The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Back to feedPost

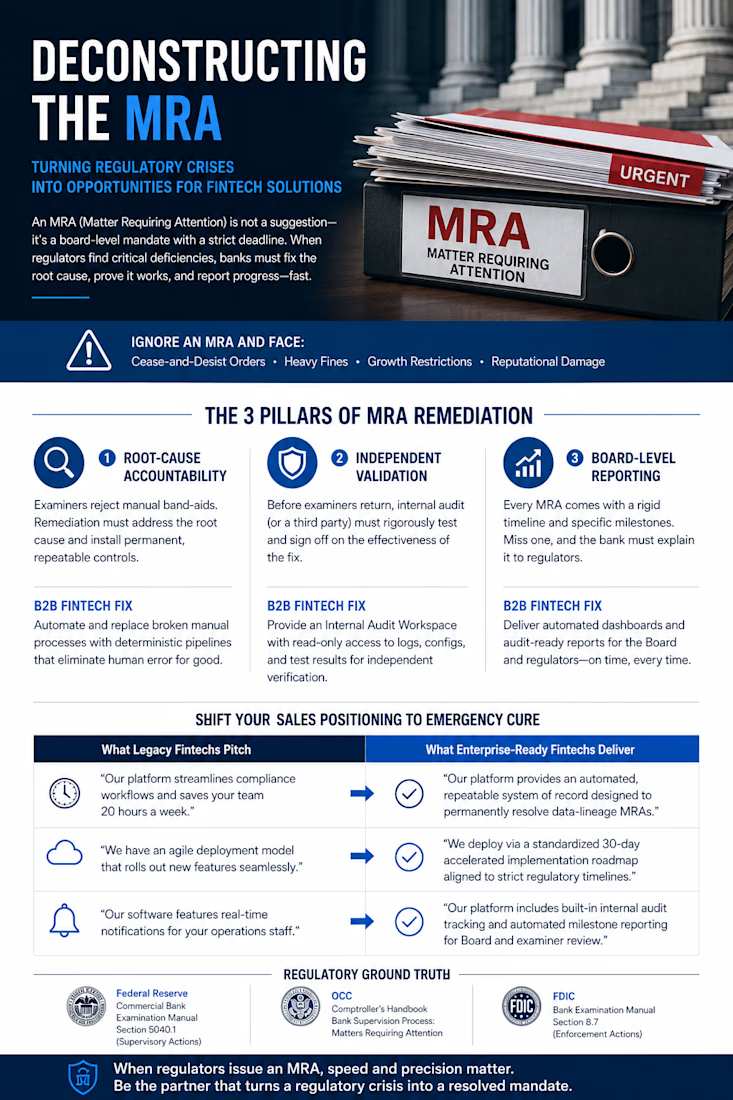

Deconstructing the MRA (Matters Requiring Attention) ### Positioning B2B Software as the High-Stakes Emergency Cure for Failed Bank Exams When a B2B tech vendor sells software to an enterprise bank, they usually frame it as a proactive improvement—something to increase efficiency, lower operating costs, or modernize a workflow over the next fiscal year. But there is a specific trigger event in banking where all budget constraints evaporate, procurement speed cycles jump by 10x, and a bank will buy software immediately based on sheer panic. That trigger is an MRA (Matter Requiring Attention) or an MRBA (Matter Requiring Immediate Attention) issued by bank examiners. When the Federal Reserve, the OCC, or the FDIC conducts their annual supervisory exams, they don't just hand out grades. If they find deficiencies in a bank's risk management, compliance tracing, or data governance, they issue a formal regulatory citation. An MRA is not a friendly suggestion; it is a legally binding, board-level mandate with a strict, non-negotiable ticking clock. If a bank ignores an MRA, it escalates to a formal Cease-and-Desist order, severe civil money penalties, or a complete freeze on the bank’s ability to acquire other companies or launch new products. ### The Anatomy of an MRA Crisis When an executive team receives an MRA, their job is on the line. If your B2B fintech can align its value proposition directly with the specific pain points of an active MRA remediation lifecycle, you stop being a "discretionary software expense" and instantly become an "emergency rescue asset." To build a GTM strategy around this, your software must solve the three fundamental requirements of an MRA remediation plan: #### 1. Root-Cause Accountability (Beyond the Quick Fix) When a bank fails an exam due to a compliance gap (e.g., weak transaction monitoring or broken data lineage in credit decisions), the knee-jerk reaction is to throw manual labor at it. Banks will hire hundreds of expensive contractors to manually audit spreadsheets. * The Regulatory Reality: Examiners explicitly reject manual band-aids for systemic issues. Under the standard Fed and OCC supervisory manuals, a bank’s remediation plan must address the root cause of the deficiency and install permanent, repeatable controls. * The B2B Fintech Fix: Don't pitch your platform as a tool that simply "helps teams work faster." Pitch it as an automated, permanent replacement for their broken manual processes. Provide deterministic software pipelines that programmatically eliminate human error, ensuring the root cause cited by the examiner can never happen again. #### 2. The Independent Validation Hurdle A bank cannot just fix the problem, write a letter to the Fed saying "it's fixed," and close out the MRA. * The Regulatory Reality: Before the regulatory examiners return to review the remediation work, the bank’s internal independent audit function (or an expensive third-party consulting firm) must rigorously test the new fix and formally sign off on its operational effectiveness. * The B2B Fintech Fix: Build an explicit "Internal Audit Workspace" directly into your software. Give the bank's internal auditors independent, read-only access to historic system logs, configuration changes, and testing metrics. This allows them to verify your software’s compliance with the remediation plan without interrupting production operations. #### 3. Board-Level Milestone Reporting Every MRA comes with a rigid timeline—frequently 60, 90, or 180 days—broken down into specific execution milestones. The bank's Board of Directors is personally required to monitor this progress and submit detailed status updates to the regulators. * The Regulatory Reality: If a milestone is missed, the bank must proactively explain the failure to the regulators, severely damaging their supervisory relationship. * The B2B Fintech Fix: Provide automated, executive-ready progress tracking dashboards. If your software is being deployed to fix a data cleanup or compliance tracking problem, it should automatically generate scannable, audit-ready PDF reports that the compliance officer can hand directly to the Board of Directors for their monthly regulatory submission. ### Shifting Your Sales Positioning to Emergency Cure When you find a bank dealing with regulatory pressure, you must completely drop the standard startup marketing language and speak the language of exam defense: | What Legacy Fintechs Pitch | What Enterprise-Ready Fintechs Deliver | |---|---| | "Our platform streamlines compliance workflows and saves your team 20 hours a week." | "Our platform provides an automated, repeatable system of record designed to permanently resolve data-lineage MRAs." | | "We have an agile deployment model that rolls out new features seamlessly." | "We deploy via a standardized 30-day accelerated implementation roadmap aligned to strict regulatory remediation timelines." | | "Our software features real-time notifications for your operations staff." | "Our platform includes built-in internal audit tracking and automated milestone reporting for Board and examiner review." | ### Verified Regulatory Ground Truth via navigation path: * Federal Reserve Source: Federal Reserve Commercial Bank Examination Manual - Section 5040.1 (Supervisory Actions) * OCC Source: OCC Comptroller’s Handbook - Bank Supervision Process: Matters Requiring Attention

The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Related posts

I built Chirp, a temporary shared room for small moments — 10-second sounds, photos, doodles, and stickers that disappear after 24 hours.

Most online spaces today feel public, permanent, and performative. I wanted to make the opposite: a private, playful, low-pressure room where people can leave tiny traces together without creating another profile, feed, or archive.

Anyone can create a room without logging in, share a unique link, and invite others to record short sounds, reply with audio, add photos, place stickers, or doodle on the canvas.

Chirp may look like a playful canvas, but it is not a productivity board or a persistent workspace. The 24-hour expiration is part of the design: because everything fades away, people can post more casually and treat the room like a shared moment, not a social feed.

I built Chirp with Figma Make to explore how Figma can be used to create an interactive, expressive, and temporary web experience.

Note: Chirp is an experimental prototype built for Config Makeathon. Rooms and uploaded content are temporary, so please don’t use it for sensitive information.

Live project:

https://chirp.figma.site/

Amazing!!!

I wanted to build a Sci-fi HUD creation tool with plenty of customization options.

So I built the SINGULARITY HUD CREATION TOOL

Live site: https://singularityhud.figma.site/

GitHub Repository: https://github.com/nytrite/SingularityHudCreationTool

SINGULARITY is a notch web-based studio for making cool animated graphics, technical drawings, and futuristic interfaces.

It works in your browser and uses special technology to make smooth animations.

The studio has a professional look, with a dark theme, orange accents, and a clean, simple design.

This makes it easy for designers to create and animate graphics and export them in a ready-to-use format, such as MP4.

The tool is great for making all sorts of graphics from animated user interfaces to schematics and cinematic sci-fi interfaces.

It uses an animation engine that makes everything look smooth and realistic.

With SINGULARITY, designers can make high-quality motion graphics and HUDs quickly and easily.

My process:

Pen and paper → Figma make → Using Figma make to generate ideas → Prompting it out as perfectly as I can get it to work → Connected to Supabase → Deployed

Thank you!

I built a digital paper fashion atelier. It's called Vogue & Scissors.

It started with a simple wish: I wanted to try on different outfits on myself online. But make it 1960s Vogue, inspired by collages, cutouts, and paper dolls.

Built the entire thing in @Figma Make, first thing I've ever vibecoded with it.

I used Figma Weave to transform the dress images.

Every visitor gets a doll and a wardrobe. You mix, match, and layer vintage-inspired pieces to style your own look on an interactive canvas.

In Vogue & Scissors the wardrobe never runs out, the scissors are optional, and nothing ever tears.

I love how Figma Make is the kind of tool that lets you focus on what something should feel like, not how to ship it. I can’t wait to use it for real projects at Macromo.

Made for the @contra x Figma Makethon #FigmaMakeathon

Try it yourself, link is in the first comment.

Love the visual direction here. The attention to detail really stands out.

Trending

Claude

Claude has entered the design space. How are you using Claude Design?

Contra University

Learn from expert creatives how to earn more using next-gen AI tools.

MagicPath

The canvas is infinite, and exploration is becoming the workflow. How are you using MagicPath?

creativeaiflow

Creative AI workflows are evolving. What tools do you use, and what are their strengths and weaknesses?

freelancerlife

Freelancer life is wins, pivots, and everything in between. What’s yours right now?