FIS Advisory Trust-Building Website Content

Sumit Joshi

FIS Advisory — Making "Save 75% on Your Mortgage" Sound True Instead of Suspicious

*The number is real. The job was making it not sound fake*

If a stranger told you they could cut your mortgage interest by up to 75% without refinancing, without switching banks, and without renegotiating anything — you'd assume it's a scam. That's not a hypothetical objection for FIS Advisory. It's the first reaction almost every visitor has, and it happens before they've read a single word of explanation.

The claim is true. Ten years, 900 advisors, and over 10,000 completed cases back it up. But truth and belief are different problems, and the website's entire job was closing that gap.

The Challenge

Financial claims that sound too good to be true carry a specific kind of resistance — the bigger and more attractive the number, the more skeptical people get, not less. A "save up to 75%" headline should be the strongest hook on the page. Instead, on its own, it's the single biggest reason someone would bounce, because it pattern-matches to every predatory loan scheme and financial scam ad they've ever learned to ignore.

Compounding it: the actual mechanism is unusual enough that it doesn't map to anything a typical homeowner already understands. FIS doesn't refinance, doesn't negotiate with the bank, and doesn't change anyone's loan agreement — clients simply follow a restructured repayment schedule FIS calculates from the terms already signed. That's a genuinely different model from anything in the mortgage-advice category, which means the usual trust shortcuts ("like refinancing, but better") don't apply.

Why the Obvious Fixes Don't Work

The instinct with a skeptical audience is to pile on more reassurance — more testimonials, more badges, more exclamation points about how real the savings are. In practice, that backfires. Over-reassurance reads exactly like the marketing language used by the schemes people are already primed to distrust. The more a page insists "this isn't a scam," the more it can look like one.

The other trap is over-explaining the mechanism in technical detail, hoping thoroughness equals trust. But a visitor who doesn't understand amortization schedules and base lending rates won't be reassured by a page full of them — they'll just leave confused instead of leaving skeptical, which isn't actually progress.

The Approach

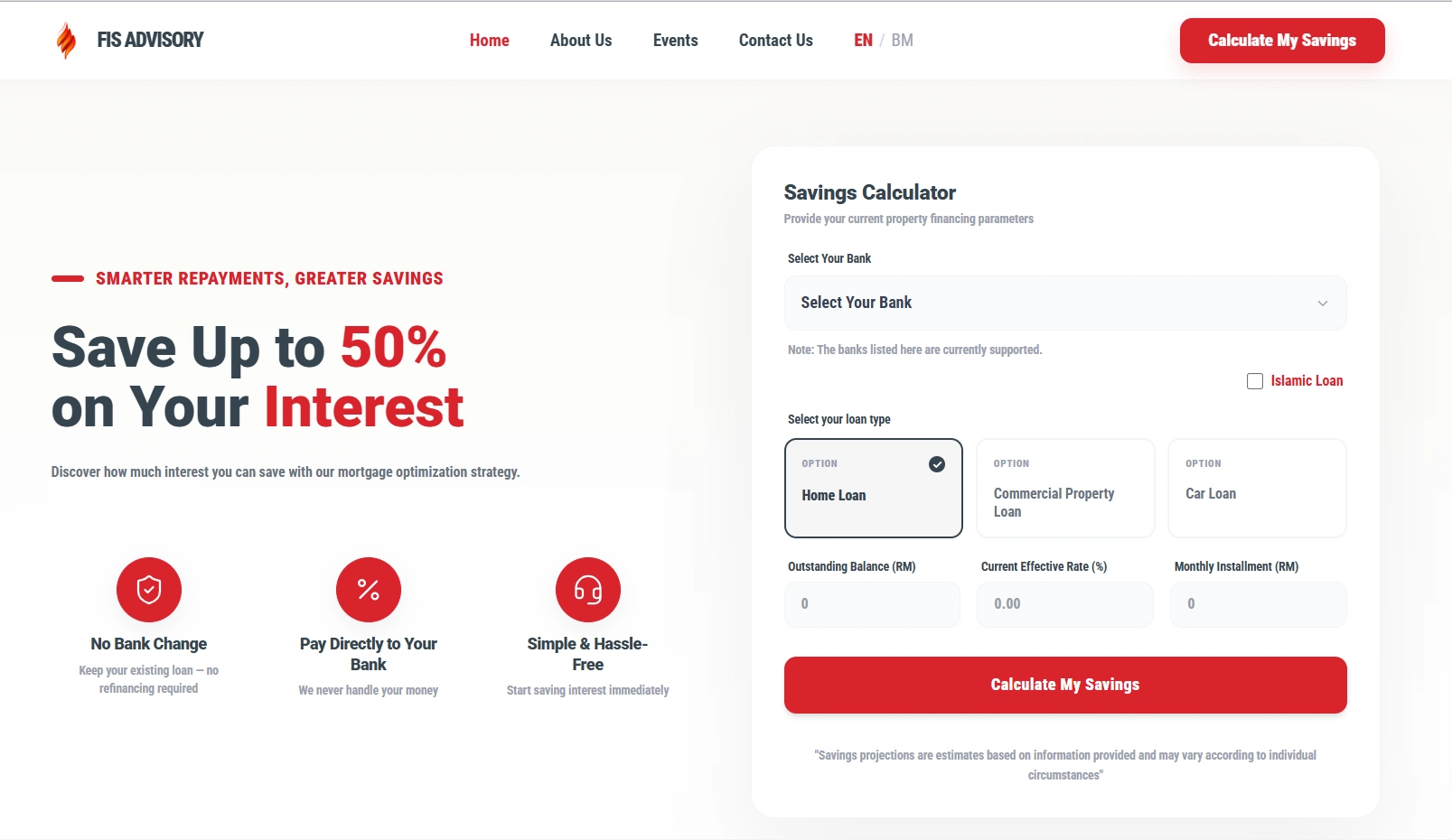

Specificity over superlatives. Instead of leaning on the headline percentage alone, the site had to ground the claim in concrete, case-based detail — real loan amounts, real timeframes, real before-and-after numbers — because specific facts read as evidence, while big round percentages read as marketing.

Explain the model by what it isn't, first. Because "no refinancing, no bank changes, no renegotiation" is unusual, stating clearly what FIS doesn't do turned out to be more reassuring than explaining what it does — it immediately rules out the objections a skeptical visitor already has queued up (Are they going behind my back with my bank? Am I signing something risky?) before diving into the mechanism itself.

Scale as quiet proof, not a banner. Ten years in business and 10,000+ completed cases are strong credibility signals, but presented as loud badges they read as vanity metrics. Placed as supporting context near the claim itself, they do the quieter, more effective job of making the number feel earned rather than promised.

A low-commitment first step. Since the biggest barrier is trust, not interest, the site's real conversion goal wasn't "sign up" — it was "let us show you your own numbers first." A free loan review lets a skeptical visitor test the claim against their own situation before committing to anything, which does more to build belief than any amount of copy could.

The Result

FIS Advisory's site now carries a claim that would sound unbelievable from almost any other source, and gives visitors enough concrete, specific reasoning to actually believe it — without over-explaining the finance behind it, and without over-selling the number itself. The credibility comes from restraint: showing the math, not shouting the headline.

The strongest number on the page was also the biggest liability. The whole job was earning the right to say it plainly.

Like this project

Posted Jul 11, 2026

A too-good-to-be-true mortgage claim, made credible — specific numbers over hype, for a skeptical Malaysian homeowner audience.