Designing the Pix experience for Neon Bank

Marcelus Fernandes

Design strategy to facilitate the Pix adoption and lower the learning curve to increase the product penetration on record time

·

Context

By July 2020 I had recently joined Neon and I was welcomed with an amazing challenge: Design the Pix Experience for Neon and MEI Fácil. It was a very ambiguous challenge with strict constraints. Pix is heavily regulated by the Central Bank and they defined strictly go-live dates. By the time I joined Neon to deliver both Pix experiences I had a little more than 6 weeks and the team was about to be hired yet.

What is Pix?

Pix is an instant payment method powered by the Central Bank through APIs and strictly experience requirements. In 2020 It was an obligation to Payments Institution and licensed banks. Pix is a step towards the Open Banking initiative, by taking control of the APIs the Central Bank promotes competition and the creation of better products for consumers. It also will remove the middleman on transactions allowing instant transactions (10s) at any time, any day, and free of charge (merchants will need to pay a very small fee comparing to other payment methods).

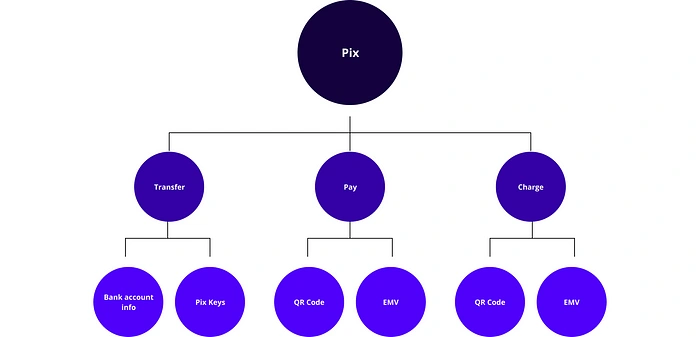

It will allow you to perform transactions using an alias, Pix Keys, and also charging any amount of money through QR Codes.

Simplifying all the paragraphs, this is work Pix works.

Research time!

Time was the worst constraint we had so I needed to be creative to gather the information I need and find the design challenge behind the formal request. So I triangulate the insights using articles, 3rd-party research, Government research, Consulting reports, Reverse engineering benchmarks, interviewing stakeholders, and watching market specialist talks about the topic. It was challenging to get all the pieces together and come out with actionable insights in such a short time but we managed to nail it.

Miro is our best friend on the “Thinking fast” part of the process.

1. Finding the first clues

So, to find the starting point I reduct Pix to its essential meaning, It gave me 2 clues, I should understand about payment methods and digital payments.

At that time market specialists and the Central Bank team were sure that Pix would have a huge impact on debit at first, the analysis allowed me to bet against the market specialists showing that actually, TED and DOC would die first. After launch, the bet proved right, and you can see it

(Portuguese only, sorry).

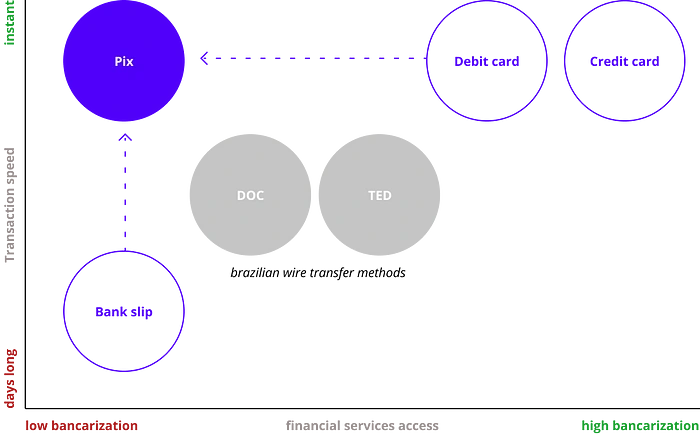

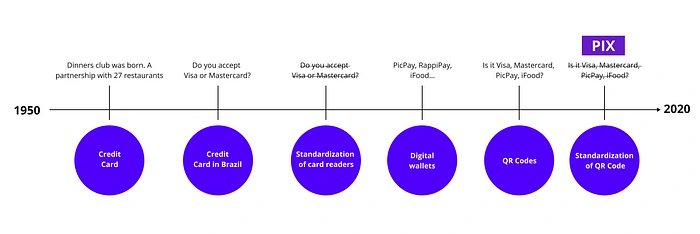

Payment methods

Reading about the current payments It was possible to see how Pix fits into 2 relevant characteristics: Transaction speed and Access to financial services. That view could tell me the potential adoption of the Brazilian market. Official research pointed out that 29% of the Brazilian population has a low level of bancarization, so Pix is a great opportunity to bring these people onboarding. And also understand how it compares with other methods.

At that time market specialists and the Central Bank team were sure that Pix would have a huge impact on debit at first, the analysis allowed me to bet against the market specialists showing that actually, TED and DOC would die first. After launch, the bet proved right, and you can see it here (Portuguese only, sorry).

Digital Payments

QR Codes are not new, actually, they are in the Brazilian market since 2012 on digital wallets. The pandemic scenario helped to bring more awareness about this payment method but even relevant players spending a mountain of cash on marketing, cashback, and all kind of rewards, QR Codes are still not a top-of-mind payment on the market. Reports showed that 95% of consumers believe that the market is not ready to accept digital payments.

The fragmented pieces allowed us to identify an interesting pattern:

By understanding the history of the Credit card we could see a pattern, the QR Codes were facing the same problem and Pix would remove a huge barrier to make it work.

2. The users

To deal with the time constraints and regulatory deadlines I had to work with non-linear research. The initial knowledge about the users came from past researches but I still need to find out the adoption mindsets we have to understand the right levers on the experience.

To get to where I wanted I used a mix-method of Generative In-depth interviews + Moderated usability tests (Central bank defined experience requirement, It allowed me to create hypothetical flows and scenarios to test). I wanted to understand behavior and motivations before validating interactions. The generative research would point me to the right thing while the usability test showed me if I was doing the things right.

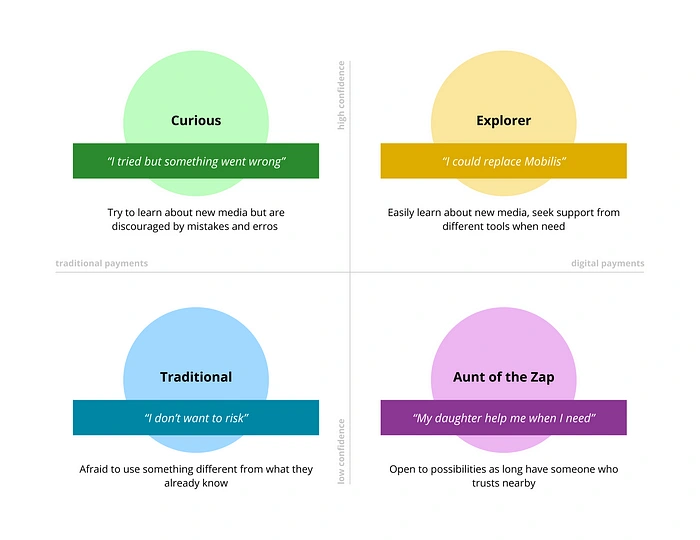

Adoption mindsets

I strongly believe that mindsets are key to understand human behavior and promote behavioral changes. This is the reason I built it instead of Personas.

These mindsets were built under 2 pillars: Digital payment (a fact, a question on recruitment) and Confidence (Subjective, observed on the interviews. It means how the person feels confident to learn and engage with new digital solutions).

Each mindset has its own needs and goals, that view allowed us to understand how to deal with them and helped to define the real challenge and pix goals. Besides the particular needs, they all had one thing in common, people don’t want a feature, they want to move money from point A to B fast, cheap, and safely.

3. Design challenge

Summing up the context, market research, and mindsets we frame the design challenge as:

How to facilitate Pix adoption and lower the learning curve to increase the product penetration on record time

4. Defining the solution

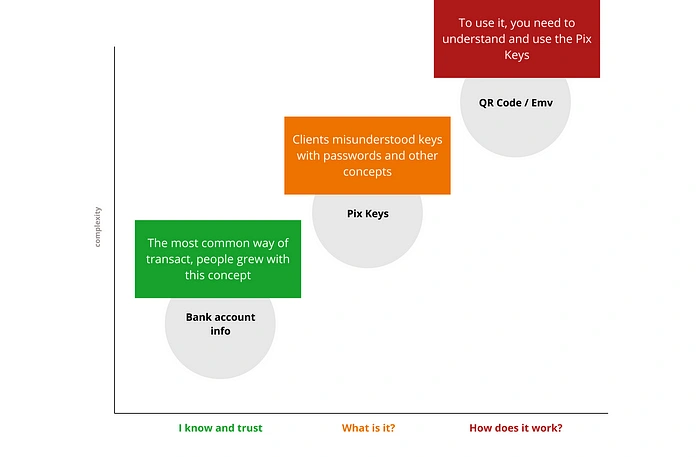

To understand the steps we need to take to facilitate the adoption I brought what we learned about payment methods mixing with the Pix methods and it gave me this view over Complexity x Familiarity:

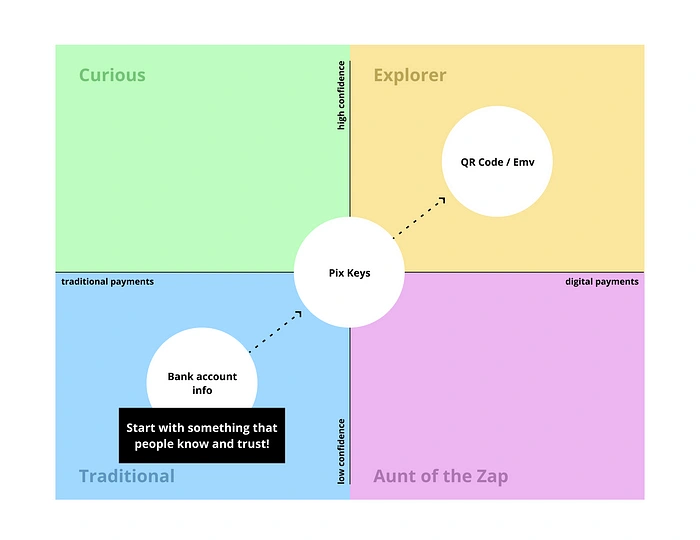

And when you merge the payment methods view with the mindsets, we have a map on how to create the Pix experience smoothness. We should focus the initial experience on something that customers know and trust, something that wouldn’t trigger any fear or need to understand the tool.

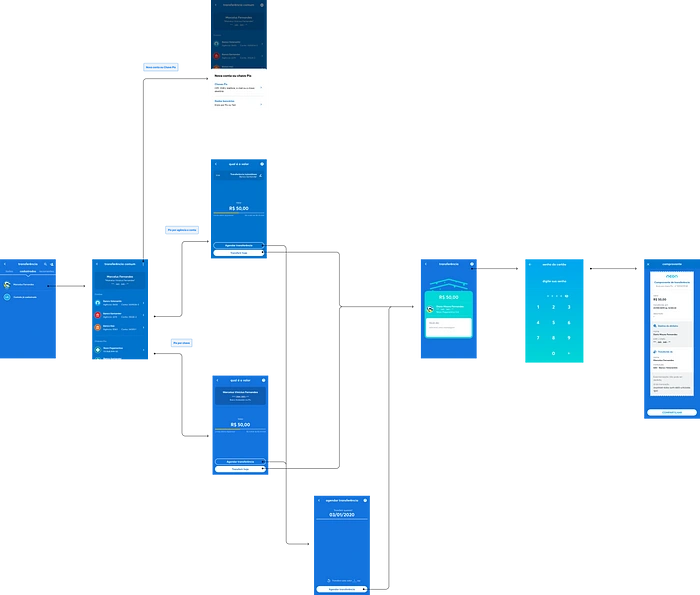

6. Designing the solution

To facilitate the adoption experience we would need to remove the complexity of learning, trusting in a new tool. While all the market was talking about Pix Keys we understood that users don’t want to make a Pix, they want the money going from point A to B fast and cheap. So we avoided using the name Pix and merged the wire transfer with the pix experience offering two options: Instant transfer and Normal transfer. Even not asking anyone to make a Pix on the usability tests, that approach gave us 100% of people following the expected path. It was a success.

Even with a heavy regulation defining the experience we created a strategy to design a unique experience with a strong differentiator. That approach led us to achieve 2x the goal (Product penetration and registered Pix Keys), providing a huge business impact on the reduction of transactional costs and increase the TPV.

Last chance! 6 days left to get 20% off membership.

Free

Distraction-free reading. No ads.

Organize your knowledge with lists and highlights.

Tell your story. Find your audience.

Membership

Get 20% off

Read member-only stories

Support writers you read most

Earn money for your writing

Listen to audio narrations

Read offline with the Medium app

Like this project

Posted Aug 12, 2024

By July 2020 I had recently joined Neon and I was welcomed with an amazing challenge: Design the Pix Experience for Neon and MEI Fácil. It was a very ambiguous…

Likes

0

Views

15