, Europe, Canada and Australia for treating anemia in certain rare blood disorders. Reblozyl is being developed and marketed through an international partnership with Bristol Myers Squibb. The acquisition is expected to conclude in the fourth quarter of 2021 upon receiving approval (''Merck agrees to acquire Acceleron”, 2021). The acquisition of Acceleron is a huge advantage for Merck as the company has valuable products that can further grow and expand Merck’s portfolio of products.

Merck’s future looks promising as their portfolio is expanding and growing with their recent acquisitions. The pharmaceutical company does face competition in sales for their COVID-19 antiviral pill Molnupiravir that is currently awaiting Emergency Use Authorization in the United States. Pfizer’s oral medication Paxlovid has shown to be more effective than Molnupiravir and these results can potentially affect Merck’s revenue for the drug. Despite the competitive threat that Merck faces, their recent acquisitions and the U.S. FDA approval of their top product Keytruda can help make up for the loss of sales that they might experience with Molnupiravir.

Economic Analysis

Merck’s future economic standing with respect to the stock market is highly dependent on the economic environment. The stock market reacts to changes in the monetary policy that is set by the federal reserves. A contractionary monetary policy can cut the funding availability for market makers in the stock market and the Federal Reserve may inject risk in the stock market when it tries to dampen the business cycle and stabilize the economy (Jiang, 2011). The Federal Reserve reacts to changes in inflation by increasing or decreasing interest rates. Therefore, analyzing the economy is important in order to predict interest rates, stock liquidity, and the riskiness of securities.

Economic Indicators

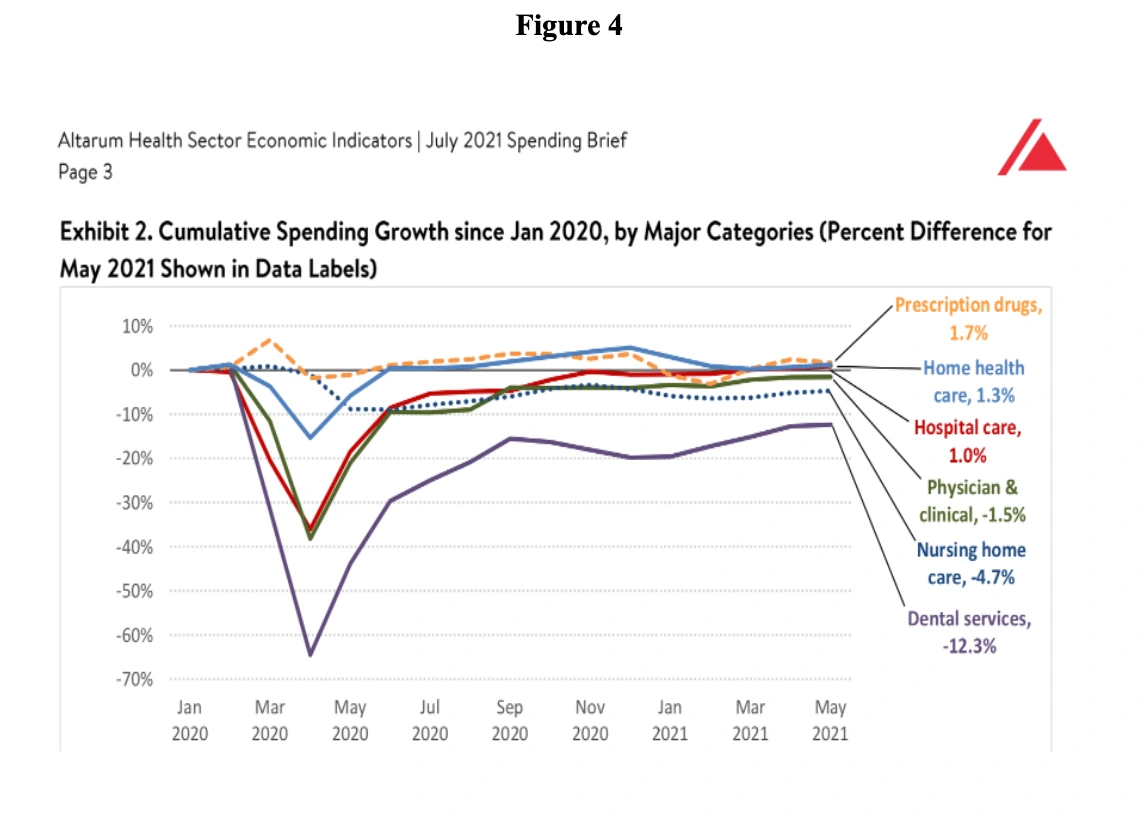

The COVID-19 pandemic has affected the world’s economic standing; however, the economy is starting to recover slowly. The U.S. unemployment rate fell to 4.6% in October 2021 according to the U.S Bureau of Labor Statistics. This is a good indication that more people are being employed and with that benefiting the economy. “National Health spending in May 2021 was 15.7% higher than in May 2020, reflecting the continued recovery from the effects of the COVID-19 pandemic” (“Health Sector Economic Indicators”,2021). According to a report published by Altrum, a non-profit research and consulting organization, health spending has grown more slowly than GDP in recent months. Prescription drug spending showed the greatest growth since January 2020 as shown in the graph below. This is a good economic indicator for Merck as it shows that the pharmaceutical industry is recovering faster than other industries in the healthcare sector. A low unemployment rate is also a positive factor as more people are contributing to the economy.

Another contributing factor to the U.S economy that can affect Merck’s stock price is inflation. The consumer price index has increased by 6.2% since October of 2020 and is the largest twelve month increase since November of 1990, according to the U.S Bureau of Labor Statistics. The price for consumer goods has increased dramatically within this past year and is a good indication of high inflation. The U.S inflation is currently at 5.4% and according to Fed Chairman, Jerome Powell and Treasury Secretary Janet Yelllen, the current price pressures are temporary and related to the pandemic issues. While inflation has been more persistent than they expected, they see conditions returning to normal over the next year or so (Cox, 2021).

If inflation continues to increase, the Federal Reserve might adjust the monetary policy in order to slow the growth of the money supply and bring down inflation. A contractionary monetary policy increases interest rates and slows down economic growth. Additionally, a contractionary policy can cut the funding availability for market makers in the stock market, driving down stock liquidity. For this reason, “investors should be careful with monetary policy effects on their asset liquidity and take the shock of monetary policy into account when making their investment choices and form portfolios” (Jiang, 2011). If inflation persists, the Federal Reserve will react by increasing interest rates and this negatively impacts earnings and stock prices. Although inflation is high at the moment and is expected to decrease in the near future, the unpredictability of how the Federal Reserve will respond makes investments riskier.

There are global efforts towards health care costs that put pressure on Merck & Co. product pricing and market access around the world. The current changes to the US healthcare system as part of a reform, has allowed for healthcare industries like Merck & Co. to have an increased purchasing power to negotiate on behalf of Medicare, Medicaid, and other private sector beneficiaries. The healthcare reforms and the purchasing power of the healthcare industries contribute to pricing pressures (“Merck & co inc,” 2020). In several foreign markets, governments have imposed pricing restrictions that forced health care industries like Merck & Co. to reduce prices of generic and patented drugs. During 2019, Merck & Co. had a revenue performance that was negatively affected by governmental cost-reduction policies due to government requirements. (“Merck & co inc,” 2020). The company believes that as such governmental regulations and actions continue to take place, it will negatively affect their revenue performance in the future (“Merck & co inc,” 2020).

Economic Outlook

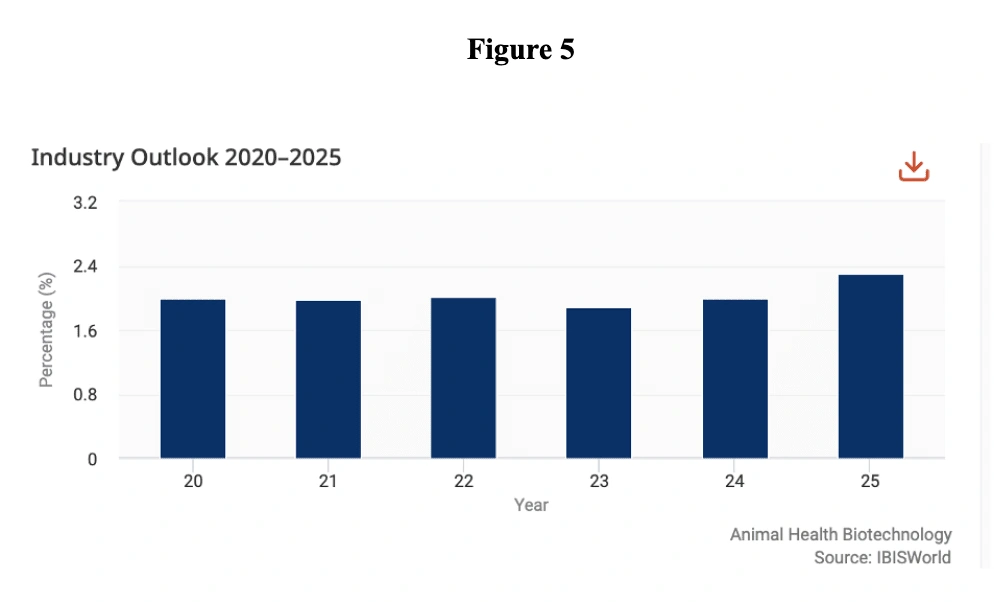

Along with the current state of the economy, it is also important to consider how the future economic outlook will affect Merck and Co. This is significant to our analysis in predicting the company’s stock price. The U.S Specialized Industry Report number OD4023 written by Dan Spitzer provided important insight on the future economic outlook of the Animal Health Biotechnology industry in which Merck and Co. is a major player. The accelerated growth in the number of pets and rising global demand for livestock products are expected to fuel the demand in the industry for veterinary medicine and vaccines, extending the average lifespan of companion animals and further fueling industry expansion. Rising demand for industry products to protect livestock is a positive sign for Merck and Co. as the company has an expansive portfolio in animal health medicine for livestock. Consequently, the increase in demand is expected to lead to an increase in industry competition. However, if Merck and Co. continues to develop innovative drugs and expand its portfolio to diagnostic products to identify and treat diseases, then they are likely to beat their competition. The threat of diseases in livestock is a pressing issue and this poses an opportunity for Merck and Co. to expand their portfolio in the Animal Health Biotechnology sector. “The Animal Health Biotechnology industry is expected to steadily grow over the next five years to 2025, with revenue forecast to increase at an annualized rate of 2.0% to $12.0 billion”, as shown in the graph below (Spitzer, 2020).

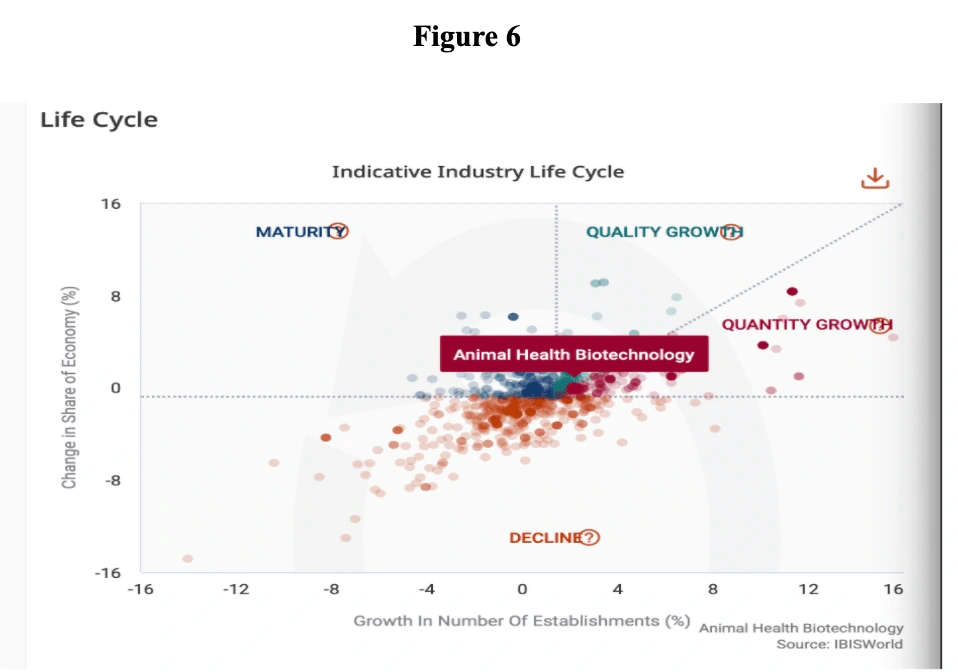

Furthermore, the industry life cycle for the Animal Health Biotechnology business is in the growth stage, as can be seen below. This is also a positive indication for Merck and Co. future outlook in this industry.

Contrary to the Animal Health Biotechnology industry, the Brand Name Pharmaceutical Manufacturing industry is at a mature stage of its life cycle. The market is expected to expand over the next five years and with that increasing market competition and price scrutiny that might dampen revenue prospects (Kennedy, 2021). However, as supply chains are rebuilt and made more robust, operating costs will decrease and this will enable Merck to sustain price competition. Merck also has a diversified portfolio that includes products in oncology, neurodegenerative diseases, fertility, and metabolic endocrinology among others that will help Merck overcome their competition and sustain revenue.

Merck and Co. is also a major player in the Global Biotechnology industry that is expected to rise over the next five years according to the Global Biotechnology industry report number L6724-GL. The growth will be supported by global investments in biotechnology, particularly in emerging economies. The industry revenue is expected to rise an annualized 3.1% to $ 347.3 billion. The Global Biotechnology industry is in the growth phase of its economic life cycle. This is due to an abundance of new market opportunities, rising industry participation, and rapid technological advancement. If Merck and Co. continues to provide innovative products and prioritizes their biotech and pharmaceutical product development, the company will benefit from new avenues of revenue.

Industry Analysis

The global Pharmaceutical Manufacturers—General industry was worth $405.52 billion in 2020 and is expected to grow at a compound annual growth rate (CAGR) of 11.34% from 2021 to 2028. However, product pricing and market access are under pressure from global efforts to reduce health care costs, as previously mentioned. Research and development play a large role in this industry, which is constantly evolving. More than 32.3% of the healthcare sector is accounted for which is highly capital-intensive with high R&D costs. Since 1960, over $300 billion in U.S revenue has been driven from the sales of prescription drugs (brand name and generic) and over-the-counter medicines. The U.S. pharmaceutical market share is the highest in the world, with five of the ten largest manufacturers based in the country (Johnson & Johnson, Merck & Co., Pfizer, Abbott Laboratories, etc.) (15 astonishing statistics and facts about U.S. Pharmaceutical Industry)

There is a high level of competition and government regulation in Merck's markets, as well as the pharmaceutical industry in general. Competition in the pharmaceutical industry is based on a constant search for technological advancements and the ability to effectively market these advancements. For decades, Merck has placed a high priority on research and development, putting it in a strong position to compete for technological breakthroughs. External alliances, such as licensing agreements and collaborations, are a major part of Merck's strategy for acquiring and promoting its products. Nevertheless, even for patent-protected products, the launch of new products and mechanisms by competitors may lead to price cutbacks and product displacement. For instance, as the amount of substances available to treat a specific disease grows, the company's products in that therapeutic segment may encounter slower growth or a drop in sales.

There has been a long-standing effort by federal and state governments in the United States to bring down the cost of drugs and vaccines that they are responsible for paying for. Federal and state laws, for example, ensure that companies pay designated rebates for medications compensated by Medicaid as well as provide discounts for medications acquired by certain state and federal institutions, mainly the Department of Defense, Veterans Affairs, Public Health Service entities, and hospitals serving a disproportionate share of low income or uninsured patients. (Medicaid Drug Rebate Program). In Japan, the pharmaceutical industry is subject to government-mandated price reductions every two years for certain pharmaceutical products and vaccines (Japan's Second Biennial Report).

Re-pricing orders can also be issued by the government in cases where it defines that using a particular product will exceed thresholds established by the government's repricing rules. Many of Merck's products are likely to see a price cut when the next round of price reductions is implemented in 2022. On the other hand, the Chinese government has instead implemented a series of structural reforms in past years to expedite the shift toward innovative products while also reducing costs (Organon & Co. Form 10). Numerous new policies have been instituted by the government since 2017 in improving access to “breakthrough” technology, minimizing regulatory filing sophistication, and speeding up the review and approval process. Consequently, the number of new products approved each year has increased significantly. Drugs were added to the National Reimbursement Drug List (NRDL) in 2020 after “double-digits” price reductions were achieved. But even as price competition has always occurred throughout China, health care reform has exacerbated it, partially due to the momentum of generic substitution via volume-based procurement (VBP).

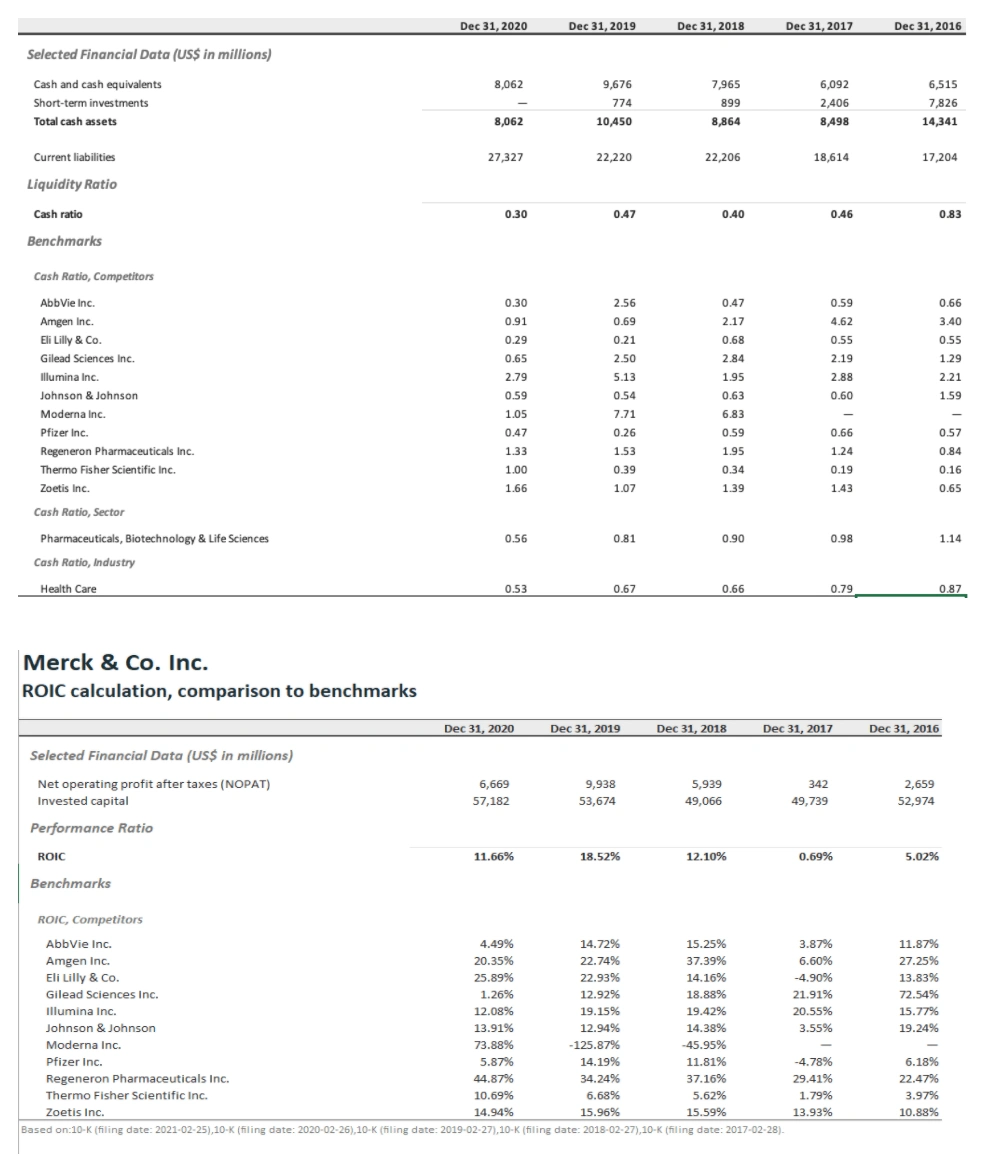

It is also important to compare Merck and Co. returns on invested capital with the company’s competitors. Below in Figure 8, you can see that Merck and Co returns are steady and do not fluctuate as those of Moderna, Zoetis, and Pfizer. Although Merck’s returns are steady meaning they are not as risky as some of their competitors, their returns are also not growing exponentially. A riskier company would have returns on capital that are increasing at a faster pace than the rest. The jump in returns on invested capital for Moderna, Zoetis, and Pfizer can be associated with the COVID-19 pandemic that emerged during the beginning of last year. Zoetis is a subsidiary of Pfizer and their rise in invested capital can be associated with Pfizer’s success. As you will find in Figure 8, all of the competitors listed have a higher return on invested capital than Merck and Co. This is a concerning finding we should take into consideration when determining whether to hold or sell the company’s stock.

Company Analysis

The pharmaceutical segment provides the most growth and profits for the company. The segment provides drugs and vaccines that can treat diverse health conditions like the respiratory system, cancer, and other infectious diseases (“Merck & co inc,” 2020). The pharmaceutical segment was reported to have revenue of $41,751 million during 2019, meaning there was a 10.8% increase since 2018. The revenue increased due to higher sales during 2019 from Keytruda, Gardasil, ProQuad, Bridion, and Pneumovax 23. The segment also reported an operating profit of $28,324 million in 2019. This means that profits have increased by 13.9% since 2018. Overall, the pharmaceutical profits were due to higher sales and lower selling costs in 2019 (“Merck & co inc,” 2020).

Additionally, the company focuses on research and development which helps it expand and improve its product base and offer innovative products that meet customer expectations. The company has the strategic advantage of collaborating with other organizations to develop early research for late-stage diseases (“Merck & co inc,” 2020). Moreover, Merck Animal Health is one of the top animal health companies in the world that researches, develops, manufactures, and sells veterinary medicines. During 2019, the company obtained 9.4% of its revenue from the animal health segment. Merck Animal Health provides veterinarians, pet owners, farmers, and governments a wide range of anti-infective and anti-parasitic drugs, vaccines, innovative delivery solutions, and value added programs like livestock data management tools and pet recovery services. Merck Animal Health invests the majority of its funds in comprehensive R&D resources and for a modern global supply chain. During 2019, the Animal Health segment reported revenue of $4,393 million, meaning the revenue increased by 4.3% since 2018. The growth in revenue was primarily due to higher sales generated from livestock products and companion animal products. The growth in revenue was also because there was a high demand for swine and aqua products (“Merck & co inc,” 2020).

Furthermore, When Merck & Co. discontinues its product development and stops during various phases of clinical studies, it loses a high amount of monetary investments and intellectual time. For instance, when the company found that Keytruda could cause immune-mediated pneumonitis, including death if used as a single agent in patients with non-small cell lung cancer (“Merck & co inc,” 2020). Merck discontinued clinical trials and developments when the product started to affect patients with advancing the disease and producing further complications. Moreover, there are several product liability claims against Merck & Co. due to testing errors, manufacturing defects, and other marketing and sale of its products. These liability claims can affect the company’s product commercialization and impair the company’s operations (“Merck & co inc,” 2020). As of December 31, 2019, there were 3,750 cases against Merck. These liability claims could prevent the company from developing the same product that once affected a person, thus, it could decrease the company’s profits if the product was a highly sold product. Such liability claims and allegations could generate negative publicity about Merck’s products and prevent commercialization of other future product candidates (“Merck & co inc,” 2020).

The majority of Merck’s revenues are highly dependent on a small group of customers. If the company loses a high amount of revenues, it would be due to losing its customers. The company’s main customers are AmerisourceBergen Corporation, Cardinal Health Incorporation, and McKesson Corporation. These three customers account for 35% of Merck’s total accounts receivable as of 2019 (“Merck & co inc,” 2020). If Merck loses any of these customers, then Merck’s profits and financial position will be affected.

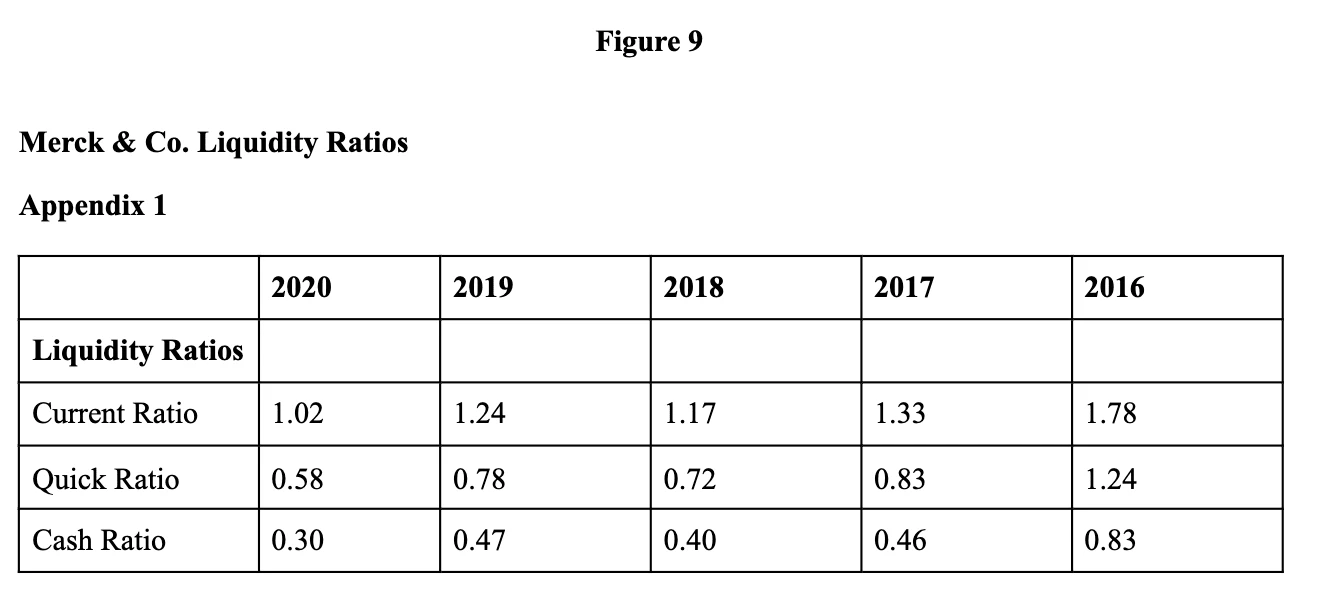

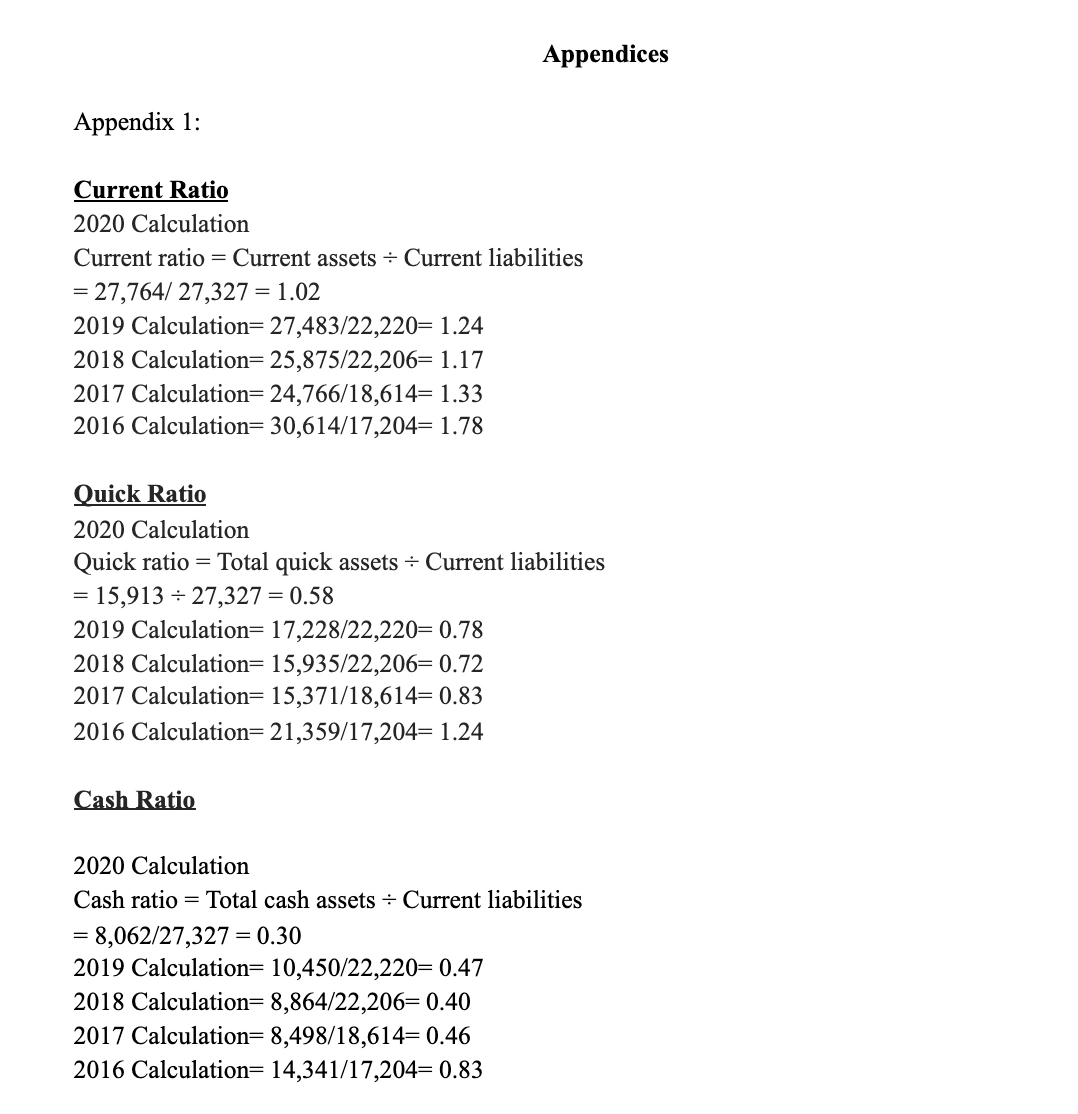

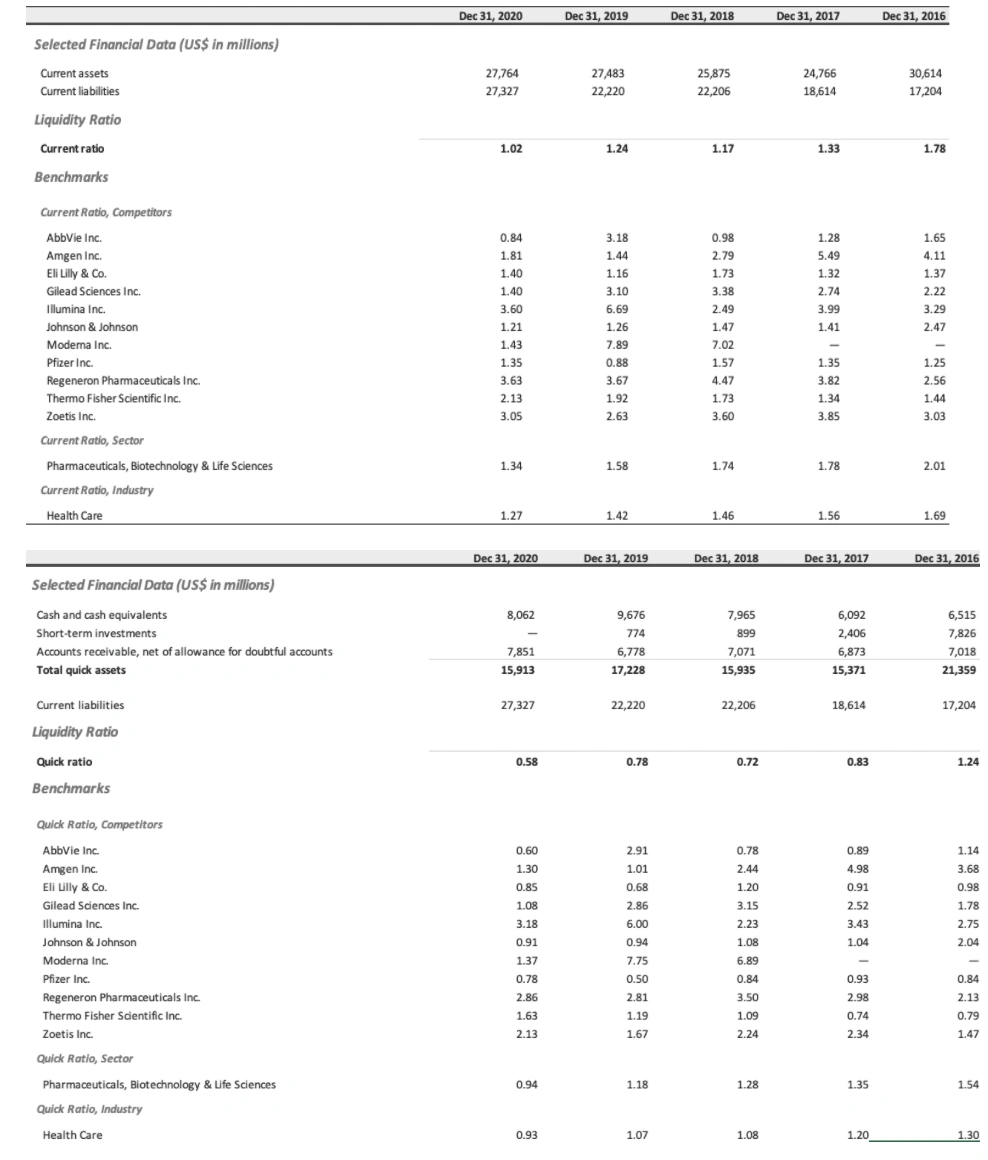

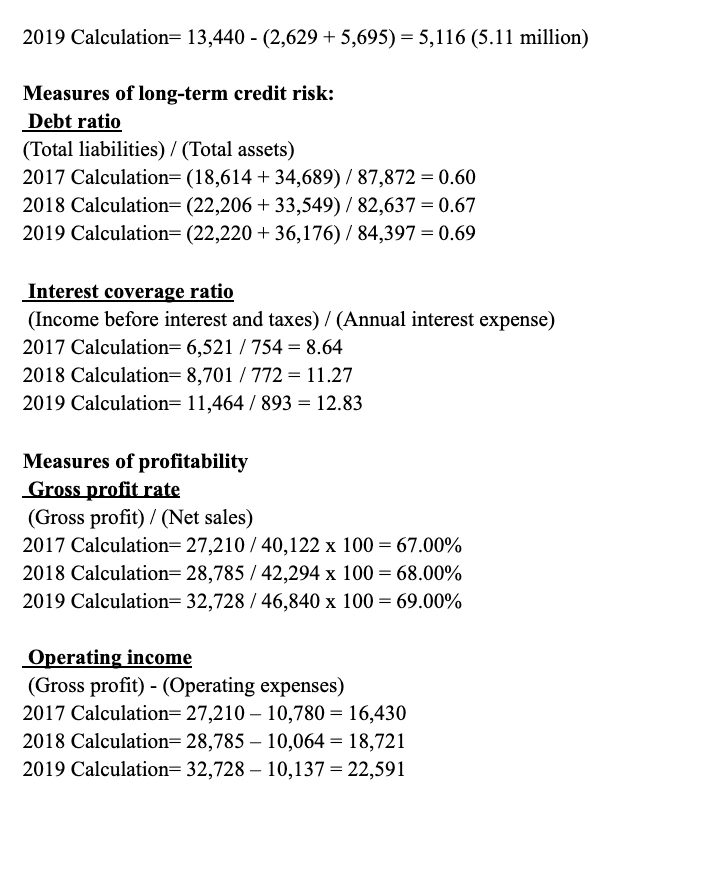

To better understand Merck and Co., we will compare the company ratios to the overall industry ratios. When we look at these ratios, we are able to compare Merck’s performance compared to its competitors. We found the ratios using the data of the recent five years from the 10-K annual reports. The liquidity ratios show that Merck’s current ratio has decreased since 2016. However, there were two years that the ratios increased and remained high. The ratios of the healthcare industry also increased in those two years where current ratios of the company increased. For instance, the two highest current ratios were during 2017 and 2019 of the company. It can be seen that Merck’s current ratio improved from 2018 to 2019 but then declined significantly in performance from 2019 to 2020. The quick ratio is interesting because Merck’s pharmaceutical clinical trials, drugs, and vaccines hold substantial value on their financial statements. Merck’s latest quick ratio is 0.58, which is slightly under the healthcare industry ratio average of 0.93. Cash ratios have been decreasing every year since 2016, however, there was a small increase in 2019 but a massive drop in 2020. The decline in cash ratio after 2016 suggests us that Merck would not be able to generate enough cash to pay off short-term debts. Factors that have caused this decline in cash ratio could be due to an increase in short-term debt or a decrease in current assets.

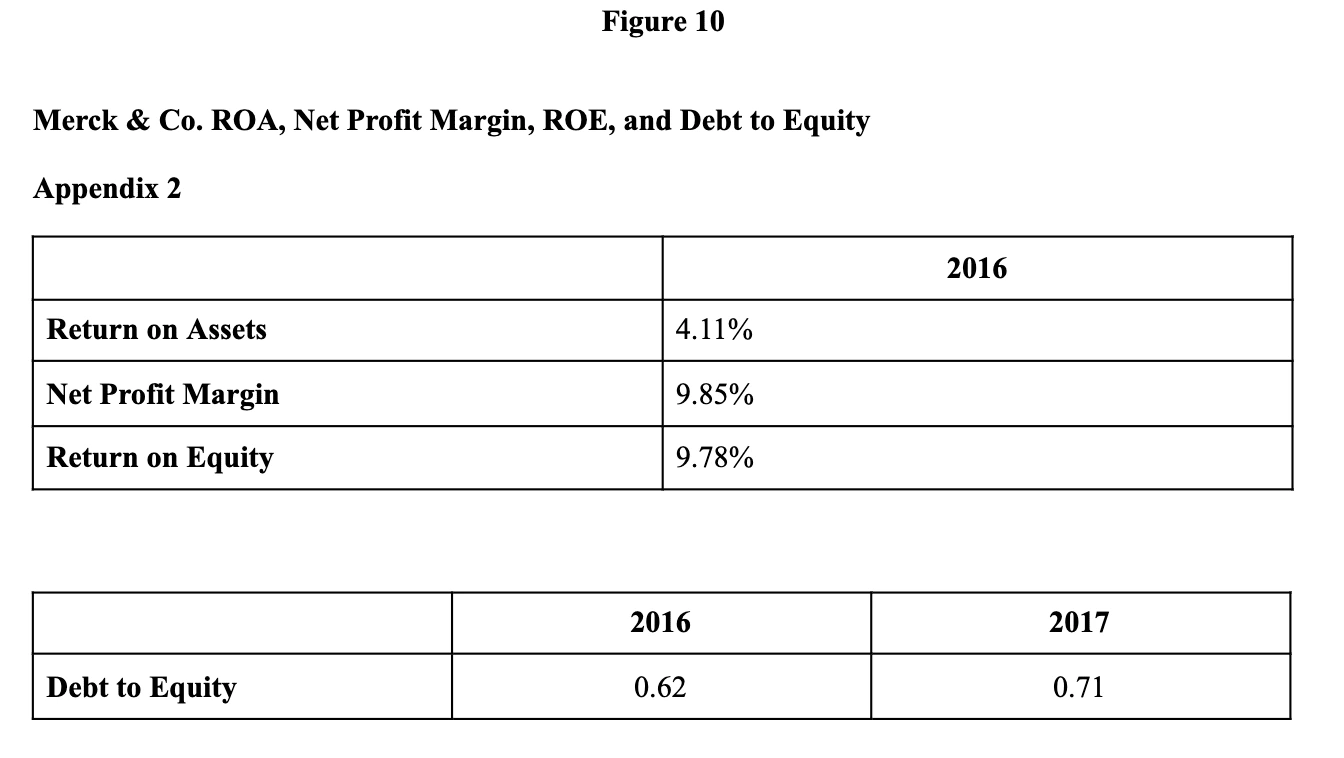

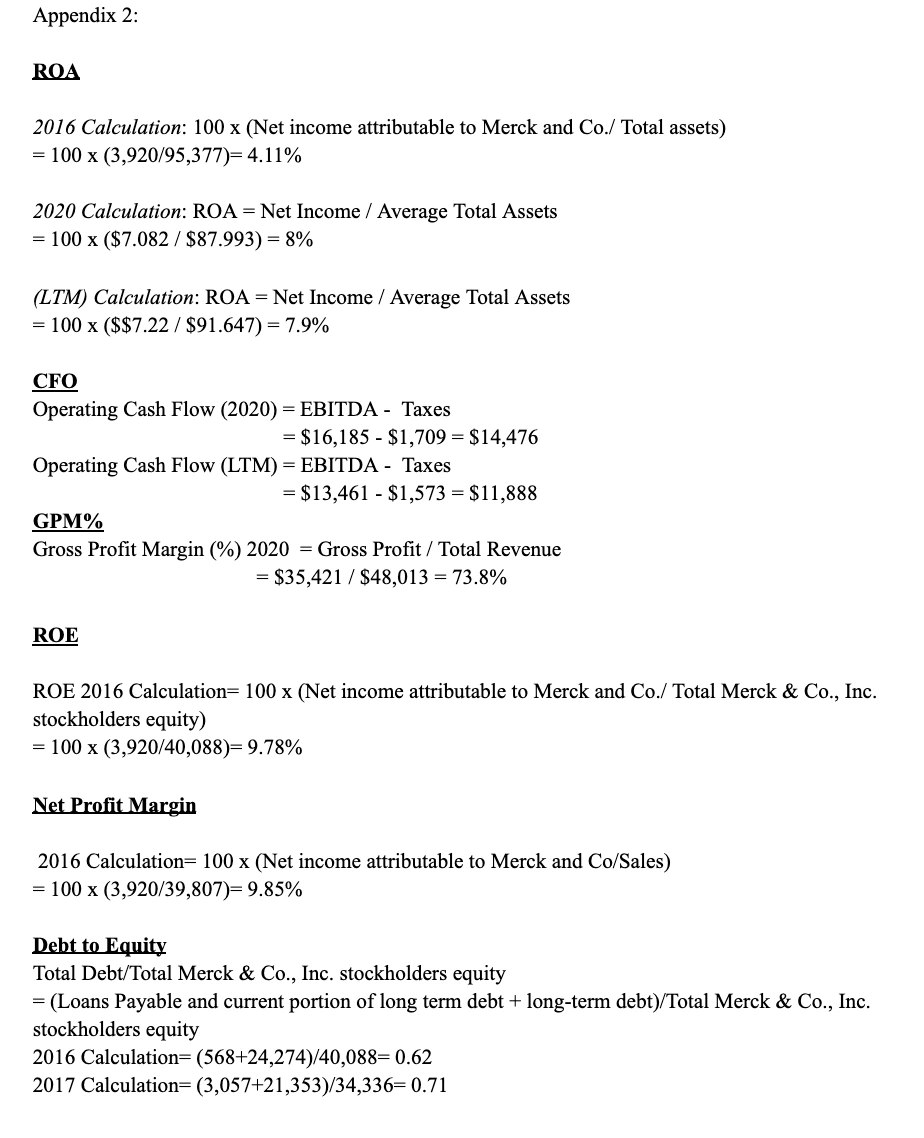

In 2016, Merck announced two partnerships with Quartet Medicine and Complix. They estimated that their partnership will generate up to $595 million and $280 million. Later in 2016, they also announced the acquisition of IOmet Pharma and Afferent Pharmaceuticals. The increase in cash, short term investments, and receivables from the partnerships has caused the quick ratio to rise to 1.24%. Due to the company’s lower net income, ROA decreased to 4.11%, ROE decreased to 9.78%, and net profit margin decreased to 9.85%. Moreover, in 2017, Merck made more acquisitions with Vallee, a Brazilian animal health products manufacturer. Later during the year, Merck also acquired Rigontec for $554 million. The quick ratio declined to 0.83% and cash ratio declined to 0.46% due to a decrease in cash and short term investments. However, debt to equity increased to 0.71 due to increases in total liabilities and decreases in stockholders’ equity.

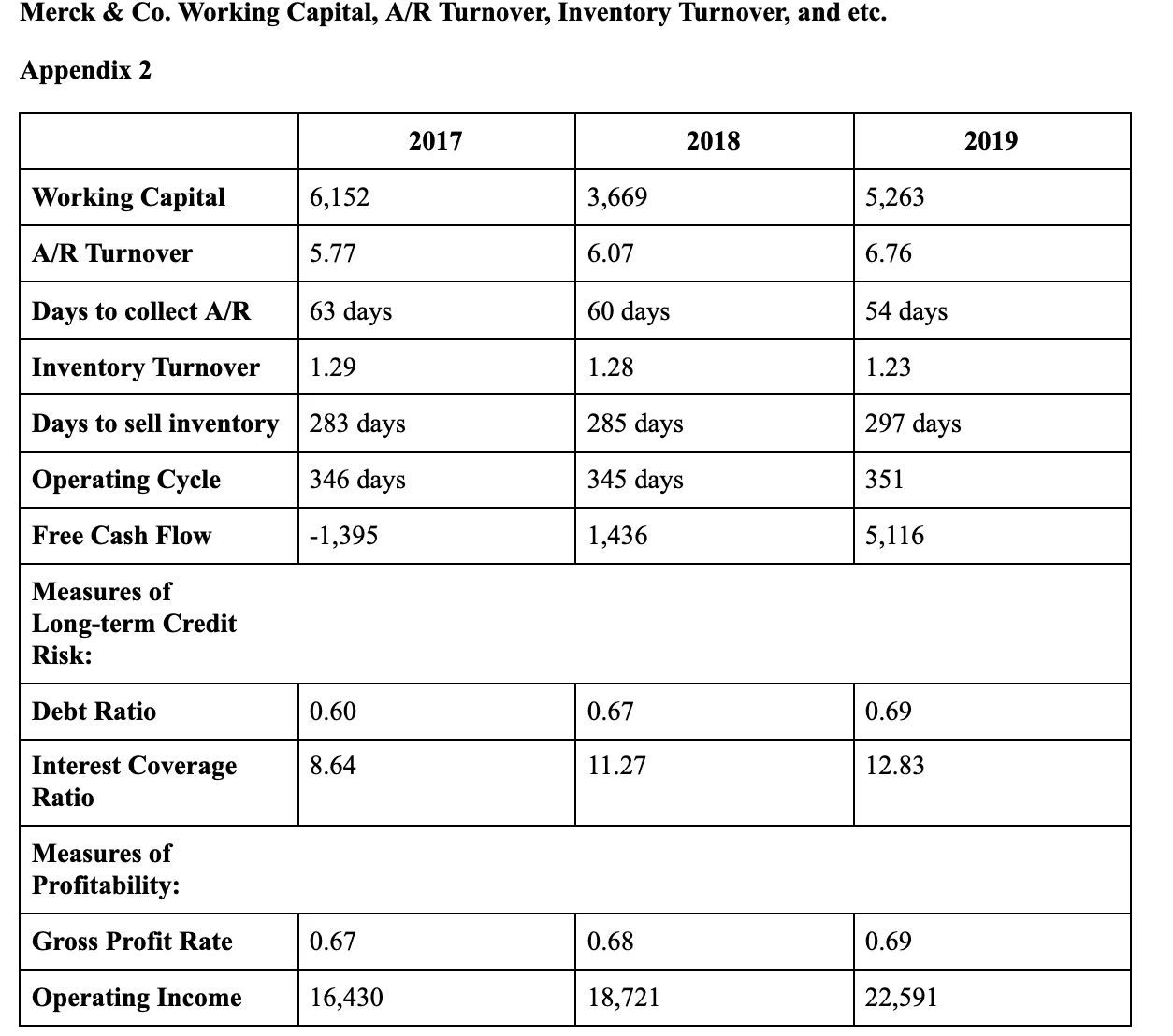

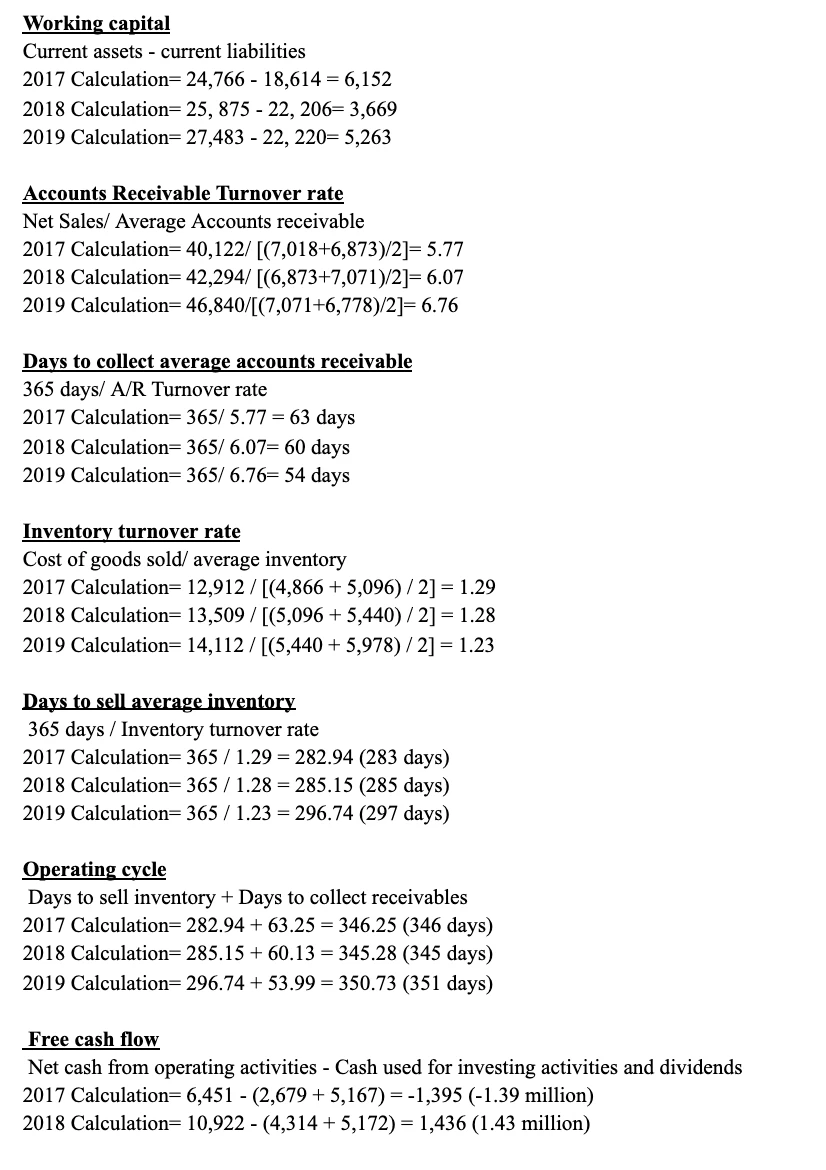

Additionally, the working capital determines the difference between current assets and current liabilities in Merck. The working capital helps in identifying the company’s liquidity status. When compared with competitors like Amgen Inc., it can be understood that Merck does not have as much working capital as the competitor Amgen Inc., therefore, the working capital of Merck declines and rises much slower than Amgen Incorporation. Merck would not be able to meet its obligations in the short-term. Moreover, a high accounts receivable turnover would be considered great for a company. Merck’s accounts receivable collection turnover shows that it is efficient. In other words, Merck is having an upward trend across years because it is collecting financial amounts more efficiently from debtors. As it can be seen in figure 11, the number of days for collecting financial amounts was decreasing in 2019 to 54 days, meaning Merck was starting to perform better than previous years and was overtaking competitors like Amgen Inc. in collection of financial amounts from debtors. When the number of days decreases, it shows efficiency in collecting receivables from debtors.

Furthermore, the inventory turnover ratio represents how many times an inventory is sold for a certain period of time. The inventory turnover for Merck shows that the company was able to sell its inventory quicker than competitors like Amgen Inc., meaning more sales were generated for a particular period of time. Merck was also successful in selling its inventory in lesser days compared to Amgen Inc. The operating cycle of the company represents the period of time it takes to convert the company’s inventories into cash. A shorter number of days would reflect more efficiency of the company’s operations. Merck’s operating cycle was almost constant in three years. This shows how efficiently the company’s management was able to convert its inventory into cash. The free cash flow of Merck was positive in 2018 and 2019, implying that the company manages its cash very well. If the free cash flow is negative, the company may need to search for other sources of funding such as debt financing. Merck’s free cash flow shows how capable the company is to produce internal growth and to offer shareholder profits.

Merck’s debt ratio was increasing from 2017 to 2018. When we looked at Amgen Inc. debt ratio as a competitor, we realized that Merck was performing better than Amgen Inc. because Merck’s debt ratio was less than Amgen Inc. Generally, when a ratio is less than 1, it means that a larger portion of assets are financed by the company from equity. The interest coverage ratio for Merck was increasing from 2017 to 2018. When there is an increase in ratio, it means that the company has a greater financial stability and that the company is more capable in fulfilling its interest obligations through operational income. A high interest coverage ratio also means that the company is ignoring opportunities to increase its profitability by leverage. Furthermore, Merck’s sales have been increasing in 2017, 2018, and 2019. This increase in sales shows that the gross profit rate had also increased. In other words, Merck had increasing gross profit rates in those three years. When compared with Merck’s competitor Amgen Inc., we noticed that Merck was increasing at a higher rate on its operating income than its competitor. In other words, Merck was performing better in business than Amgen Inc. because it had a better operating income.

Opportunities

Merck & Co. has been successful in generating higher revenue from its new products and in improving its market share. Merck has gained several regulatory approvals for its developments and distribution of business. In January 2019, the company gained approval from the United States Patent and Trademark Office for its patent to create crypto-objects based on blockchain technology and artificial intelligence for use in pharmaceutical supply chain management (“Merck & co inc,” 2020). Additionally, Merck continues to consider being part of strategic acquisitions and agreements for business growth purposes. These acquisitions and agreements will expand the company’s operations, developments, and business, including introducing new technologies, products, and geographical reach. For instance, in January 2020, Merck acquired ArQule Incorporation to develop kinase inhibitors to treat patients with cancer and other diseases (“Merck & co inc,” 2020).

As one of the top providers of cardiovascular drugs, Merck has the advantage to benefit from the growing pulmonary arterial hypertension market. According to in-house research, the overall sales of pulmonary arterial hypertension market is anticipated to grow in seven major pharmaceutical markets (“Merck & co inc,” 2020). Those seven pharmaceutical markets are the United States, France, Germany, Italy, Spain, UK, and Japan. By 2026, the overall market is expected to have sales of $4.7 billion. The factors that will influence the growth include higher price of pharmaceutical products and patient assistance programs by manufacturers that will help provide reimbursement support to patients. Research shows that pulmonary arterial hypertension is expected to increase among people to 63,047 cases by 2026 (“Merck & co inc,” 2020).

Merck has a development strategy that focuses on pursuing research to address unmet needs and perhaps improve therapies. Merck was able to obtain the FDA Orphan Drug designation for selumetinib, an inhibitor, for the treatment of neurofibromatosis type 1. The Orphan Drug designation helps in speeding up the process of development and commercialization of the drug candidate (“Merck & co inc,” 2020). Also, the Orphan Drug designation provides several benefits to Merck, including reduced costs of clinical trials and reduced fees for filing the Marketing Authorization application. The Orphan Drug designation provides upto 50% tax incentive on clinical development costs (“Merck & co inc,” 2020).

Threats

Merck’s products are located in very intense competitive environments. The company’s products experience competition from the new and innovative products produced by competitors. Merck’s competitors consist of big research-based pharmaceutical companies, generic drug manufacturers, and animal health care companies (“Merck & co inc,” 2020). The company’s major competitors are AbbVie Inc., Johnson & Johnson, Bristol-Myers Squibb Company, and Pfizer Inc. Moreover, changes in customer demand patterns, incentive programs, and the arrival of new products from competitors could affect the company’s competitive advantage, position, and ability to compete (“Merck & co inc,” 2020).

The US federal and state governments impose pricing pressures on Merck’s products. According to the US federal laws, Merck is responsible for paying specific rebates and discounts for medicines reimbursed by Medicaid, Public Health Service entities, and hospitals (“Merck & co inc,” 2020). The US government enforced major health care reform legislation, informing Merck as a pharmaceutical manufacturer to pay 50% of service discount to Medicare beneficiaries because it falls under the coverage gap provision. Merck reduced $615 million from its 2019 revenues and $365 million from its 2018 revenues. Merck was also required to pay an annual health care reform fee of $2.8 billion in 2019 (“Merck & co inc,” 2020).

Merck operates in a highly regulated industry where there are several statutes and regulations that should be complied with for the testing, manufacture, and sale of pharmaceutical products. The company has to gain approval from the regulation officers and departments like the FDA before commercializing its products (“Merck & co inc,” 2020). To receive marketing approval for new products, medical devices, and research procedures, is time consuming and expensive. If Merck fails to comply with the present and future regulations related to clinical, laboratory, and manufacturing practices, then it may result in delayed approval for drugs and even denied permission to produce or sell the drugs (“Merck & co inc,” 2020).

Stock Analysis

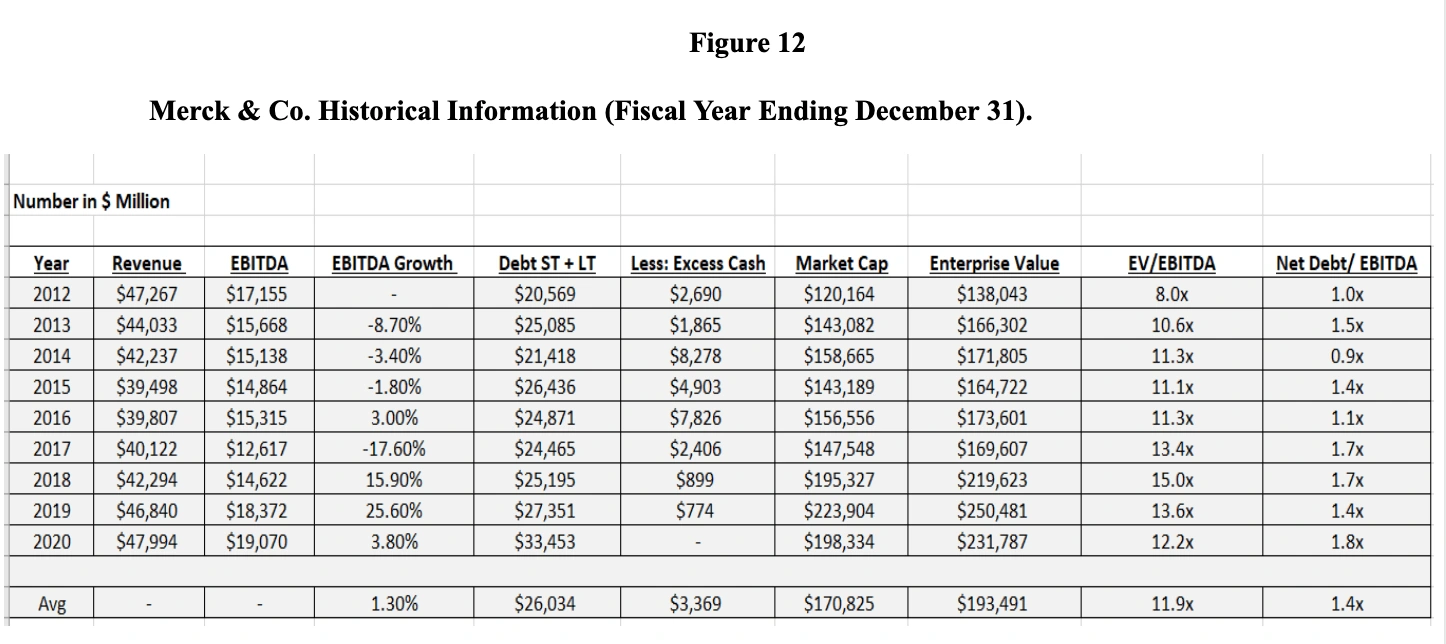

In Figure 12, EBITDA is enterprise level earnings whose profit I want to look at instead of EPS, because EPS can be manipulated by the number of shares outstanding. I only want a company or a business that on its face can grow revenues and earnings, then I can buy back shares and have more ownership stake in that business. However, the principal enterprise should be able to grow on its own. If considering over the past 10 years, 1.3% is not really a good number, however, it has been growing stably in 5 years recently. As for the debt, there is a 62.6% increase in the total amount that they have on relatively flat earnings (EBITDA). Iits then would expect the debt ratios to be going up, and it is because the company has a dividend which is relatively high to a free cash flow that they generate. Therefore, in order to maintain that dividend, they’re borrowing money as they run the business and that is not really a good sign. In addition, the excess cash has gone down to zero historically as debt has grown by 62.6%, which is another indication that the dividend is too high. Coming to the leverage ratio, the Net/EBITDA reflects more than 50% increase in cash on flat earnings and that is a 80% move on the ratio, which is clear evidence that debt is piling up as the company is not able to reinvest the borrowed money in high ROIC projects.

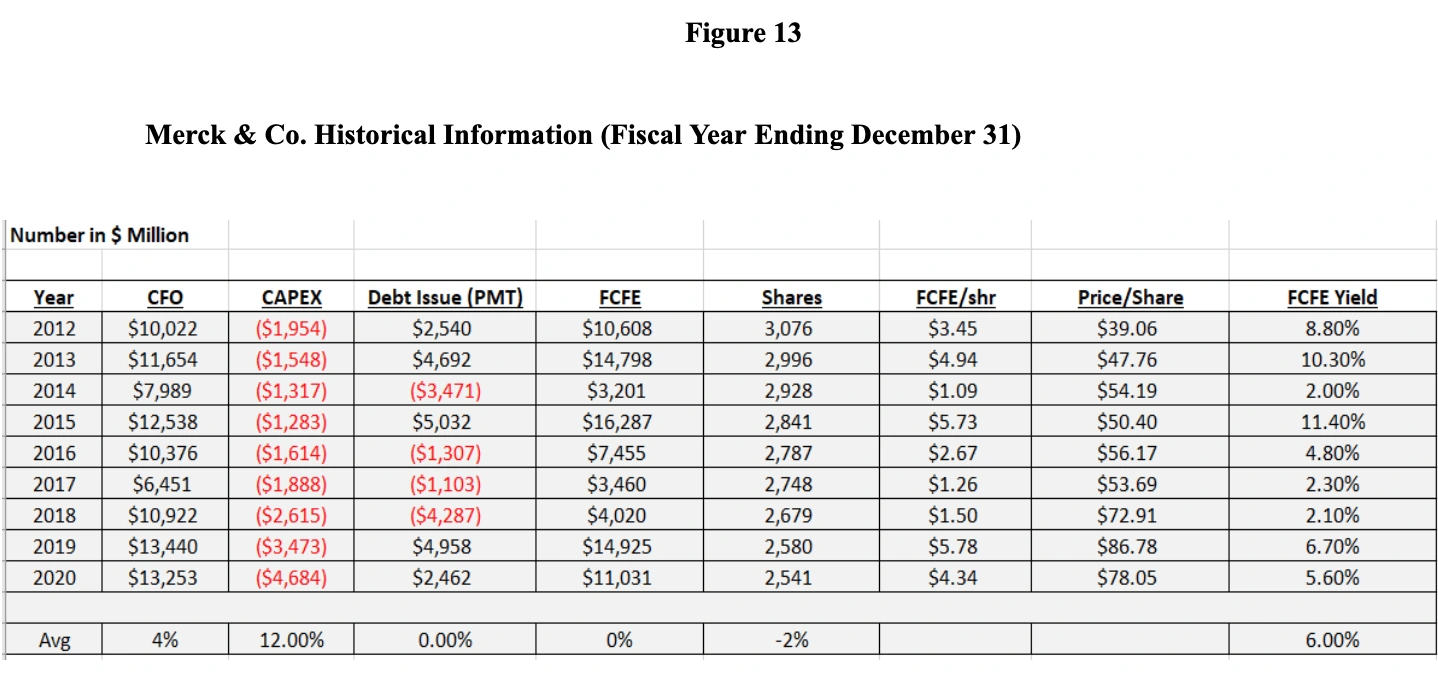

For figure 13,the free cash flow chart, CAPEX is growing steadily at 12% and that is a big number. The average difference between CAPEX and CFO is only a flat of 0.8%. This means the company is spending all its money in CAPEX but is not able to grow as it expected. The interesting thing is that they have been buying back shares as I think they are doing this to boost the EPS. Because as I discussed above, I only want to see enterprise level earnings growth, but their EBITDA and Free Cash Flows are flat even though they are paying dividends, so the only one way they can represent earnings growth to Wall Street (Wall Street looks at EPS) is to boost the EPS. The market seems to value this stock at about a 5% yield (FCFE Yield). In short, the Revenue, Cash Flow and EBITDA are still at a weak growth. Debt is still less than 3x but it is growing. To see if it is well-priced or not, I need to forecast the business and observe whether the future value is relative to the current.

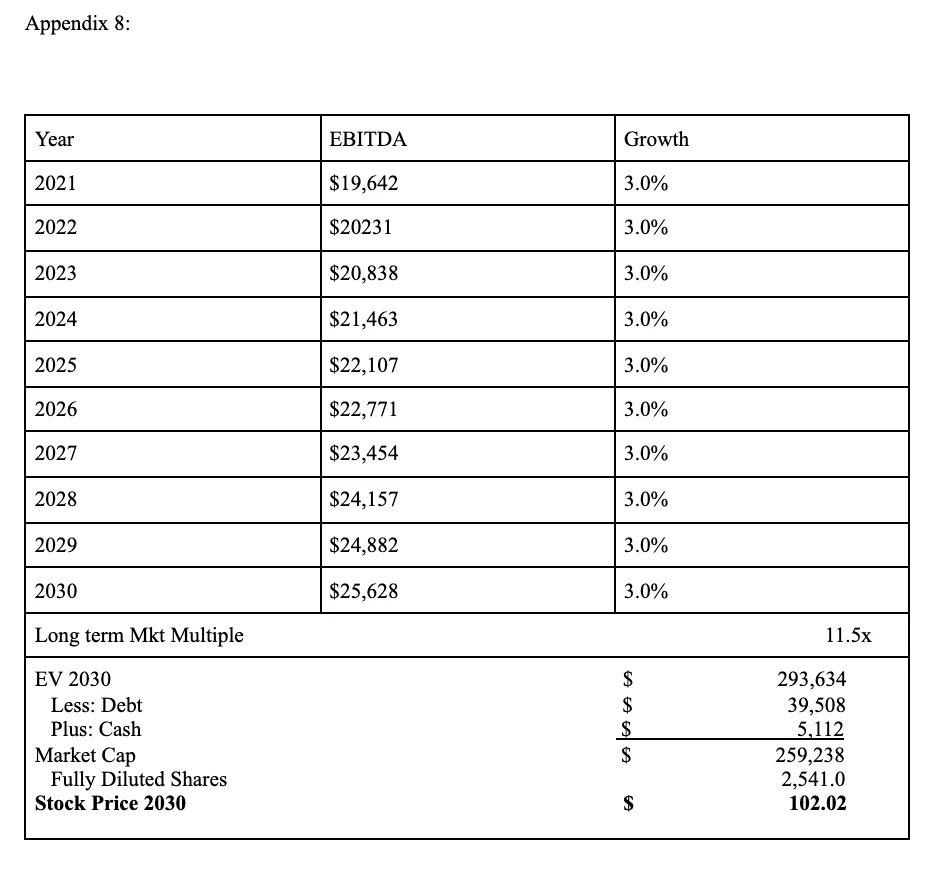

With the EV/EBITDA market multiple approach, I picked up 2020 EBITDA of about $19,070 million and then I grew it at 3%. The reason I used 3% is because they’re growing at 1% long-term 10 year average and recently they have had an uptick in EBITDA for 3%, 5%, and there’s one year with 11%. I wrote off the 11% because everything has been based on one or two drugs of the company, so I give the credit for 3% as a conservative growth forecast. Also, if I am investing my money into the stock, I would be buying the forecast that I have put down so this could be considered as a good risk-adjusted opportunity. After applying 3% all the way down to the year 2030, I got $25,628 billion of EBITDA. Then I took the historical average enterprise value to EBITDA ratio, which is 11.5x and I multiplied with $25,628 to get $293,634 billion enterprise level valuation for the business. I subtracted that number from debts and added cash in order to get the estimated market cap of $259,238 billion long-term. For the final result, I divided it by the current shares outstanding and came up with 2030 estimated price per share of $102.02 (Appendix 8).

The dividend discount model was used to calculate Merck and Co. expected price per share. I compared Merck’s and the S&P 500’s historical returns dating back to January 31, 2016 obtained from Yahoo Finance website. I then calculated the per share of common stock adjusted for stock dividends, the market rate of return, and the rate of return for common stock. I obtained an average rate of return of 1.19% for Merck and 1.22% for the S&P 500. The standard deviation for Merck was calculated to be 4.86% and 4.36% for the S&P 500. The standard deviation measures the volatility of the stock and this shows how much on average the yearly return is away from the mean. I then took the variance and covariance of Merck’s and the S&P 500’s rate of return. I also subtracted Merck’s rate of return from the rate of return of the S&P 500 and calculated the covariance. I obtained a positive number as shown below in appendix 3, showing that the stocks move in the same direction. The variance and covariance of the rate of returns was then used to calculate the beta for Merck which came out to be 0.42, as shown in appendix 4.

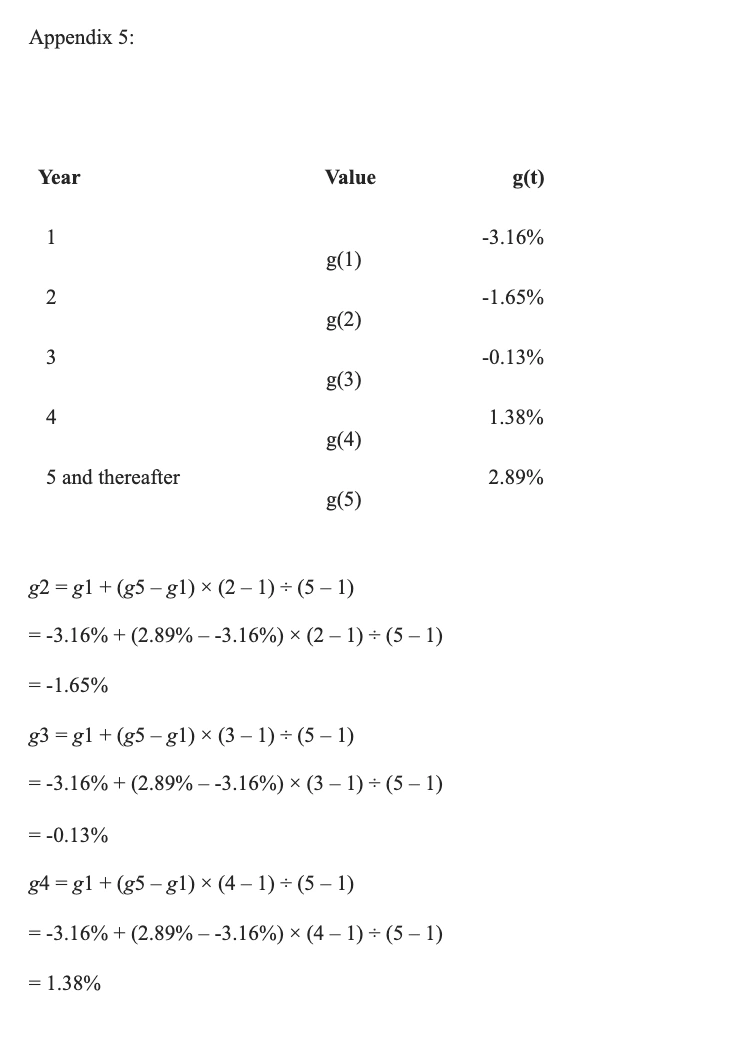

Furthermore, I calculated the average return on a ten year U.S treasury bond that came out to an average of 2.01%. The expected rate of return on a market portfolio was found to be 11.51%. I used this information along with the beta that was previously computed to calculate the required rate of return for Merck’s common stock. The rate of return was found to be 5.97%. Merck’s financial data from their 10-K filing was used to calculate the dividend growth rate using the PRAT Model that came out to be -3.16%. I also used the Gordon Growth Model and took the current price of share of Merck’s common stock and the last year's dividends per share along with the required rate of return to calculate the growth rate of 2.89%. The PRAT and Gordon Growth Model growth rates were then used to calculate the growth rates for years 2, 3, and 4 as shown in appendix 5.

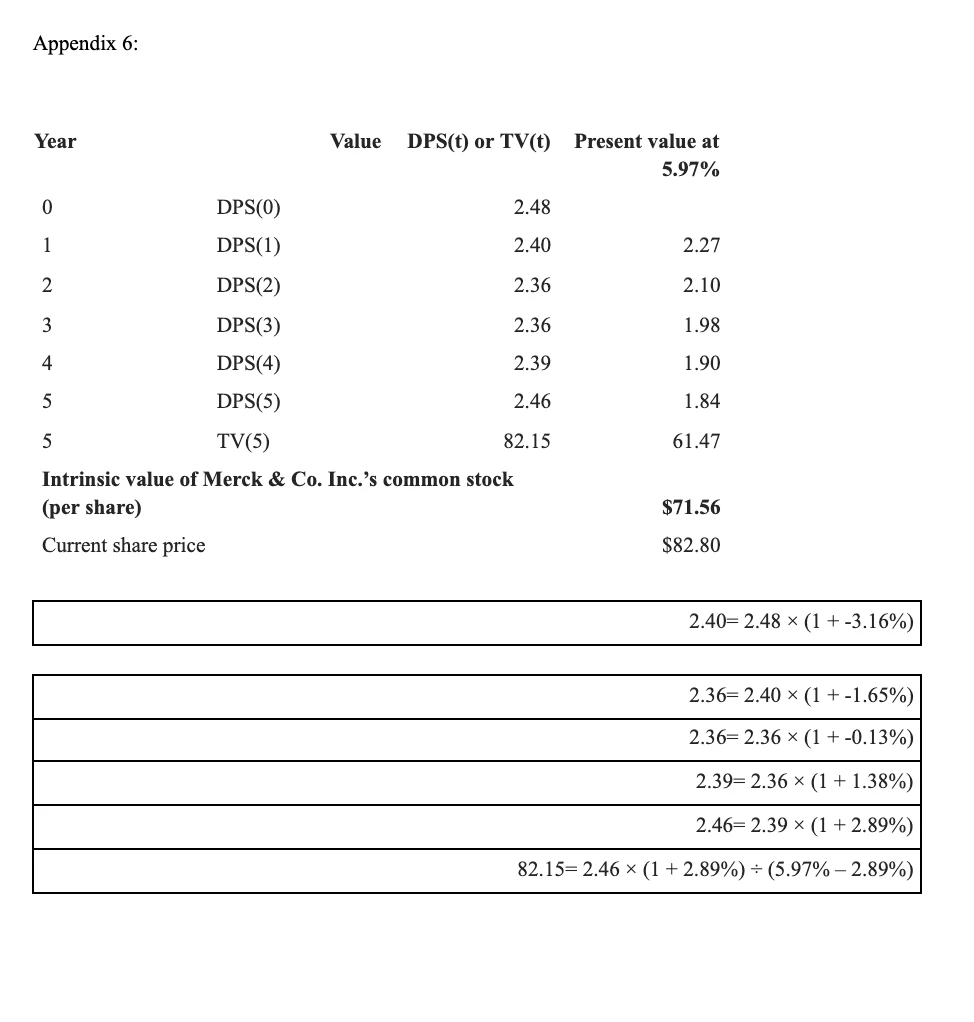

Finally, I was able to compute the expected value per share for Merck’s stock that totalled $71.56. This was calculated by taking the rate of return for the previous year which was $2.48 and using this amount along with the betas that were previously calculated in appendix 5. The totals were discounted at a rate of return of 5.97%, that was previously calculated. The calculations can be found below in appendix 6.

Recommendation

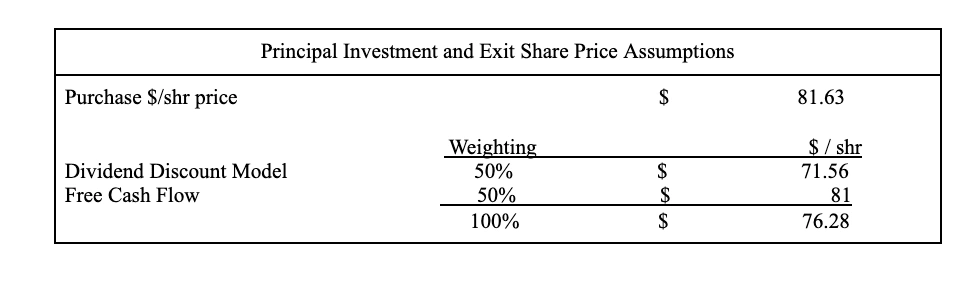

Based on the models used, I obtained a price of $71.56 from dividend discount model and $102.02 from EBITDA market multiple valuation. As this is 10 years out, I want to be conservative by splitting the difference 50/50 and calling it $86.79 (Appendix 9). I would be issuing a “HOLD” for Merck and Co. Over the next few years, with a string of advanced drug manufacturing technologies and diversified portfolio of products, especially some outstanding drugs like Keytruda, Januvina, etc, I am confident in this stock and waiting for its breakthrough. The company has always focused on the segment of intensive development of disease prevention and treatment initiatives, hence I believe I should hold this stock for the short-term period.

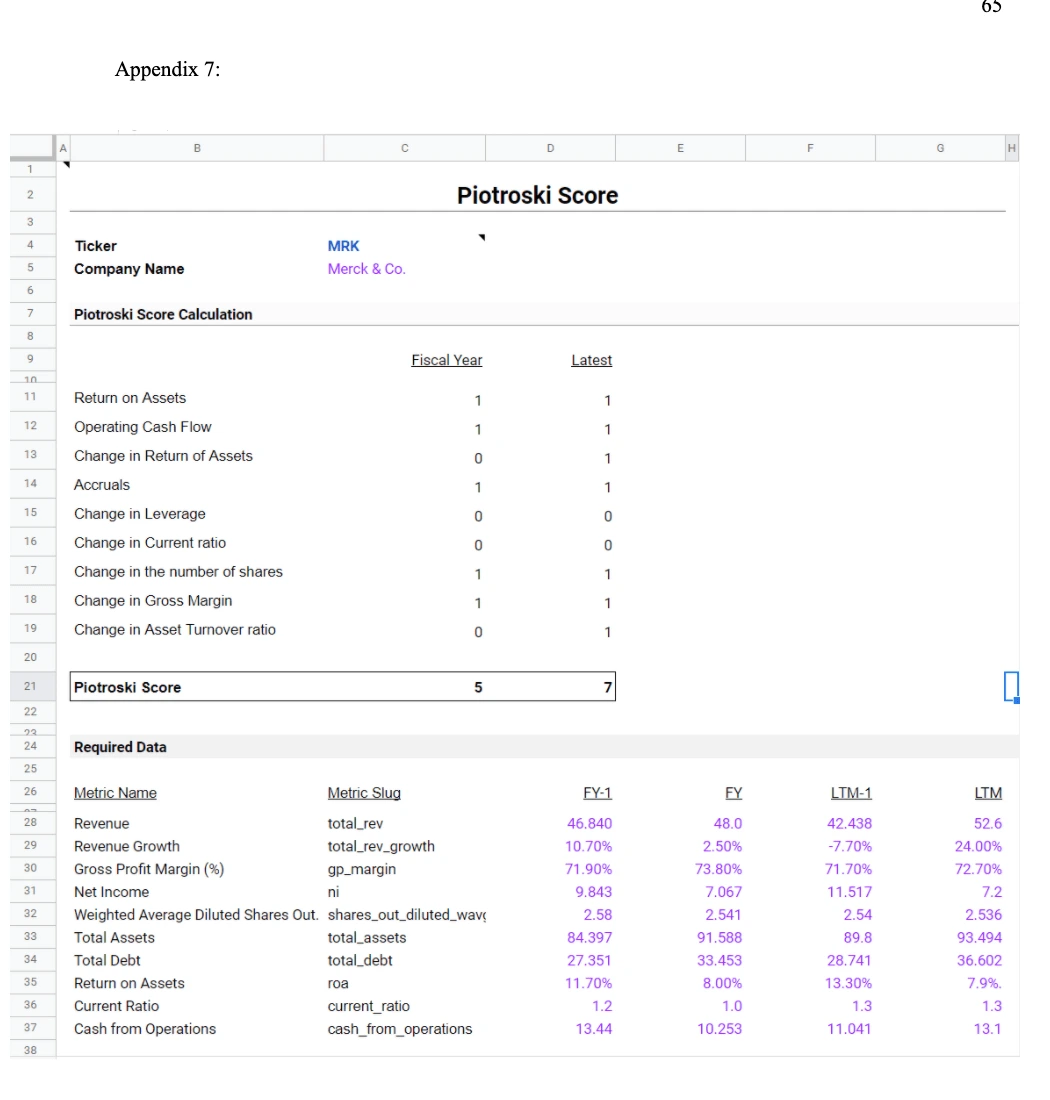

I recognize the fact that Merk has a fairly strong financial position and valuable stock in the upcoming years based on Piotroski F-Score. This is a popular financial indicator that puts together nine criteria to evaluate the financial strength of Merck Company based on its profitability, leverage, liquidity, source of funds, and operating efficiency. Scores of 8 and 9 are usually classified as strong value stocks, whereas scores of 2 or below are considered weak value stocks. Some research analysts and sophisticated value traders use Piotroski F-Score to find opportunities outside of the conventional market and financial statement analysis. They believe that some of the new information about Merck's financial position does not get reflected in the current market share price, suggesting a possibility of arbitrage. Based on Appendix 7, if we look at the fiscal year 2020, the Piotroski score is only average (5 points), but when we jump to the current 3rd quarter, the score has clearly developed.

References

Merck & co inc (MRK) - financial and strategic SWOT analysis review. (2020). London: GlobalData plc. Retrieved from ABI/INFORM Collection. https://ezproxy.csusm.edu/login?auth=shibboleth&url=https://www.proquest.com/reports/merck-amp-co-inc-mrk-financial-strategic-swot/docview/2476816777/se-2?accountid=10363

Pharm Approach. (2020, November 21). 15 astonishing statistics and facts about U.S. Pharmaceutical Industry. Pharmapproach.com. Retrieved November 25, 2021, from https://www.pharmapproach.com/15-astonishing-statistics-and-facts-about-u-s-pharmaceutical-industry/#:~:text=In%202019%2C%20the%20United%20States,of%20the%20global%20pharmaceutical%20market.

Medicaid Drug Rebate Program (MDRP). Medicaid. (n.d.). Retrieved November 24, 2021, from https://www.medicaid.gov/medicaid/prescription-drugs/medicaid-drug-rebate-program/index.html.

“S&P 500 Historical Data.” Retrieved from https://finance.yahoo.com/quote/%5EGSPC/history/

“Merck & Co., Inc. (MRK) Historical Data.” Retrieved from https://finance.yahoo.com/quote/MRK/history?p=MRK

Jiang, L. (2011). Essays on stock return predictability and market efficiency. Available from ABI/INFORM Collection; ProQuest Dissertations & Theses Global: The Humanities and Social Sciences Collection. (879771681). Retrieved from https://ezproxy.csusm.edu/login?auth=shibboleth&url=https://www.proquest.com/dissertations-theses/essays-on-stock-return-predictability-market/docview/879771681/se-2?accountid=10363

Health Sector Economic Indicators: Insights from Monthly National Health Spending Data through May 2021. (2021). Altarum. Retrieved from

Like this project

Posted Dec 18, 2021

The paper advises holding Merck and Co. at $86.79, citing confidence in advanced technologies, diverse products, and improving financials.