How to Create an Emergency Budget to Deal With COVID-19

Tulie Finley-Moise

Save more, spend smarter, and make your money go further

This content is for the first stimulus relief package, The Coronavirus Aid, Relief and Economic Security Act (The CARES Act), which was signed into law in March 2020. Looking for the latest news on the stimulus relief package? For more information on The American Rescue Plan, the stimulus relief package which was signed into law in March 2021, please visit the “American Rescue Plan: What Does it Mean for You and a Third Stimulus Check” blog post.

COVID-19 has made a profound impact on many individual lives and economies across the globe. With businesses shifting to remote operations, restaurant doors shuttered, and a down stock market, the shutdown of much of the U.S. economy has affected millions of Americans. Since the all coronavirus outbreak touched down in the U.S., over 10 million Americans have filed for unemployment in hopes of recouping their recent loss of income.

If you’re like many Americans dealing with the current COVID-19 crisis, you’re likely concerned about your finances. Whether or not your paycheck or lifestyle has been affected by the pandemic, it’s important to retain financial stability during such a time of uncertainty. The best way to avoid a financial emergency is to prepare an emergency budget that works for you and your household.

Protecting your finances amidst a global pandemic may seem like an impossible feat, but with the right budget in place, you can properly prepare yourself for any unforeseen expenses that may come your way. Using this guide, we’ll walk you through how to create an emergency budget and gain the peace of mind you deserve during these unprecedented times.

What is an emergency budget?

At its very core, an emergency budget prioritizes survival above all else. Though similar to your average weekly or monthly budget, an emergency budget is one that eliminates all unnecessary expenses and solely accounts for your basic needs and financial responsibilities.

When used effectively, an emergency budget can provide extra financial leeway that allows you to deposit more into an emergency fund or simply stretch your money longer. Cutting costs and reprioritizing expenses is a reality many Americans are facing today as COVID-19 applies pressure to their financial well-being.

Due to the unpredictable nature of coronavirus, expecting the unexpected must be an integral piece of your budget-planning puzzle. Ultimately, your emergency budget should account for costs required to make ends meet and all leftover earnings should be put toward an emergency fund.

How to create an emergency budget: A step by step guide

Creating an emergency budget is a lot like creating your usual monthly budget, however, instead of allocating funding for ancillary expenses like a gym membership or restaurant dinners, your focus is more positioned on how to cover basic needs and dedicate the rest to securing your future stability.

Grab a calculator and have your old budget plans handy—let’s break down how to create an emergency budget, step by step.

Step 1: Assess your current budget

In order to create a successful emergency budget, you should first understand the state of your pre-pandemic finances. Your existing budget will reveal all you need to know about your current spending and where your money is going.

List out all of your monthly expenses, including both recurring and variable costs as well as needs and wants. To get a bigger-picture view of these charges, it may help to review your Mint transactions, monthly bank or credit card statements. Add up the sum of these expenses to calculate your monthly spending.

Now, compare your monthly spending with your current income. This is especially critical if you have recently become unemployed or have taken a pay cut. This comparison will give you an accurate look at how you’ll need to modify your spending to accommodate your basic needs while allocating residual income toward future spending or an emergency fund.

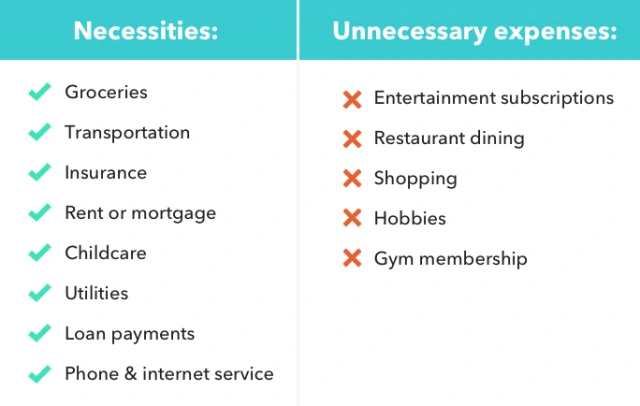

Step 2: Divide your expenses

Once you’ve developed a comprehensive list of your monthly expenses, divvy them up into two categories: necessities and unnecessary expenses. Because lifestyle essentials vary from person to person, it’s up to you to determine your needs from your wants. Keep in mind that the more wants you’re able to give up, the more money you’ll have to put toward needs in the future.

To help you get started, use these lists of common necessities and unnecessary expenses:

Necessities – Also commonly referred to as fixed expenses, necessities include everything that ensures your basic needs are met. Examples include:

Groceries

Transportation

Insurance

Rent or mortgage

Childcare

Utilities

Loan payments

Basic Phone and internet service

Unnecessary expenses – Embodied by costs for things you can live without, unnecessary expenses should be the first to be removed or reassessed when carving out your emergency budget. Examples include:

Entertainment subscriptions (streaming, gaming, etc.)

Restaurant dining

Shopping

Hobbies

Gym membership

Step 3: Adjust your budget

With a visual understanding of how your finances are divided up amongst needs and wants, you can make smarter, more calculated decisions as you develop your emergency budget. Whether you’re going through financial hardship or not, it’s important to make the necessary budget adjustments to protect yourself from going into the negative in the event of a medical emergency or life-changing curveball.

Reconstructing your budget means determining which expenses to keep or cut, and figuring out ways to lower recurring fixed expenses. Let’s walk you through it.

Decide what expenses to keep or cut

The criteria you’ll use to determine which expenses you’ll maintain versus expenses you’ll eliminate is completely up to your discretion, but keep in mind that the more nonessential costs you’re able to cut, the better.

This may mean canceling your streaming service subscriptions and yoga studio memberships in favor of funding next month’s budget for groceries.

With much of the country under stay-at-home orders, ousting restaurant dining, gym memberships and nightlife expenses should be relatively easy as most of these establishments are no longer open to the public. In light of this change, put your best foot forward to turn a restrictive situation into one of growth. Dust off an old board game to substitute your pricier entertainment methods or try out a new recipe to satiate your craving for fine dining.

The vast majority of your necessities will likely remain as such in your modified emergency budget and should always be the priority expenses each and every month moving forward.

Lower fixed expenses

Once you’ve eliminated all gratuitous expenses, you can better define the details of your emergency budget. Go through your list of surviving expenses and survey which costs can be lowered. You may be surprised to find just how many fixed costs can actually be lowered to better accommodate your time of financial hardship.

Unbeknownst to most, many utility companies, cable companies, and cell phone providers will be happy to work with you in finding a more economical plan that ensures you remain a loyal customer. Negotiating your bills takes a bit of know-how and persistence, but you may find that you’re able to save $10 or $100 on a recurring bill with a simple phone call.

Step 4: Explore available benefits

In light of the situation the coronavirus has placed on the American people, the federal government has extended help to those most vulnerable to the jarring effects. From stimulus packages and expanded unemployment benefits, there are a number of assistive measures available and in-progress that you may be eligible for.

As of March 30, 2020, the U.S. Internal Revenue Service has confirmed that tax filers with an adjusted gross income of $75,000 or less are qualified to receive the government-issued economic impact one-time payment of $1,200. Married couples who earn an AGI of $150,000 or less will be eligible to receive a check of $2,400, and up to $500 more for each qualifying child. As long as you have filed a tax return for the 2019 or 2018 year the IRS will calculate and send the payment to those eligible via direct deposit or a check in the mail.

Federal and state unemployment programs work together to provide financial assistance to those who have lost their jobs to no fault of their own. Signed into law on March 27, 2020, the Coronavirus Aid, Relief, and Economic Security (CARES) Act actively extends unemployment benefits to gig workers, freelancers, and furloughed employees.

The Pandemic Emergency Unemployment Compensation (PEUC) program allows workers who have depleted their unemployment compensation benefits to receive an additional 13 weeks of benefits. This program also extends benefits to those that are gig-workers, freelancers, and independent contractors.

Depending on your unique situation, you may qualify for a number of government assistance programs that may broaden the limits of your emergency budget plan.

Step 5: Reassess your financial goals

In the face of a potential financial emergency, the most important goal should be paying your most vital bills. For most, this likely means that any other goals will need to be paused for the foreseeable future to fully prioritize making ends meet for as long as possible until your regular income stream is restored.

Financial experts recommend having between three and twelve months’ worth of expenses stashed in an emergency fund to protect yourself from any bumps in the road and provide extra cushion through tough times. When reassessing your financial goals during COVID-19, narrow your focus on sticking to your emergency budget and building up an emergency fund.

Conclusion

During times of great uncertainty, keeping your finances in order is essential. Though there is no universal answer to how to handle financial hardship, there are a number of viable ways you can prepare for one. By using this emergency budget guide, you can take the necessary preventative measures to ensure you remain stable and secure throughout COVID-19.

Sign up for Mint today

From budgets and bills to free credit score and more, you’ll

discover the effortless way to stay on top of it all.

Like this project

Posted May 18, 2023

Use this step-by-step guide to create an emergency budget to help you weather the financial impacts of coronavirus.