Guide to Nigeria's 2026 Tax Law Changes

Oladele Steve

Nigeria’s New Tax Laws (2026): Your Complete Guide to What Changes and Why It Matters

The Bottom Line Before You Read

Starting January 1, 2026, Nigeria is implementing four new tax laws that represent the biggest tax system overhaul in decades. The headline: 98% of Nigerian workers and 97% of small businesses will pay little or no tax. However, there’s a catch: everyone earning any income now has to register, file returns, and keep detailed records. The government isn’t asking anymore; they’re watching.

If you earn money, whether as a salaried employee, freelancer, small business owner, or content creator, this will affect you. So let’s break down what’s actually happening in plain English.

Why Is Nigeria Doing This?

Nigeria’s tax system has been broken for a long time. Tax laws were scattered across dozens of different statutes, confusing for both taxpayers and the government. Small businesses operated informally to avoid the headache. Freelancers and digital workers didn’t file returns. And the government couldn’t track income flowing through digital platforms.

The result? The country’s tax-to-GDP ratio sits at less than 10%, one of the lowest in Africa. The government wants to raise it to 18% by 2027, not through higher taxes on the poor, but through wider participation. Everyone contributes a fair share based on their actual income.

These new laws consolidate everything into four clean, modern statutes designed for a digital economy. They make the rules clearer and aim to protect low-income earners while making sure nobody can slip through the cracks.

The Four New Laws

Nigeria Tax Act 2025 (NTA) — Covers income tax, VAT, capital gains, and all the actual tax rates and rules

Nigeria Tax Administration Act 2025 (NTAA) — The enforcement side: how to register, file, keep records, and what happens if you don’t comply

Nigeria Revenue Service (Establishment) Act 2025 — Creates the new Nigeria Revenue Service to replace FIRS

Joint Revenue Board (Establishment) Act 2025 — Coordinates tax between federal and state levels

The first two of these take effect January 1, 2026. The others already started in June 2025.

FOR INDIVIDUALS: WHAT THIS MEANS FOR YOUR PAYCHECK AND SIDE HUSTLE

The New Tax-Free Threshold

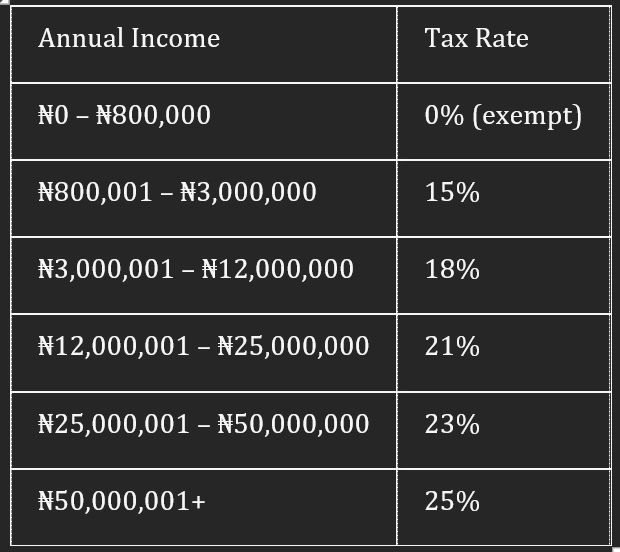

This is the good news. The government is raising the amount of money you can earn before paying any personal income tax. Starting January 1, 2026:

If you earn ₦800,000 per year or less, you pay 0% tax — nothing. You’re completely exempt.

If you earn above that, you enter a tax bracket system.

Here’s the full breakdown:

For example:

A teacher earning ₦45,000/month (₦540,000/year) → 0% tax

An accountant earning ₦100,000/month (₦1.2M/year) → Some of that is taxed at 15% (1,200,000 — 800,000 = 400,000) → 15% × ₦400,000 = ₦60,000

An executive earning ₦500,000/month (₦6M/year) → Falls into multiple brackets.

The government says about 98% of Nigerian workers will either pay zero tax or pay significantly less than before. The exemption threshold has basically doubled.

What About Deductions?

You don’t pay tax on your entire income. The government allows certain deductions that reduce your taxable income:

Standard deductions:

Pension contributions to your PFA (Pension Fund Administrator)

National Health Insurance Scheme contributions

National Housing Fund contributions

Rent relief: 20% of your annual rent, capped at ₦500,000

Example: : If you earn ₦2,000,000 per year and pay ₦600,000 in rent:

Rent relief: 20% × ₦600,000 = ₦120,000

Income after deductions: ₦2,000,000 — ₦120,000 = ₦1,880,000

Tax-free threshold: First ₦800,000 is exempt

Taxable portion: ₦1,880,000 — ₦800,000 = ₦1,080,000

Tax due: 15% × ₦1,080,000 = ₦162,000

Health insurance, life insurance, and home loan interest are also deductible if you have proper documentation.

The keyword: documentation. You need receipts, bank statements, and proof to claim these deductions.

“But Wait, What About My Side Hustle?”

This is where things change significantly. Under the old system, many side hustles went unreported. A designer taking freelance gigs, a content creator earning from TikTok, someone running a small POS business, all these were often kept off the books. But not anymore.

The new law has a simple rule: Every naira you receive is taxable unless the law specifically exempts it.

This includes:

✅ Freelance work (design, writing, coding)

✅ Content creation income (YouTube, TikTok, Instagram)

✅ POS/bill payment commissions

✅ Rental income (from rooms, property)

✅ Investment returns (dividends, interest)

✅ Capital gains (selling something for more than you bought it)

✅ Affiliate marketing, network marketing, betting commissions

✅ Cryptocurrency or digital asset gains

✅ Honoraria, prizes, and grants

The only income that remains completely untaxed:

Gifts from family

Legitimate compensation for loss of employment (up to ₦50 million)

Certain disability benefits and pensions

The critical difference: Capital gains and digital asset profits are now treated like regular income. In the past, cryptocurrency trading might have had a flat 10% tax. Now, gains are added to your income and taxed under the progressive bracket system, potentially at 25% if your total income is high enough.

Digital Enforcement: They Can See You Now

This is important: The tax authority now has legal access to your bank account data. How?

Your National Identification Number (NIN), which is linked to your bank account(s), is your tax ID.

Banks report transactions above certain thresholds to the tax authority.

The government has agreements with over 100 countries to exchange income information.

Google, Meta, and other platforms have agreements to report payments made to Nigerian creators.

What this means in practice: If you earn money through formal channels (bank transfers, digital platforms, payment apps), the tax authority can see it. If you receive ₦2 million from a freelance client through your account, they can see it. If you earn from YouTube ad revenue, they can see it.

Oyedele, the government’s tax reform chairman, was explicit about this: “If you earn money online, the platforms paying you number very few — Google, Facebook, and a few more. We can go to them for income reports.”

There’s no more hiding in the digital economy.

What about Freelancers and Remote Workers?

If you’re a freelancer or remote worker earning from a foreign company or platform, here’s what applies:

1. You must register for a Tax Identification Number (TIN) — Even if you already have one, ensure it’s properly linked to your NIN and bank account

2. You must file an annual tax return — Even if your income falls below ₦800,000 and you owe nothing, filing is mandatory

3. You can deduct legitimate business expenses:

Internet and data costs

Electricity and fuel

Software subscriptions and tools

Work-related equipment

Rent (up to ₦500,000 worth)

4. After deductions, if your income is below ₦800,000, you owe zero tax

5. If a client withholds tax from your payment, that counts as a credit against your total tax liability

Example: Freelance writer scenario

You earn ₦1,500,000 annually from writing for US-based clients.

Gross income: ₦1,500,000

Less: Internet, software, rent relief (combined): ₦400,000

Taxable income: ₦1,100,000

Tax at 15% on (₦1,100,000 — ₦800,000) = 15% × ₦300,000 = ₦45,000

That’s it. You owe ₦45,000 for the year. If your client withheld ₦10,000 in tax, you’d only owe ₦35,000 when you file.

FOR SMALL BUSINESSES AND SELF-EMPLOYED PEOPLE

The ₦100 Million Question: Are You a Small Business?

Under the new law, small businesses get massive breaks. Here’s the definition:

A small business has:

Annual turnover of ₦100 million or less, AND

Fixed assets of ₦250 million or less

If you meet both conditions, congratulations. You get:

✅ 0% Corporate Income Tax (completely exempt from paying CIT)

✅ 0% VAT (you don’t have to charge or collect VAT)

✅ 0% Withholding Tax (clients don’t have to deduct tax from payments to you)

✅ Exemption from the 4% Development Levy

✅ Reduced compliance burden (simpler record-keeping requirements compared to larger companies)

This exemption covers about 90% of Nigerian businesses

For comparison:

Businesses earning ₦25m–₦100m turnover pay 20% corporate tax

Businesses earning over ₦100m pay 30% corporate tax

So if your small shop, salon, repair service, or consulting firm generates ₦50 million in turnover per year, you pay zero corporate tax.

Cryptocurrency and Digital Asset Businesses

If you run a fintech, VASP (Virtual Asset Service Provider), or digital payment platform, the law targets you specifically.

Taxable:

Your profits are taxed at 30% corporate tax

You must report all user transactions to the tax authority

Each transaction must include: date, amount, type of asset, user details

Penalties for non-compliance: ₦10 million in the first month of default, then ₦1 million per month thereafter.

If you earn crypto trading profits personally:

Capital gains are added to your income

Taxed at whatever rate your total income puts you in (up to 25%)

Capital Gains Tax Changes

Under the old system, capital gains had simpler, flatter treatment. The new system integrates them into personal income tax.

Examples of capital gains:

Selling property for more than you paid

Selling shares

Selling a business

Selling cryptocurrency or digital assets

Exemptions (completely tax-free):

Sale of your owner-occupied house (the one you live in)

Sale of personal items worth up to ₦5 million

Selling up to 2 personal vehicles per year

Stock gains below ₦150 million threshold or ₦10 million in gains per year (for investors with 99%+ exemption)

If you exceed these thresholds:

Gains are added to your other income

Taxed at your marginal rate (up to 25%)

OR you get a “reinvestment relief” if you reinvest the proceeds

Keeping Records: You Need Digital Proof Now

Under the new law, you must maintain accurate, auditable records of all transactions. This isn’t optional.

Records you must keep:

Daily sales/revenue records

Invoices and receipts

Employee payroll and deductions

Expense documentation

Bank statements

Tax payment receipts

In what format?

Digital records are strongly preferred

Transaction dates, amounts, and descriptions

Clear categorization (what type of income/expense)

How long?

Generally, keep records for at least 5 years

The penalty if you don’t keep proper records:

₦10,000 for individuals

₦50,000 for companies

WHAT YOU NEED TO DO BEFORE JANUARY 1, 2026

Step 1: Get Your Tax Identification Number (TIN)

If you already have one: Verify it’s linked to your NIN at tat.gov.ng. No further action needed.

If you don’t have one:

Go to tat.gov.ng or use the JTB mobile app

Click “Register for TIN”

Choose “Individual TIN Registration” or “Business Name” depending on whether you’re registering as a person or sole proprietor

Enter required information: NIN/BVN, date of birth, phone, email, occupation, address

Click the verification box and submit

You’ll receive your TIN via email within days (sometimes immediately)

That’s it. Your NIN automatically becomes your Tax ID.

For registered companies:

Your CAC RC number automatically becomes your Tax ID

No separate registration needed

Step 2: Open or Separate Your Business Bank Account

If you’re self-employed or run a business:

Open a separate business bank account (don’t mix personal and business money)

Link this account to your TIN

Use this account exclusively for business transactions

Why? Makes your records clean. It’s easier to prove what’s business income versus personal money. During an audit, mixed accounts create confusion and increase your tax liability.

Step 3: Set Up Digital Record-Keeping

Start tracking:

Income: All money received, from all sources, with dates

Expenses: Everything you spend on the business

Bank statements: Monthly records

Tools you can use:

Excel spreadsheet (simple but works)

Accounting software (Wave, Zoho Books, XPresso — some are free)

Your bank’s mobile app (already captures transactions)

Step 4: Understand Your Tax Bracket

Calculate: What’s my total annual income after deductions?

Then find yourself in the tax bracket table above. This tells you your tax rate. If you’re a salaried employee, your HR department should handle this automatically with PAYE withholding from your salary.

If you’re self-employed or freelance, you’ll calculate it yourself and file a return.

You can calculate how much you will pay as tax using this official website: Personal Income Tax Calculator – fiscalreforms.ng

Step 5: Gather Deduction Documentation

Collect proof of anything you want to deduct:

Rent: Lease agreement and payment receipts

Healthcare: Insurance premium receipts

Pension contributions: PFA statements

Work expenses: Receipts for equipment, software, supplies

You’ll need these when you file your return.

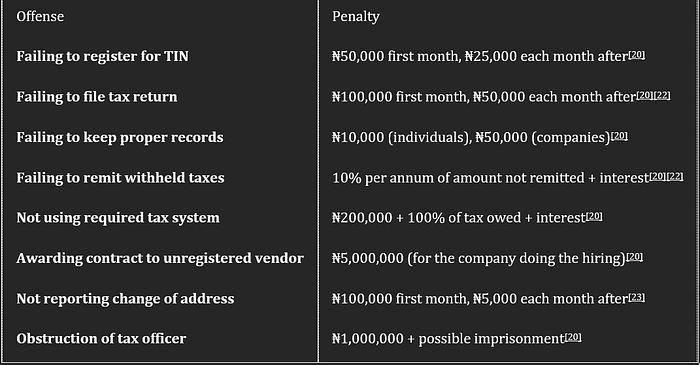

THE PENALTIES: WHAT HAPPENS IF YOU DON’T COMPLY

Administrative Penalties (Money Fines)

Criminal Penalties (Prison)

Serious violations can result in imprisonment:

Submitting false documents: Up to 3 years in prison or ₦1 million fine

Fraud related to taxes: Up to 3 years in prison + fine equal to principal amount + 50% penalty

Obstruction of tax officer with weapon: Up to 5 years in prison

Bribery of tax officer: Up to 3 years in prison + ₦500,000 fine

Not remitting withheld taxes: Up to 3 years + fine equal to principal + 50% penalty

Corporate officers (directors, managers, company secretaries) can face personal penalties for corporate tax violations.

MYTHS VS. REALITY: CLEARING UP THE CONFUSION

Myth 1: “My bank account will be frozen if I don’t have a Tax ID”

Reality: False. TIN is only required when opening new bank accounts. Your existing accounts are safe. The government said this explicitly to debunk rumors. However, for new accounts you open from January 2026 onward, you’ll need a Tax ID.

Myth 2: “Everyone earning under ₦800,000 is completely invisible to tax”

Reality: No. You’re exempt from paying tax, but you must still file a return. Filing puts you in good standing legally. If the government matches bank records and you haven’t filed, you face penalties for non-declaration.

Myth 3: “Small businesses can operate completely cash-based without records”

Reality: The law requires all businesses to maintain auditable records. “Digital enforcement” means the tax authority will cross-check bank accounts, fintech platforms, payment apps, and POS terminals. Cash-only operations increase audit risk.

Myth 4: “I can hide income by using cash”

Reality: No. With data linkage between tax authorities, banks, fintech platforms, and international agreements, large cash deposits and unexplained inflows raise red flags. The tax authority will ask where the money came from.

Myth 5: “Penalties are just threats; they’re never actually enforced”

Reality: The law transferred enforcement from FIRS to a new Nigeria Revenue Service with modernized systems and stronger digital tools. Early signs show the government is serious.

Myth 6: “Remote workers paying foreign taxes don’t owe Nigerian tax”

Reality: False. If you’re a Nigerian resident earning from abroad, the tax applies to your worldwide income. You may get a credit for foreign taxes paid, but you still owe tax in Nigeria

CONCLUSION

Nigeria’s new tax laws are complex, but the core message is simple: Everyone earns. Everyone registers. Everyone files. The system is digital and it’s watching.

Register. Record. Report. That’s all you need to remember.

Like this project

Posted Jan 3, 2026

Guide to Nigeria's upcoming 2026 tax law changes, impacting freelancers and small businesses.

Likes

1

Views

8