M.J Borkowiec

Strategic Intelligence Writer — Market Briefings, Executive

Ready for work

M.J is ready for their next project!

Strategic Market Briefings & Intelligence Reports

0

46

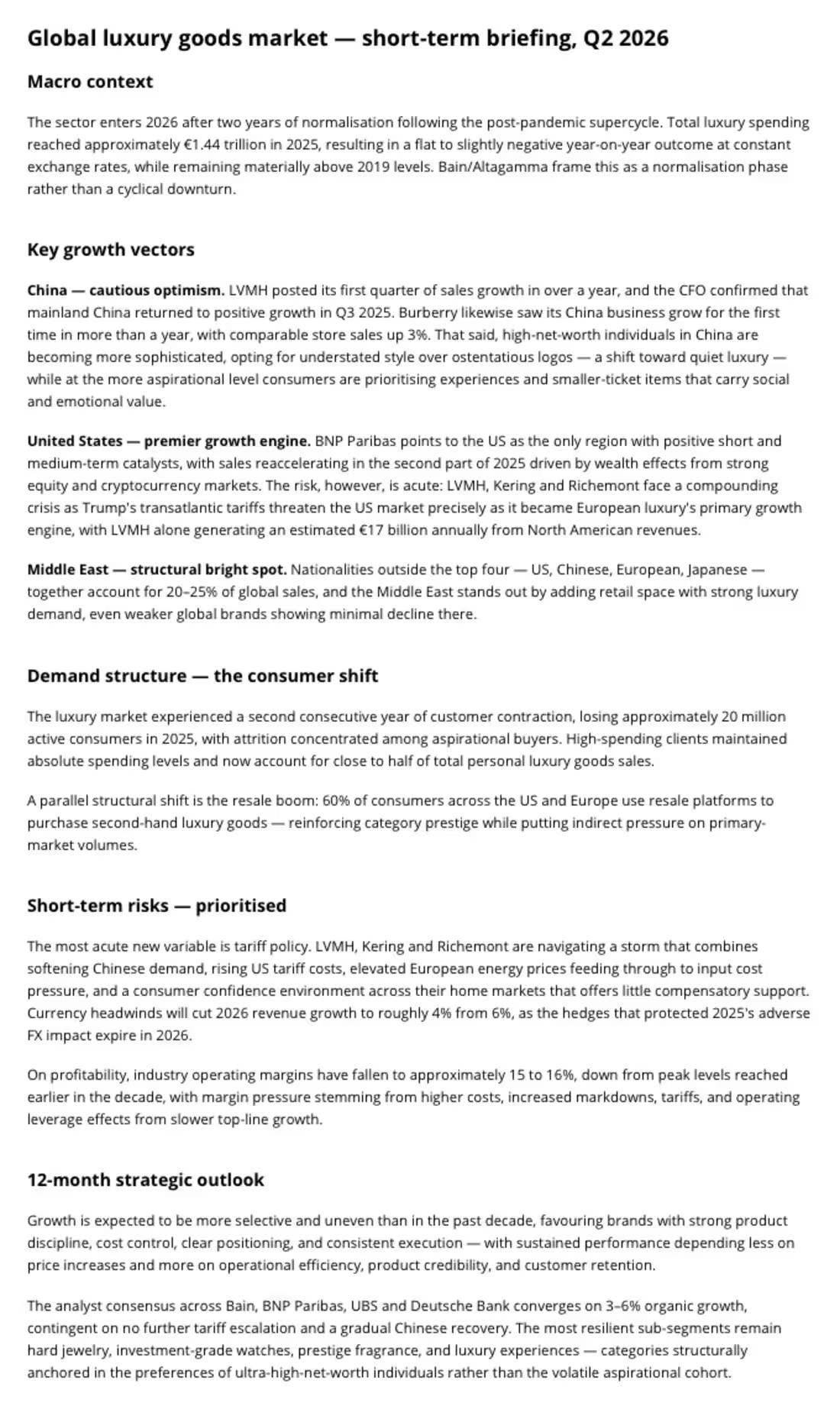

12-month strategic outlook

Growth is expected to be more selective and uneven than in the past decade, favouring brands with strong product discipline, cost control, clear positioning, and consistent execution — with sustained performance depending less on price increases and more on operational efficiency, product credibility, and customer retention.

The analyst consensus across Bain, BNP Paribas, UBS and Deutsche Bank converges on 3–6% organic growth, contingent on no further tariff escalation and a gradual Chinese recovery. The most resilient sub-segments remain hard jewelry, investment-grade watches, prestige fragrance, and luxury experiences — categories structurally anchored in the preferences of ultra-high-net-worth individuals rather than the volatile aspirational cohort.

0

43

Macro context

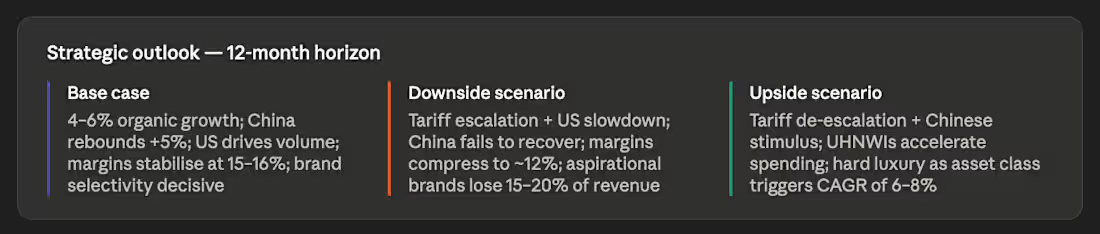

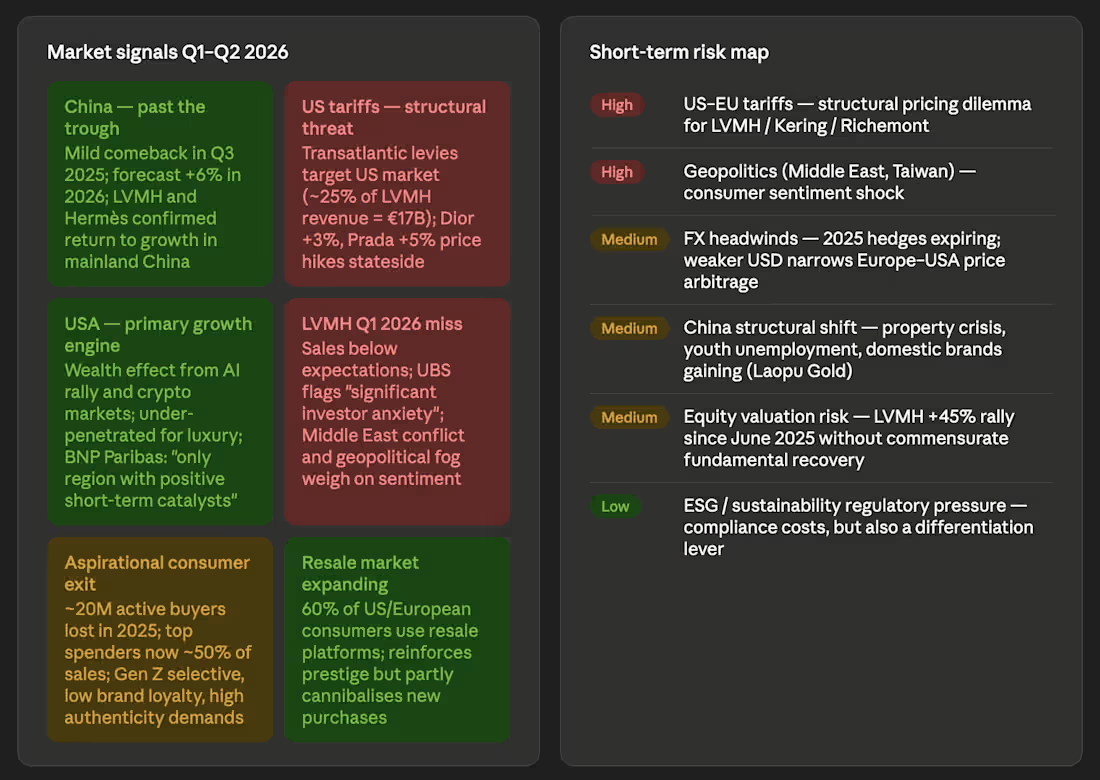

The sector enters 2026 after two years of normalisation following the post-pandemic supercycle. Total luxury spending reached approximately €1.44 trillion in 2025, resulting in a flat to slightly negative year-on-year outcome at constant exchange rates, while remaining materially above 2019 levels. Bain/Altagamma frame this as a normalisation phase rather than a cyclical downturn.

2

100

Global luxury goods market — short-term briefing, Q2 2026

3

3

200