Reflections on 2022 Fintech

Jessica Le

I was very bullish on Real time payments. I still am, especially with FedNow on the horizon for 2023.

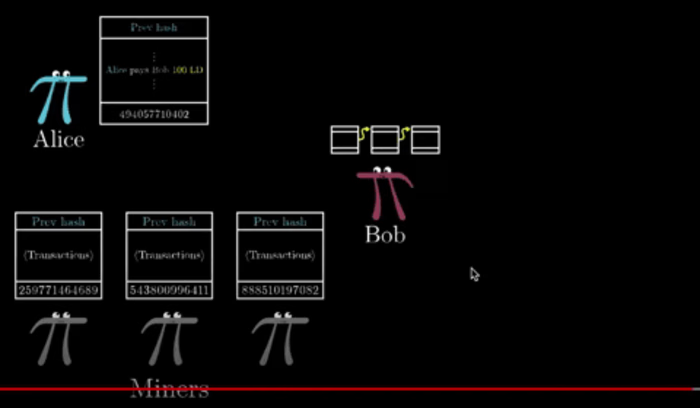

We are already seeing real time rails like RTP, FedNow and Interac and Pix. Startups like Orum are also working to re-route payments to speed them up. Perhaps the answer is also stablecoins but I am less well versed in that arena and believe mass adoption of that for banks and large financial institutions would come later.

Early October it was the 50 year anniversary of ACH. A bit mindblowing to think about - it’s been around half a century and nothing that drastic has improved since then.

The payments sector is saturated full of players owning a piece of the stack, orchestrating the stack, or building software on top. Of course owning more of the stack is valuable, but also providing several payment methods beyond ACH, push payments, cards, etc. is critical. Businesses want faster payments at the very least as an option. And they want it to work, not be patchwork. RTP by TCH (launched in 2017, consortium of 25 largest banks/tech companies, with most smaller FI’s not participating), Zelle (P2P debit payments, NOT settled in real time), Same day ACH, fintech bandaids from large companies like Apple or Google have already been around but what companies are really waiting for I’ve found, is FedNow.

As a quick primer, FedNow will be the first new payment rail since ACH. It’ll actually be instant, all hours of the day, all days of the year. Payments will be received and settled instantly. Funds have to be available instantly. And given certain compliance and fraud measures, funds should be able to be recovered. Similar to RTP in that it’s 24/7 and instant. However it’ll include clearing functionality aka recover funds from failed payments, as well as offer accessibility into 10,000+ financial institutions. It’ll be the first new payment rail since ACH!

Pertinent given how cash focused companies now are, faster payments will be a growing theme, and likely a new embedded feature instead of full-fledged new product.

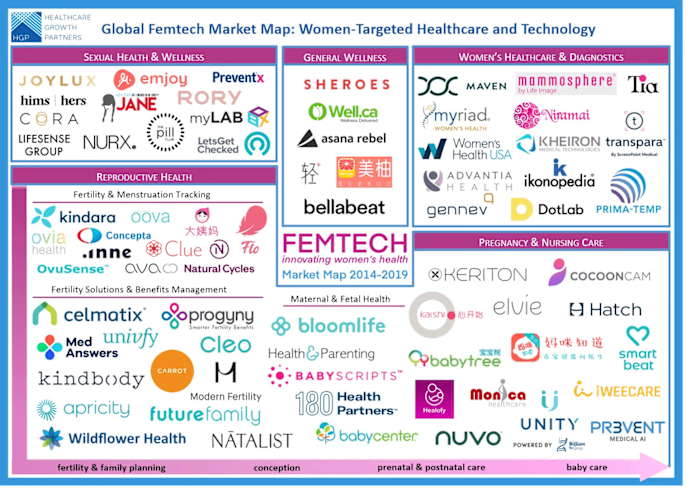

Vertical Payments has and will continue to be an important theme of mine. I’m seeing the beginning of the J curve of more vertical fintech softwares broadly now.

Of course we have big players like Lightspeed POS or Toast or Kindbody that have really succeeded in the vertical payments spaces. However I’m seeing more in verticals like healthcare or specific geographies like MENA now which is very exciting, given how old the infrastructure there is and how difficult it is to penetrate doctors, insurance companies, hospital systems, care providers, etc. There are many moving parts and building a successful network will be a great moat.

Some I have in mind are Nitra and Mercantile. Those two have emerged in the past quarter in the healthcare payments/expense management space (Q3-Q4 2022) and I expect to see a lot more me-too players. I’ve also seen Pluto, the MENA version or Mendel in Latam. I think what will really differentiate will be the same logic as what made Ramp stand out from Brex, Airbase, etc. Better product, better value proposition for customers, monetizing on multiple fronts (although I will say the business models of existing large expense management companies has yet to move towards profitability, but I’d like to think that they know what they’re doing and are going to explode out of nowhere with a crazy product suite like Figma did).

I thought a lot of M&A was going to happen. I change that thought to M&A AND partnerships/collaboration.

I thought big companies were going to swallow the smaller companies that had great technology but were at risk of being swept away with the market downturn, running out of runway, and decline in VC funding, especially as fintech has been experiencing a lot of unbundling and so many “me-too” companies popped up.

As companies work together more closely, it becomes harder to differentiate who actually owns the tech and if it is the network that holds the value or what the company has built itself. As industries become saturated with more me-too companies and we see increasing commoditization, being able to differentiate that will become key.

While I still believe in that and it has already happened, I’ve come to realize that it’s not just about 1 company versus another, but rather about one company’s products and features versus another. Perhaps sometimes it is strategic to acquire a whole startup. But more often than not, as fintech is unbundled and the space becomes more saturated, the smartest fintechs will learn to collaborate and partner with others on some products/features and then compete on others where they believe they have an edge. Especially when it comes to particular customer segments, or incumbents who cannot move as quickly as smaller companies but have the market share. This is already an active theme in crypto given the decentralized nature of the industry, but we have yet to see the communal nature proliferate intro centralized industries.

Of course though, M&A still will continue to persist. However, what I am keen on seeing is if major players will acquire companies more for their tech or book of business. It seems like many are interested more in the former, to cross sell existing customers, especially as many startups in the past couple of years have really just built features, and overall industry saturation has led to commoditization.

Either way, the power law holds true and a handful of companies will hold the vast majority of the pie eventually.

Crypto is suffering right now in the wake of FTX and general market downturn. Thus, regulators are cracking down on the space. 2023 will be a year to see who can hold out the longest and navigate this changing regulatory landscape with the greatest finesse.

Within the broader tech markets, many companies will die as funding becomes more scarce and entrepreneurs don’t manage their cash properly. This holds even more true within crypto, as it was one of the most volatile and noisiest (if not holding #1 place) of 2020-2022. With what happened with FTX, many crypto companies will become easy collateral.

I’m interested to see which infrastructure players will suffer and which ones won’t - as regulators crack down even more aggressively, I’m sure many providers will start turning away crypto customers or stop onboarding until this wave “passes”. This will create a domino effect throughout the industry as most topple (probably within defi and applications) and few survive (probably within more core functions). The ones that survive I’m sure will survive many crypto cycles to come.

Either way, I am fully confident the industry isn’t going anywhere in the long run, but that it will suffer some pretty casualties in 2023.

The market did indeed take a big downturn, forcing companies to focus on profitability and extending runway. The world is so noisy for founders right now. What is the right answer? Growth or profitability? I seriously do not know.

Some of my friends are starting companies. Actually, more and more - I haven’t really seen desire to be a founder drop even though the market took a downturn amongst my demographic at least. But on one hand, you’re hearing from venture capitalists that you should optimize for profitability and reduce burn as much as possible. Advice, I believe worthy or a founder already in the growth stage with moderate amount of funding. But then you hear how Figma got acquired by Adobe and became one of the biggest SaaS acquisitions to date. And they didn’t even start making money until 5 years post launch. The past doesn’t predict the future, but what does hold true is that if you sell a half baked product too early, before finding product-market fit and before truly understanding the problem you’re solving, it’s very hard to turn around after you’ve started selling. I feel for founders right now who are faced with tons of conflicting opinions and noise.

So growth or profitability? Ultimately a question for smart and lucky founders who raised early and have the runway to even contemplate this question. If most companies that become big don’t really get there for at least 5 years, I do believe the market will make a correction before the half decade is up (sorry being hypocritical that past market behavior does predict future behavior here…). So really, optimizing for the long term seems like the best play, again, if you are in the position to do so. Being too short sighted can be your downfall.

Like this project

Posted Oct 17, 2024

These are some personal reflections for my personal blog on the biggest fintech trends of 2022.

Likes

0

Views

9