The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Back to feedPost

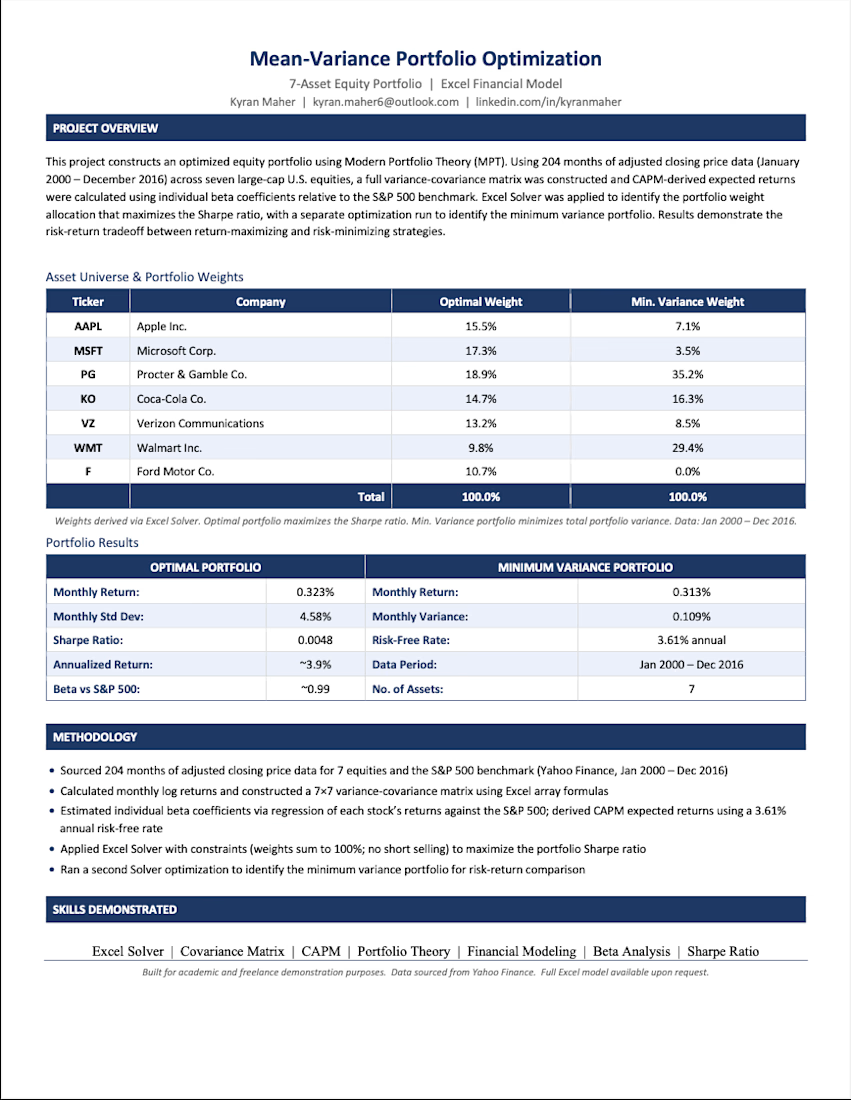

I recently built a mean-variance portfolio optimization model in Excel from scratch — 204 months of return data across 7 large-cap equities including Apple, Microsoft, Procter & Gamble, and Coca-Cola. Using CAPM-derived expected returns, a full 7x7 covariance matrix, and Excel Solver, I identified the optimal portfolio weights to maximize the Sharpe ratio and separately solved for the minimum variance portfolio. The result: a fully documented, professionally formatted financial model with five organized tabs covering price data, monthly returns, statistical analysis, and optimization results. This is the kind of structured, accurate analytical work I bring to every project.

The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Related posts

Built this using Figma Make for the $100K Makeathon.

Instead of creating something visually flashy, I focused on what actually drives results — clarity, hierarchy, and conversion psychology.

This concept is an AI-powered SaaS landing page designed specifically for service businesses that struggle with inconsistent lead flow. Every section is structured to reduce friction and increase demo bookings — from the headline framing to the trust positioning and CTA flow.

The goal wasn’t just to design a page.

It was to design a system that converts.

Open to feedback — and always open to building ambitious things.

figma.com

Figma

Created with Figma

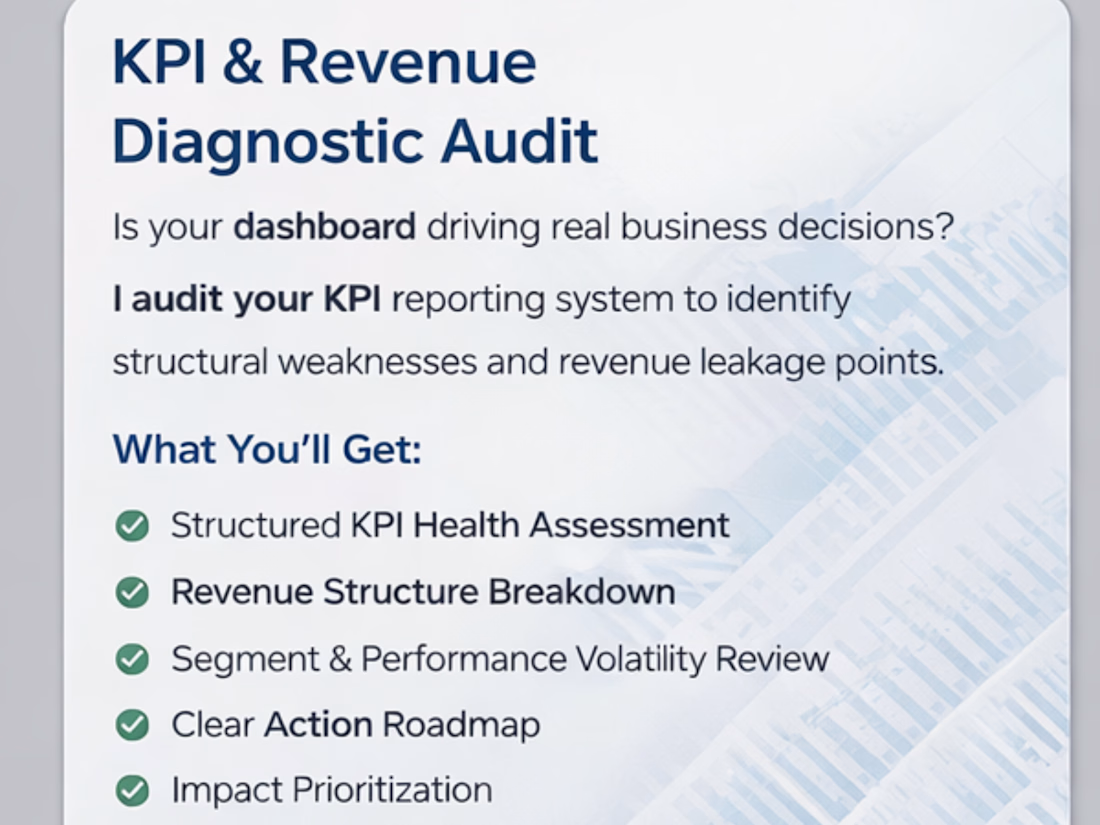

Most dashboards don’t have a visualization problem.

They have a KPI problem.

I’ve reviewed dozens of reporting systems recently and the pattern is consistent:

Metrics are defined differently across sheets

“Revenue” means one thing in finance and another in marketing

KPIs are tracked… but not tied to decisions

Dashboards look clean but don’t answer operational questions

When metric logic isn’t aligned, teams don’t have a data problem.

They have a decision problem.

That’s why I’ve started offering a structured KPI & Revenue Diagnostic Audit — focused on:

• Metric consistency

• Reporting logic

• Revenue driver alignment

• Decision-readiness

If you're building dashboards or scaling reporting systems, this layer matters more than design.

Data VisualizationData AnalysisProduct Data AnalyticsMicrosoft ExcelMicrosoft WordGoogle Sheetsexceldashboardexceldataanalytics

Completely agree. Most dashboards optimize for visuals, not decision velocity. If KPIs aren’t standardized across teams, you’re basically scaling confusion. The real leverage is in metric governance before visualization.

Trending

maxearnings

The next frontier of payments is live on Contra. How are you maximizing revenue?

freelancerlife

Freelancer life is wins, pivots, and everything in between. What’s yours right now?

aidesignflow

AI tools are redefining how designer work. What does your workflow look like?

micrographics

Micrographics started as utility - barcodes, packaging, instruction labels. How would you use them?

aivideo

AI video tools are moving at warp speed. What tools are you using?