Development and Backtesting of Algorithmic Trading Strategies

Stanislav Kanzafarov

This project focuses on creating a robust infrastructure for designing, optimizing, and backtesting algorithmic trading strategies. By leveraging real historical market data and advanced mathematical models, the system allows traders and researchers to evaluate the performance of strategies before deploying them in live trading. The framework is designed for flexibility, enabling support for multiple trading pairs, custom strategies, and comprehensive performance metrics.

Tech Stack:

Frontend:

Next.js (for interactive UI and dashboard creation)

React (for modular components and user interface development)

TailwindCSS (for responsive design and customization)

Backend:

Node.js (server-side logic and API)

Prisma ORM (database management and queries)

AWS Lambda (for scalable serverless execution of backtests)

PostgreSQL (to store historical data and results)

Data Handling:

AWS SQS (queue management for parallel task execution)

Lightweight-charts (to display trading data visually)

Axios (for API integration and data fetching)

Programming Languages:

TypeScript (frontend and backend logic)

Python (strategy testing and financial data analysis)

Testing and Automation:

Jest (unit and integration tests)

GitHub Actions (CI/CD)

Core Features:

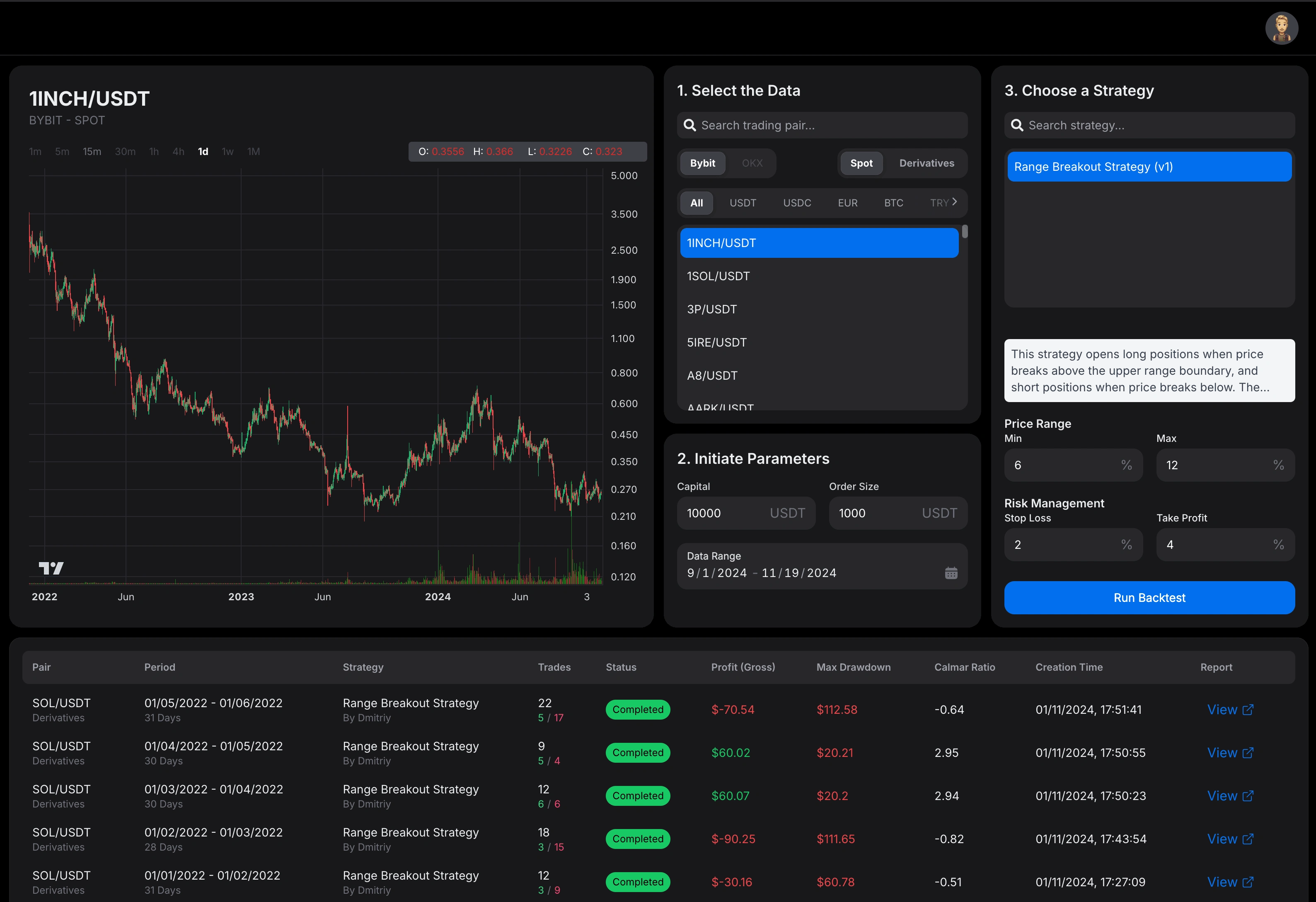

Backtesting Engine:

Analyze historical data across multiple timeframes (1m, 5m, 1h, etc.).

Support for strategies with configurable parameters (e.g., Stop Loss, Take Profit).

Generate detailed performance metrics: Net Profit, Drawdown, Sharpe Ratio, and more.

Trading Pair Management:

Selection and storage of multiple trading pairs into sets.

Reuse sets across different backtests for efficient analysis.

Customizable Strategies:

Users can define unique strategies through a UI or API.

Python-based execution for complex logic (e.g., machine learning models).

Visualization Tools:

Interactive charts for OHLC data, entry/exit points, and performance graphs.

Progress tracking for backtesting jobs.

Scalability:

Serverless architecture with AWS Lambda for parallel processing of 100+ trading pairs.

PostgreSQL for efficient handling of large datasets (70+ GB).

Objective:

The goal of this project is to provide traders, analysts, and developers with a professional-grade backtesting environment to validate trading strategies efficiently, saving time and resources while reducing financial risks.

Challenges Solved:

Built a scalable architecture capable of handling hundreds of simultaneous backtests.

Optimized database queries to ensure fast data retrieval for multi-terabyte datasets.

Integrated an intuitive UI for managing trading pairs, strategy parameters, and results visualization.

Like this project

Posted Nov 19, 2024

Built a scalable backtesting platform for algorithmic trading strategies with advanced data visualization, multi-pair management, and performance metrics. Lever