Kyran Maher

Finance & Economics student at UNH

New to Contra

Kyran is building their profile!

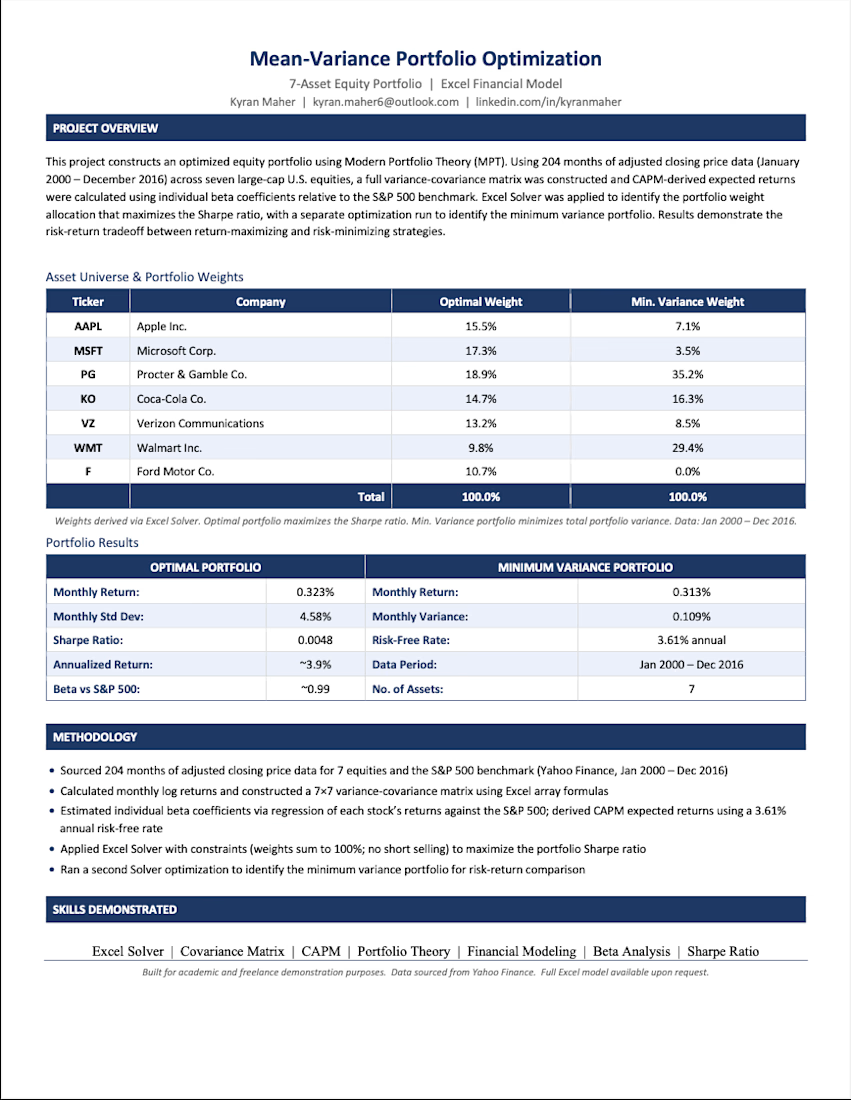

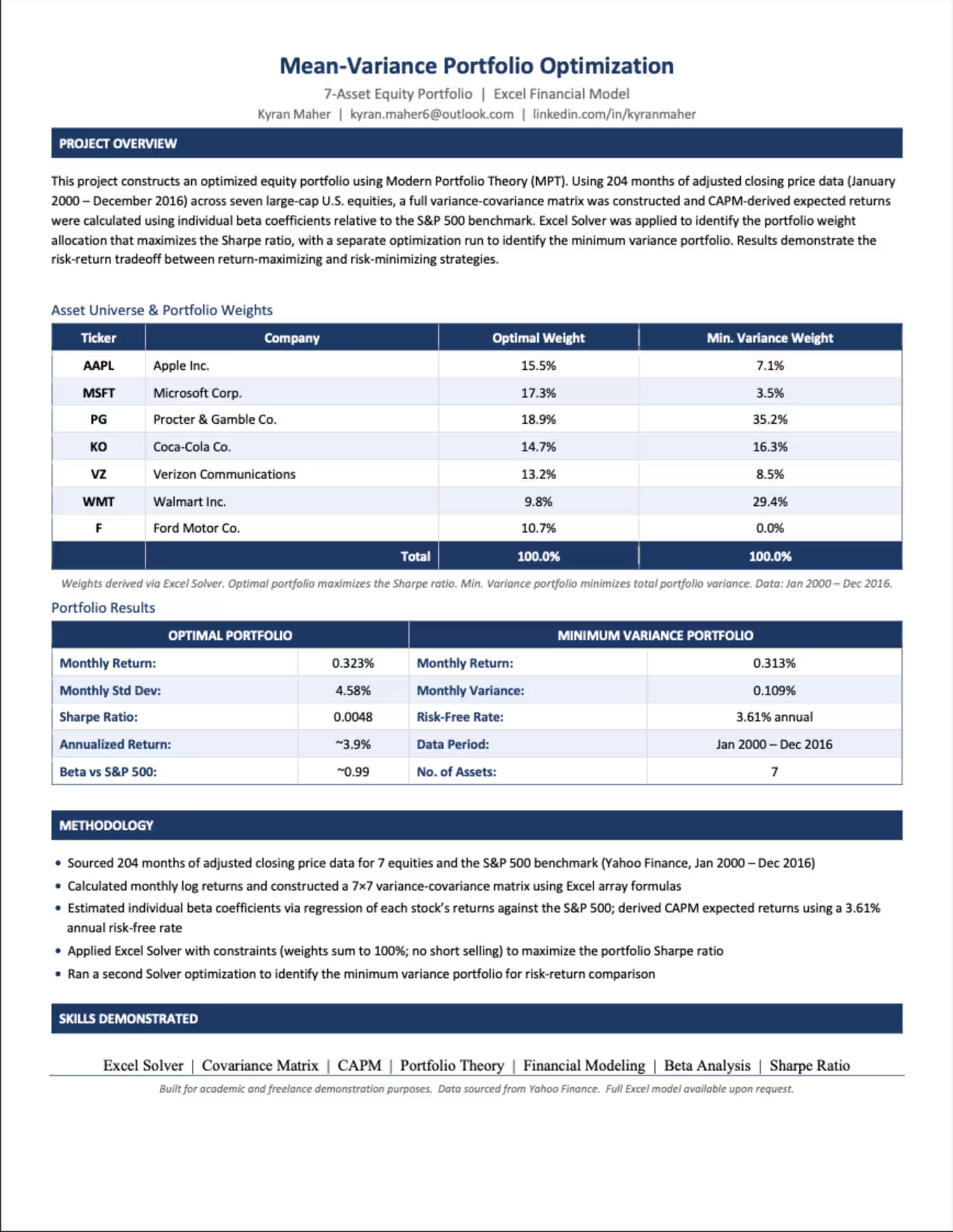

I recently built a mean-variance portfolio optimization model in Excel from scratch — 204 months of return data across 7 large-cap equities including Apple, Microsoft, Procter & Gamble, and Coca-Cola. Using CAPM-derived expected returns, a full 7x7 covariance matrix, and Excel...