Fintech and Regtech

Rupnisha Das

Navigating the 6AMLD: A Comprehensive Guide to Minimizing Impact on the Financial Sector

Introduction

The Financial Sector's Top Priority: Staying Compliant with Evolving Legislation

“Corruption is extremely flexible and easily adaptable to new scenarios…It is generally a major impediment to prosperity and security because it hinders sustainable economic growth…and erodes trust between citizens and governments.” Says Giovanni Tartaglia Polcini, Chair of the G20 Anti-Corruption Working Group.

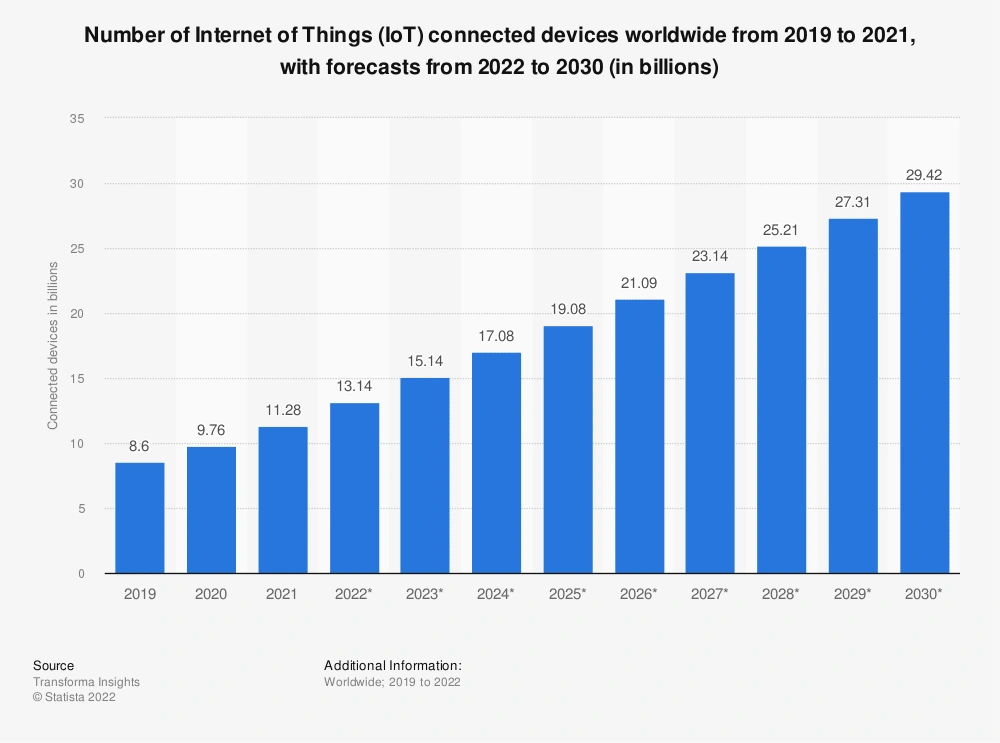

With corruption more rampant than ever, it is getting harder for Financial Institutions to keep up with the new ways in which criminals violate legislation. According to the Federal Trade Commission (FTC), more than 46,000 people have reported losing over $1 billion in crypto to scams since 2021. The rise of digital services is more rapid than ever, especially in the post-pandemic era. Since 2020, almost double the devices have been connected to the Internet of Things (IoT).

The growing use of decentralized payment structures like crypto-currency makes it harder to maintain the integrity of our global financial system. To assist in the fight of tackling Financial Crime, Compliance with evolving legislation is critical for institutions of all sizes.

Financial regulations serve as the bedrock of a stable and transparent financial system, safeguarding against money laundering, terrorist financing, and other illicit activities. Understanding and adhering to these regulations is not just a legal requirement, but also a fundamental duty to protect the integrity of the financial sector.

The financial landscape is in a constant state of flux, with regulatory frameworks continually evolving to address emerging threats and vulnerabilities. One such significant development is the 6AMLD, a game-changing legislation aimed at fortifying the fight against financial crime within the European Union. The 6AMLD is a significant development in the realm of financial regulations, and its implications extend beyond traditional financial institutions to fintech companies operating in the European market.

The amendments include the introduction of a European Union-wide cash payment limit of EUR 10,000. Additionally, the EU Council is advocating for crypto-asset service providers (CASPs) to conduct due diligence on customers for transactions as low as EUR 1,000. Enhanced due diligence measures for cross-border correspondent relationships for CASPs and the extension of the AML regime to cover third-party financing intermediaries and individuals involved in trading precious metals, precious stones, and cultural goods are also proposed.

The European Commission emphasizes that these new rules will enhance consistency in implementing the AML/CFT framework across the EU. They are expected to facilitate the integration of an EU supervisory mechanism and improve the detection of suspicious financial flows and activities.

Considering the EU’s focus on penalties and its overall urgency to tackle Financial Crime in most sectors, Organizations are urged to carefully consider the implications the directive has for them and ensure compliance.

From understanding the directive's relevance to the financial sector to exploring its potential implications and necessary compliance steps, this paper serves as a roadmap for financial institutions navigating the complexities of the 6AMLD. By equipping yourself with the knowledge and practical advice presented, you can ensure compliance, mitigate risks, and maintain a robust anti-money laundering framework amidst evolving regulatory requirements. By the end of this comprehensive paper, you will have the knowledge and tools necessary to minimize the impact of the 6AMLD and embrace emerging financial regulations with confidence.

The Need for Advice on the 6AMLD and Emerging Financial Regulations

As the 6AMLD proposes a more rigorous and comprehensive set of obligations, financial institutions find themselves confronted with new challenges and heightened compliance requirements. Understanding the impact of the 6AMLD on their operations is crucial for fintechs to ensure full compliance with the directive and avoid potential legal and regulatory consequences.

Financial institutions and companies are obligated to comply with the new rules set forth by the 6AMLD and all its ensuing iterations. They must implement robust systems and procedures to prevent and detect money laundering and terrorist financing activities. The directive emphasizes the need for a consistent and coordinated approach to combat financial crime across the EU, promoting collaboration among member states and enhancing information sharing.

Within this dynamic landscape, financial institutions face the task of deciphering and implementing the intricate regulations that govern their operations. Navigating the complexities of the 6AMLD and other emerging financial regulations necessitates expertise, foresight, and a comprehensive understanding of the regulatory landscape. To successfully adapt to these changes, institutions require trusted advice, practical guidance, and reliable solutions that can help them navigate the shifting compliance landscape effectively.

Understanding the 6AMLD: An Overview

The Sixth Anti-Money Laundering Directive (6AMLD) is a pivotal legislative framework introduced by the European Union (EU) to combat money laundering, terrorist financing, and other financial crimes. Building upon previous directives, the 6AMLD aims to strengthen the EU's anti-money laundering (AML) and counter-terrorist financing (CTF) regime.

At its core, the 6AMLD seeks to provide a comprehensive and harmonized approach to AML and CTF across EU member states. It addresses the evolving landscape of financial crimes and introduces enhanced measures to tackle emerging risks. By harmonizing AML rules and procedures, the 6AMLD promotes consistency and cooperation among member states, thereby fortifying the effectiveness of the AML framework.

The significance of the 6AMLD lies in its recognition of the growing sophistication of criminal activities and the role of emerging technologies. By adopting and implementing this directive, the EU takes a crucial step forward in the fight against financial crime, protecting EU citizens from the threats posed by terrorism and organized crime.

The financial sector plays a vital role in the fight against money laundering and terrorist financing. As such, the 6AMLD holds significant relevance for financial institutions operating within the EU. Banks, payment service providers, investment firms, and other entities involved in financial transactions must understand and comply with the requirements outlined in the 6AMLD.

Adhering to the 6AMLD is not only a legal requirement but also a responsibility for financial institutions and companies operating within the EU. Non-compliance with the 6AMLD can have severe implications for financial institutions. Regulatory authorities have heightened their focus on enforcement, imposing substantial penalties and reputational damage on entities that fail to meet the directive's obligations. Furthermore, non-compliance increases the risk of facilitating illicit financial activities, exposing institutions to legal and financial consequences. By actively embracing the provisions of the 6AMLD, organizations contribute to the integrity and stability of the EU's financial system, safeguarding it against illicit activities and ensuring a safer environment for businesses and individuals alike.

To navigate the challenges posed by the 6AMLD, financial institutions must prioritize understanding the directive's provisions and implementing robust AML and CTF measures. By proactively ensuring compliance, institutions can protect themselves from regulatory consequences, contribute to the collective effort against financial crimes, and maintain the integrity of the financial sector.

Features of the 6AMLD

Beneficial Ownership Transparency

One of the significant focuses of the Sixth Anti-Money Laundering Directive (the 6AMLD) is on beneficial ownership transparency. In 2019, a Luxembourg law was enacted to establish a register of beneficial ownership, which requires certain information about the beneficial owners of registered entities to be entered and kept in the register. Some of this information is accessible to the public, including through the Internet. The law also allows beneficial owners to request that access to their information be restricted in certain situations.

The Luxembourg District Court turned to the Court of Justice of the European Union (CJEU) to question if such a move would violate provisions under the Charter of Fundamental Rights of the European Union. In response, the CJEU stated that such registers should not be freely accessible to the public.

Considering this, the the 6AMLD strikes a balance between transparency and protecting personal data privacy. Their position is that access to beneficial ownership registers should be granted to individuals who can demonstrate a 'legitimate interest' in accessing the personal data contained in these registers. This includes journalists and civil society organizations involved in AML.

The directive mandates the creation of centralized registers that contain information on beneficial ownership. These registers aim to enhance transparency and accountability in corporate structures, thereby deterring the misuse of legal entities for money laundering and other illicit activities.

Predicate Offenses

One significant aspect of the 6AMLD is the introduction of predicate offenses. Predicate offenses play a crucial role in the context of money laundering. These offenses serve as the underlying criminal activities that generate illicit proceeds, which are then funneled into the financial system for laundering purposes. Identifying and preventing predicate offenses is essential in disrupting the flow of illegal funds and combating money laundering effectively.

Predicate offenses are crimes that generate funds that criminals seek to launder. The directive identifies 22 predicate offenses, including cybercrime and environmental crime, which were previously not included in some jurisdictions' money laundering laws. The identification of predicate offenses enables financial institutions and authorities to focus their efforts on detecting and preventing money laundering activities associated with these specific criminal acts.

The inclusion of cybercrime and environmental crime as predicate offenses in the Sixth Anti-Money Laundering Directive (the 6AMLD) acknowledges the evolving landscape of criminal activities and the need to address emerging threats. the 6AMLD also harmonizes the definition of existing predicate offenses such as insider trading and market manipulation, tax crimes, human trafficking and smuggling, as well as murder and grievous bodily harm.

Liability for Legal Persons

One significant aspect of the Sixth Anti-Money Laundering Directive (the 6AMLD) is the extension of liability for offenses from 'natural persons' to 'legal persons.' This means that companies and businesses, recognized as legal entities under EU and many national laws, can be held liable and face punishments for breaches of AML regulations. Additionally, individuals and businesses acting on behalf of another company, such as consultants and lawyers, can also be subject to liability.

This extension of corporate liability goes beyond acts of commission, where a business or individuals are directly involved in criminal activities, and includes acts of omission. In other words, individuals who fail to take action to prevent an offense from occurring can also be held liable. This represents a dramatic expansion of corporate liability and emphasizes the importance of proactive measures to prevent and detect money laundering activities.

Stricter Punitive Measures

The 6AMLD introduced stricter punitive measures for individuals and businesses that fail to comply with its requirements. There has been a notable increase in the minimum prison sentence for money laundering offenses, with individuals now facing up to four years in prison. Additionally, significant fines of up to €5 million can be imposed as part of the sentencing. Professional disqualification, and other "proportionate measures" as termed by the directive, are also included.

Corporate offenders, on the other hand, may face even larger fines, closure of business units, asset freezing, confiscation, and, in extreme cases, complete shutdown of the business. The penalties for non-compliance have never been more severe. The aim of these tougher punishments is to promote consistency in the enforcement of money laundering regulations across EU member states.

It is important for individuals and businesses to be mindful of the expanded liability for 'aiding and abetting' offenses. The introduction of tougher punishments reflects the EU's determination to address the serious threat of money laundering and reinforce the integrity of the financial system. It is important for individuals and entities to understand the heightened penalties associated with money laundering under the 6AMLD. By doing so, they can ensure compliance with AML regulations, mitigate the risk of engaging in illicit activities, and contribute to the overall integrity of the financial sector.

Increased Cooperation Requirements

In a June 2021 resolution, the EU emphasized the need “to strengthen cooperation between EU bodies and Member States’ authorities responsible for preventing, deterring and responding to cyber-attacks”.

The 6AMLD highlights the same sentiment by including the need for improved international co-operation among EU Member States investigating and prosecuting cross-border cases. The directive recommends designating one Member State as the main 'hub' for managing legal proceedings related to such cases.

When a money laundering operation spans multiple member states like this, states are required to coordinate their efforts to identify, investigate, and prosecute the criminals involved. This cooperation aims to ensure a unified and consistent approach to tackling money laundering across the European Union.

Additionally, when individuals commit acts within the territory of a Member State where they are a national or habitual resident, that Member State will have jurisdiction. This extends to professionals who divide their time between their home country and another Member State for work purposes. By working together, authorities can share information, evidence, and expertise, thereby increasing the chances of successfully prosecuting and convicting the perpetrators of money laundering crimes.

The 6AMLD provides a list of factors that authorities should consider when determining how and where to conduct their investigations. Such centralization of legal proceedings allows for a streamlined and efficient process while taking into account the interests of all involved member states.

These increased cooperation requirements aim to enhance the effectiveness of AML efforts. This collaborative approach enhances the overall effectiveness of investigations, prosecution, and conviction of money laundering criminals, ultimately contributing to the protection of the financial system and the security of the European Union as a whole.

Potential Impacts of the 6AMLD on Financial Institutions

The implementation of the Sixth Anti-Money Laundering Directive (the 6AMLD) has significant potential impacts on financial institutions:

Enhanced Due Diligence: Financial institutions are required to apply enhanced due diligence measures to identify and verify the identity of beneficial owners. This involves conducting thorough investigations and gathering accurate information about customers and their beneficial ownership structure.

Record-Keeping Requirements: Financial institutions must maintain comprehensive records of their customers, transactions, and beneficial owners. These records should be readily accessible and up-to-date to facilitate effective monitoring, audits, and investigations.

Reporting Obligations: the 6AMLD emphasizes the importance of reporting suspicious transactions promptly. Financial institutions are obligated to establish robust internal systems to detect and report potentially illicit activities, ensuring compliance with reporting requirements.

Key Compliance Steps to Meet the 6AMLD Obligations

To effectively meet the obligations of the 6AMLD, financial institutions should take the following key compliance steps:

Enhanced Due Diligence Procedures: Implement robust and comprehensive due diligence procedures to identify and verify customers and their beneficial owners. This includes conducting risk assessments, verifying identities, and ensuring ongoing monitoring of customer relationships.

Strengthened Record-Keeping Practices: Establish robust record-keeping procedures to maintain accurate and up-to-date records of customers, transactions, and beneficial owners. Ensure that these records are easily accessible for internal and external audits, investigations, and regulatory reviews.

Robust Reporting Systems: Implement systems and processes to detect and report suspicious transactions in compliance with the reporting obligations outlined in the 6AMLD. This includes establishing internal mechanisms for the identification and assessment of potentially illicit activities.

Challenges and Complexities in Implementing the Directive

Implementing the 6AMLD presents several challenges and complexities for financial institutions:

Compliance Costs: Adapting to the requirements of the 6AMLD may involve significant costs, including investments in technology, staff training, and enhanced compliance procedures. Financial institutions must allocate resources to ensure effective implementation.

Cross-Border Operations: Financial institutions with cross-border operations face the challenge of navigating varying AML regulations across different jurisdictions. They must establish comprehensive compliance programs that align with the requirements of each jurisdiction.

Technological Integration: Adopting advanced technology solutions is crucial to effectively implement the 6AMLD. Financial institutions must ensure the integration of appropriate tools for customer due diligence, transaction monitoring, and reporting, while also addressing data privacy and security concerns.

Practical Advice for Financial Institutions for Navigating the Sixth Anti-Money Laundering Directive

To successfully navigate the requirements of the 6AMLD, financial institutions can adopt the following practical advice and strategies:

Adaptation to the 6AMLD

Stay Informed: Stay updated on the latest developments, guidance, and interpretations related to the 6AMLD. Engage with industry associations, regulatory bodies, and compliance networks to access valuable insights and updates.

Review Internal Policies: Conduct a comprehensive review of existing policies, procedures, and controls to ensure alignment with the 6AMLD requirements. Make necessary adjustments and enhancements to address new obligations and guidelines.

Training and Awareness: Provide ongoing training to employees on the 6AMLD requirements, including enhanced due diligence procedures, reporting obligations, and emerging typologies of money laundering and terrorist financing. Foster a culture of compliance and vigilance throughout the institution.

Enhancing Due Diligence and Risk Assessment Processes

Risk-Based Approach: Implement a robust risk-based approach to customer due diligence (CDD) and ongoing monitoring. Tailor the level of due diligence based on the risk profiles of customers, products, services, and geographic locations.

Beneficial Ownership: Strengthen procedures to identify and verify beneficial owners, ensuring transparency and accuracy in the ownership structure of customers.

Enhanced Transaction Monitoring: Implement advanced transaction monitoring systems to detect suspicious patterns, behaviors, or anomalies. Leverage technology-driven solutions for real-time monitoring, alerts, and case management.

Collaboration and Information Sharing: Foster collaboration with other financial institutions, law enforcement agencies, and regulatory bodies to exchange information on emerging risks, typologies, and best practices in AML and CTF.

Leveraging Technology and Automation

RegTech Solutions: Explore regulatory technology (RegTech) solutions that can help streamline compliance efforts. Adopt automated tools for customer onboarding, identity verification, data analysis, and reporting, enhancing efficiency and accuracy.

Data Analytics: Utilize data analytics to identify trends, anomalies, and potential risks more effectively. Implement robust data management systems to ensure data integrity, security, and privacy.

Artificial Intelligence (AI) and Machine Learning (ML): Leverage AI and ML algorithms to enhance transaction monitoring, anomaly detection, and risk assessment. These technologies can help identify complex patterns and flag suspicious activities with greater accuracy.

How Can Companies Prepare?

So now you have an in depth understanding of the directive. But how do you and your company prepare for the changes? The implementation of the Sixth Anti-Money Laundering Directive (6AMLD) brings significant changes and challenges for companies operating within the EU. To ensure compliance and mitigate the risks associated with money laundering and terrorist financing, organizations need to take proactive measures and adapt their processes, systems, and risk management frameworks. This comprehensive guide outlines key steps and considerations to help companies effectively prepare for the requirements of 6AMLD.

Understand the Scope and Impact

Companies should thoroughly assess the scope and impact of 6AMLD on their operations. Gain a clear understanding of the directive's provisions, including the expanded definition of money laundering offenses, stricter penalties, and the extended liability to legal persons. Identify how these changes will impact your organization's risk profile, compliance obligations, and operational processes.

Conduct a Risk Assessment

Perform a comprehensive risk assessment tailored to the specific nature of your business. Identify and evaluate the inherent money laundering and terrorist financing risks associated with your products, services, customers, and geographical locations. This assessment will help you prioritize your resources and design effective controls to mitigate identified risks.

Enhance Customer Due Diligence (CDD) Processes

Review and strengthen your customer due diligence procedures to ensure they align with the enhanced requirements of 6AMLD. Implement robust and risk-based identity verification procedures, including the verification of beneficial ownership information. Consider adopting technology-driven solutions, such as automated identity verification and Know Your Customer (KYC) platforms, to streamline and strengthen your CDD processes.

Improve Transaction Monitoring and Reporting

Enhance your transaction monitoring capabilities to detect and report suspicious activities effectively. Implement advanced analytics tools and technology solutions to identify patterns, anomalies, and red flags associated with money laundering or terrorist financing. Establish a robust internal reporting mechanism that encourages employees to report suspicious transactions promptly and in line with regulatory requirements.

Strengthen Compliance Culture and Training

Foster a culture of compliance within your organization by promoting awareness and understanding of AML regulations and the implications of non-compliance. Provide comprehensive training programs for employees at all levels, ensuring they are familiar with the key provisions of 6AMLD and understand their roles and responsibilities in preventing money laundering. Regularly update training materials to reflect emerging risks and regulatory changes.

Enhance Internal Controls and Governance

Review and strengthen your internal controls and governance framework to align with the requirements of 6AMLD. Implement robust policies, procedures, and controls to mitigate identified risks effectively. Ensure proper segregation of duties, independent testing of AML controls, and ongoing monitoring of compliance activities. Designate a dedicated compliance officer or team responsible for overseeing and managing AML efforts.

Collaborate and Share Information

Establish effective collaboration and information-sharing mechanisms within your organization and with relevant external stakeholders, such as financial intelligence units and law enforcement agencies. Participate in industry forums, sharing best practices, and staying updated on emerging trends and typologies in money laundering and terrorist financing activities. Cooperate with other obliged entities in cross-border cases to facilitate investigations and prosecutions.

Keep Abreast of Regulatory Developments

Stay informed about evolving AML regulations and guidelines at the national, EU, and international levels. Monitor regulatory updates and ensure timely implementation of any changes that impact your organization. Engage with industry associations and professional networks to stay informed about best practices and industry standards in AML compliance.

Conclusion

Navigating the requirements of the Sixth Anti-Money Laundering Directive (the 6AMLD) and other emerging legislation is crucial for financial institutions. Compliance with these regulations is not only a legal obligation but also essential for safeguarding the integrity of the financial sector.

Throughout this comprehensive guide, we have explored the key aspects of the 6AMLD, including its relevance to the financial sector, potential impacts on financial institutions, and necessary compliance steps. We have provided practical advice on adapting to the 6AMLD, enhancing due diligence and risk assessment processes, and leveraging technology to streamline compliance efforts.

It is imperative for financial institutions to proactively navigate the 6AMLD and stay ahead of emerging legislation. By doing so, institutions can effectively mitigate the risks of money laundering, terrorist financing, and other illicit activities while protecting their reputation and ensuring regulatory compliance.

This is where KYC Hub emerges as a beacon of support and expertise. As a leading provider of financial compliance services, we understand the importance of keeping pace with evolving regulations. We specialize in providing comprehensive advice and strategic solutions tailored to the unique needs of financial institutions. Our team of compliance experts possesses an in-depth understanding of the 6AMLD and other emerging financial regulations, ensuring that our clients remain well-equipped to meet their compliance obligations.

At KYC Hub, we are committed to supporting financial institutions in their compliance journey. Our expertise, comprehensive services, and up-to-date knowledge of regulatory changes make us your trusted partner. We encourage you to reach out to KYC Hub for expert advice, tailored solutions, and reliable support in navigating the intricacies of the 6AMLD and other regulatory challenges.

Together, we can forge a path to regulatory excellence, mitigate risks, and uphold the highest standards of compliance in the financial sector. Contact KYC Hub today to embark on a proactive and compliant future.

Like this project

Posted Sep 12, 2023

Industry insight on updated EU law on financial regulation

Likes

0

Views

41

![[Personal Travel Account] Shanghai](https://media.contra.com/image/upload/c_fill,w_700/laoaug4nwo5p2pynbpyj.avif)