The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Back to feedPost

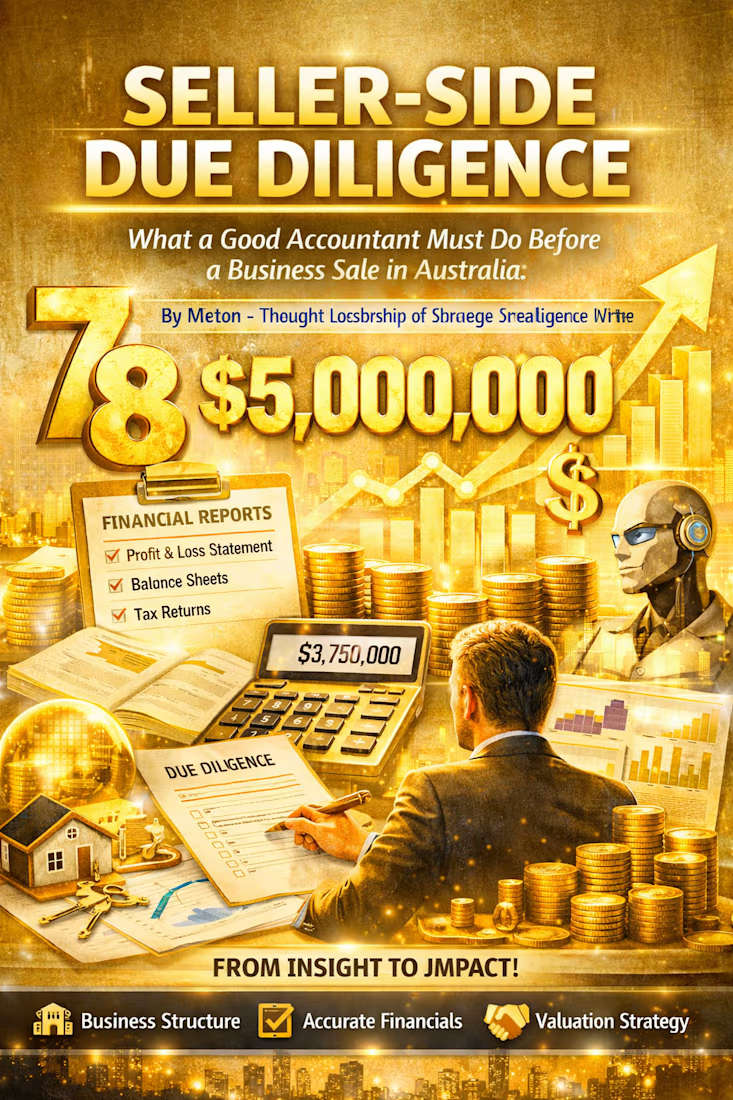

Seller‑Side Due Diligence: What a Good Accountant Must Do Before a Business Sale in Australia

Selling a business in Australia is one of the most significant financial events a small‑to‑medium business owner will ever experience. It’s not just a transaction — it’s the culmination of years (sometimes decades) of work, risk, sacrifice, and personal investment. As an accountant acting for the seller, my role is to ensure the business is presented with clarity, accuracy, and defensible financial logic. That means preparing the business for scrutiny before the buyer even begins theirs.

This process is known as seller‑side due diligence, and when done properly, it protects the seller, strengthens valuation, reduces negotiation friction, and increases the likelihood of a clean, successful sale.

With 15 years in Australian tax, business services, and forensic accounting, I’ve learned that seller‑side due diligence is not just about numbers — it’s about narrative, transparency, and anticipating the questions a sophisticated buyer (or their accountant) will ask. Below is the framework I use when preparing a business for sale.

1. Understanding the Entity Structure — The Foundation of Everything

Before touching a spreadsheet, I need to understand how the business is structured, because the entity type determines:

how goodwill is treated

whether CGT concessions apply

how assets are transferred

what liabilities follow the sale

whether the owner’s personal assets are exposed

how the sale price is allocated

In Australia, small businesses are commonly structured as:

Sole traders

Partnerships

Discretionary or unit trusts

Pty Ltd companies

Each structure has different tax consequences. For example, a sole trader selling a business they’ve operated for over 15 years may be eligible for the Small Business 15‑Year CGT Exemption, which can eliminate capital gains tax entirely if conditions are met. A company, however, may need to consider the 50% active asset reduction, retirement exemption, or rollover provisions instead.

Understanding the structure early allows me to shape the sale strategy, the valuation narrative, and the tax planning opportunities available.

2. Preparing the Financial Core — The Documents No Buyer Will Proceed Without

A buyer’s accountant will always ask for the same foundational documents. If the seller cannot provide them quickly and cleanly, confidence drops and valuation suffers.

The essential documents include:

Profit & Loss Statements (3–4 years minimum)

Balance Sheets for the same period

Tax Returns (entity and individual, where relevant)

BAS statements

General ledger extracts

Depreciation schedules

Asset registers

Loan agreements and finance schedules

Employee entitlement summaries

Superannuation compliance records

Tax returns are particularly important because they show actual tax depreciation, not just accounting depreciation. Buyers look for consistency between accounting profit and taxable income — discrepancies must be explained.

If the financials are unaudited, I perform a forensic-style review to ensure accuracy, identify anomalies, and prepare explanations before the buyer asks.

3. Normalising Earnings — The Heart of Valuation

Most small businesses have discretionary expenses, owner wages, or one‑off costs that distort true profitability. As the seller’s accountant, I prepare a normalised earnings statement that adjusts for:

owner’s salary (if above or below market)

personal expenses run through the business

one‑off legal or repair costs

non‑recurring revenue

related‑party transactions

abnormal stock adjustments

private vehicle or travel expenses

This is where forensic accounting skills matter. Buyers want to see sustainable, repeatable earnings, not inflated numbers. My job is to present a fair, defensible picture that supports the seller’s valuation without crossing into exaggeration.

4. Trend Analysis — Showing the Story Behind the Numbers

A single year’s profit means nothing without context. I analyse:

revenue growth or decline

margin stability

customer concentration

seasonality

cost trends

cashflow patterns

debtor and creditor movements

A business with stable margins and predictable cashflow commands a higher valuation. A business with volatile revenue needs explanation.

Trend analysis also helps identify risks before the buyer does. If revenue dipped in one year, I prepare the explanation upfront — new competitor, owner illness, supply chain issue, etc. Transparency builds trust.

5. Reviewing Contracts, Leases, and Operational Dependencies

Financials tell one story; contracts tell another. I review:

customer contracts (especially if one client represents >20% of revenue)

supplier agreements

equipment leases

property leases

insurance policies

licences and permits

intellectual property documentation

Buyers want to know:

what obligations they’re inheriting

whether key relationships are secure

whether the business can operate without the current owner

If the business relies heavily on the owner’s personal relationships, I highlight this early and help the seller prepare a transition plan.

6. Employee Entitlements and ATO Compliance

Employee liabilities are a major due‑diligence focus. I verify:

annual leave

long service leave

superannuation payments

payroll tax

workers compensation

award compliance

Superannuation compliance is critical. Any unpaid super is a red flag that can derail a sale.

I also check for ATO payment plans, outstanding BAS, or historical issues. Buyers will find them — better that I prepare the explanation first.

7. Valuation Scenarios — Presenting a Range, Not a Guess

A good accountant never presents a single valuation number. Instead, I prepare valuation scenarios, such as:

valuation based on normalised EBITDA

valuation based on net tangible assets

valuation based on discounted future cashflow

valuation after applying CGT concessions

valuation after adjusting for working capital

This gives the seller a realistic range and prepares them for negotiation.

8. Capital Gains Tax Planning — The 15‑Year Concession and Other Small Business Reliefs

For many small business owners, CGT is the biggest financial event of their life. Australia’s Small Business CGT Concessions can dramatically reduce or eliminate tax on the sale.

Key concessions include:

15‑Year Exemption — if the business has been owned for 15+ years and the owner is over 55 and retiring, the entire capital gain may be tax‑free.

50% Active Asset Reduction — reduces the capital gain by half.

Retirement Exemption — up to $500,000 can be contributed to super tax‑free.

Small Business Rollover — defers CGT if proceeds are reinvested in another active asset.

My role is to determine eligibility early, model the tax outcomes, and structure the sale to maximise concessions.

9. Preparing the Business Overview — The Document Buyers Actually Read

Once the financial and operational due diligence is complete, I prepare a business overview that includes:

business history

revenue breakdown

customer profile

operational structure

financial highlights

normalised earnings

valuation summary

risk factors

transition plan

This is the document the buyer reads before deciding whether to proceed to formal due diligence.

A clear, honest overview builds trust and positions the seller as organised and credible.

10. Anticipating Buyer Questions — The Forensic Mindset

Finally, I prepare the seller for the questions buyers will ask, such as:

Why are you selling?

What would happen if you stepped away tomorrow?

Are there any disputes, liabilities, or compliance issues?

How dependent is the business on key staff or customers?

What risks should we be aware of?

A seller who answers confidently and transparently is far more likely to secure a strong offer.

Closing Thoughts

Seller‑side due diligence is not about making the business look perfect — it’s about presenting it honestly, clearly, and professionally. When the financials are clean, the narrative is coherent, and the risks are acknowledged upfront, buyers feel safer, negotiations run smoother, and valuations hold firm.

As an accountant with experience in business sales, forensic analysis, and Australian tax law, my goal is simple: protect the seller, strengthen their position, and ensure the business is presented with the clarity it deserves.

__________________________________________________________________

Written by Victor Tyan MIntBus, BComm

duediligencefinancesaleofpropertyAccountingCreative StrategistAI Copywriting Content StrategyArticle WritingGhostwritingClaudeGoogle DriveNotion

The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Trending

Claude

Claude has entered the design space. How are you using it?

Contra University

Learn from expert creatives how to earn more using next-gen AI tools.

Brand Design

The best brand designers are on Contra. Scroll to see what's trending in brand design. What are you building?

creativeaiflow

Creative AI workflows are evolving. What tools do you use, and what are their strengths and weaknesses?

freelancerlife

Freelancer life is wins, pivots, and everything in between. What’s yours right now?

Related posts

Clean about section for Ledgerfy

What do you think about this style?

nice work 😊

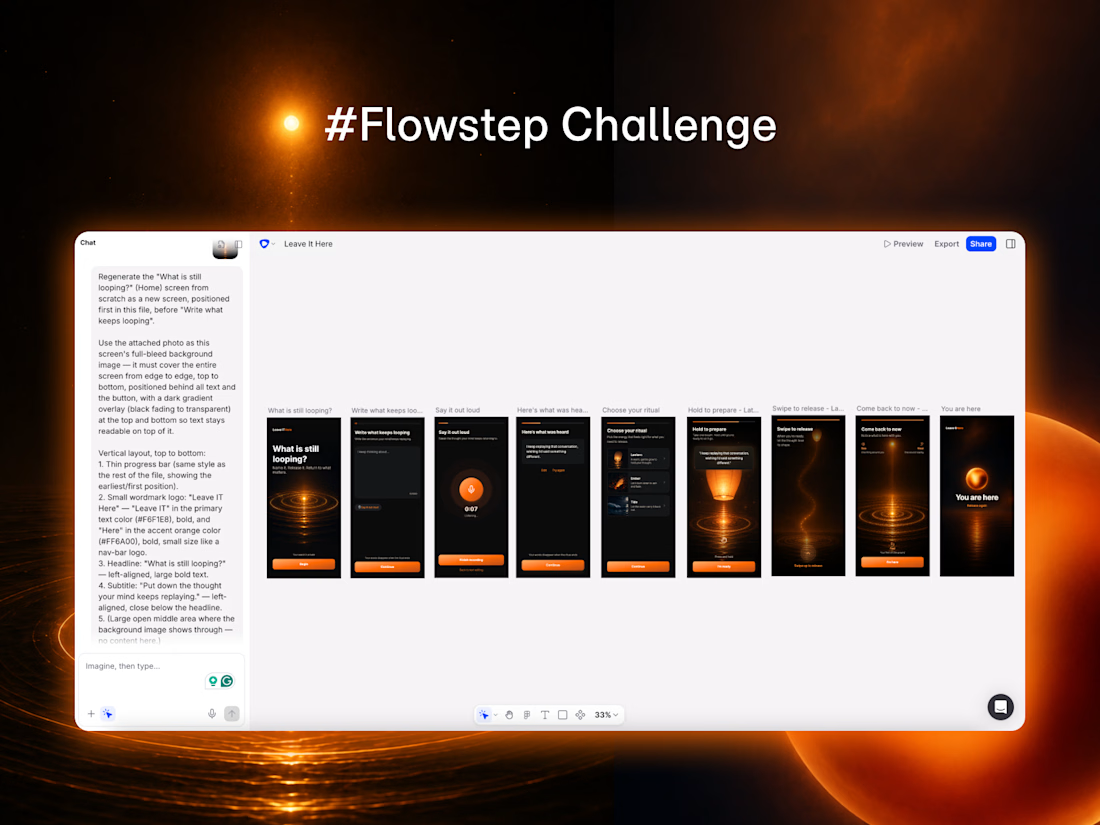

"Leave It Here" is a digital ritual for thoughts that keep looping in your mind.

I created this concept from a personal experience: when a conversation or situation hurts or unsettles me, I often replay it again and again (sometimes I can't even sleep), thinking about what happened or what I should have said or done differently.

🔮 How I used Flowstep

While working in Flowstep, I created a set of design guidelines and continuously refined them to keep the experience consistent across typography, color, spacing, tone, and interaction. I used prompting for larger changes and refined the smaller details manually, including images, texts, and button colors.

🚀 What I liked the most

I especially liked the automatic screen connections, clickable prototyping, and additional interaction states generated by Flowstep.

🔗 Prototype link

https://app.flowstep.ai/file?activeFileId=f87f9bcd-57ee-49af-a879-383ac20301cc

P.S. The prototype currently opens on the second screen instead of the intended first screen. The first screen was created later in the workflow, and I could not find a way to redefine the starting point. Flowstep team, I would really appreciate your advice on this.

💻 Thank you, Contra and Flowstep, for creating this challenge and giving me the opportunity to bring this idea to life!

Concepts built around a real feeling instead of a business use case usually turn out more polished. every design decision has something real to check against instead of just a guess

Static images out of Midjourney and Reve. Brought it into Fable and animated the windows on.

Wow... this is neat