The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Back to feedPost

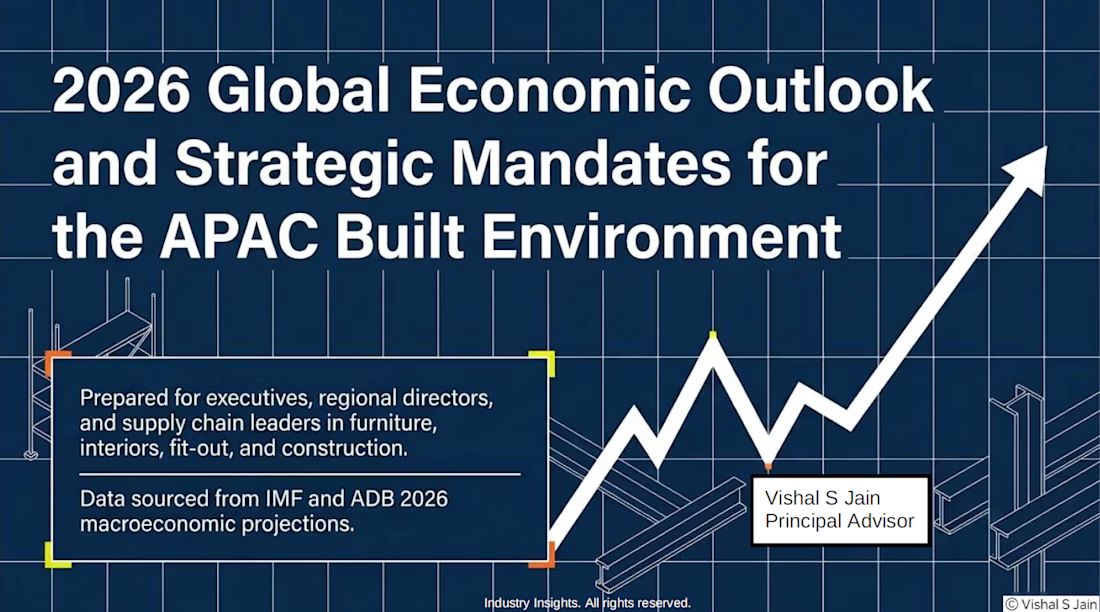

The global economy is entering a higher-risk, higher-cost, and more selective growth phase.

With slower global growth, energy volatility, geopolitical tensions, and tighter financial conditions, businesses across the built-environment sector are beginning to feel direct pressure.

For India & Asia:

-Inflation, energy costs, and currency pressure remain key risks.

For UAE & GCC:

-Growth opportunities continue, supported by infrastructure, real estate, and non-oil expansion — but with rising governance and execution expectations.

For Furniture, Interiors, Fit-Out, EPC & Construction businesses, the impact is clear:

-Raw material volatility

-Freight escalation

-Working capital stress

-Fixed-price contract risk

-Margin pressure

-Slower decision cycles

In this cycle, growth without governance becomes financially dangerous.

The future winners in the built environment may not necessarily be the fastest-growing companies — but the most commercially disciplined ones.

Check Strategic Advisory Report:

“2026 Global Economic Outlook and Strategic Mandates for the APAC Built Environment” Link: https://drive.google.com/file/d/1npSum7jhf9QXVnN0DT1DbIcydryQgReg/view

The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Related posts

Title:

📊 AI-Powered Customer Behavior Analysis Dashboard

Description:

Built an interactive Business Intelligence dashboard to analyze customer behavior, sales performance, customer segmentation, revenue trends, KPIs, and AI-driven business insights using Excel, SQL, Power BI, and Tableau.

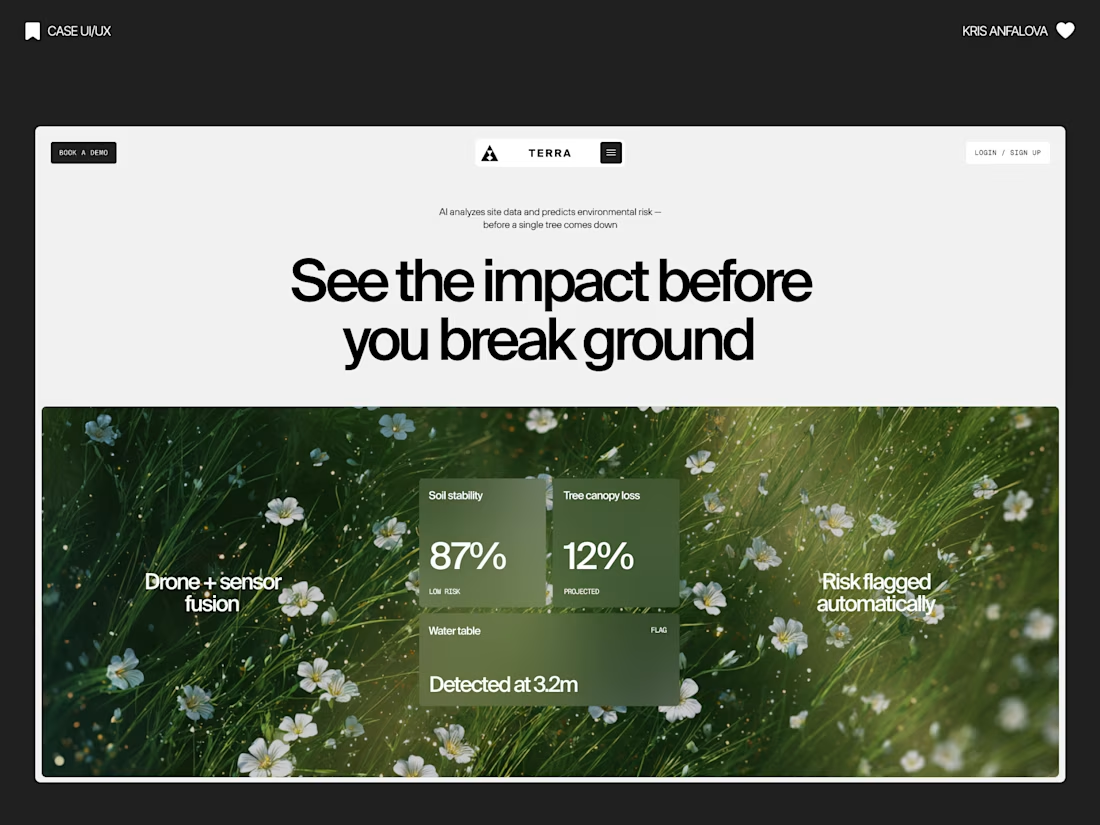

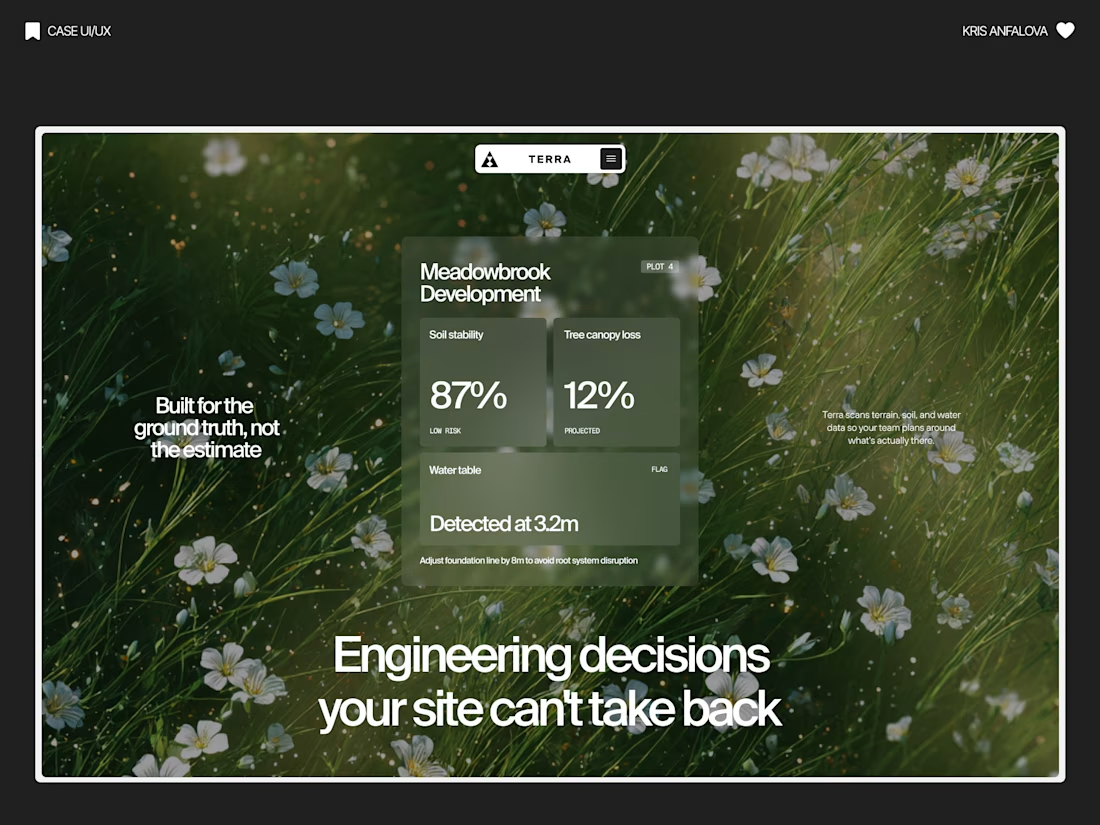

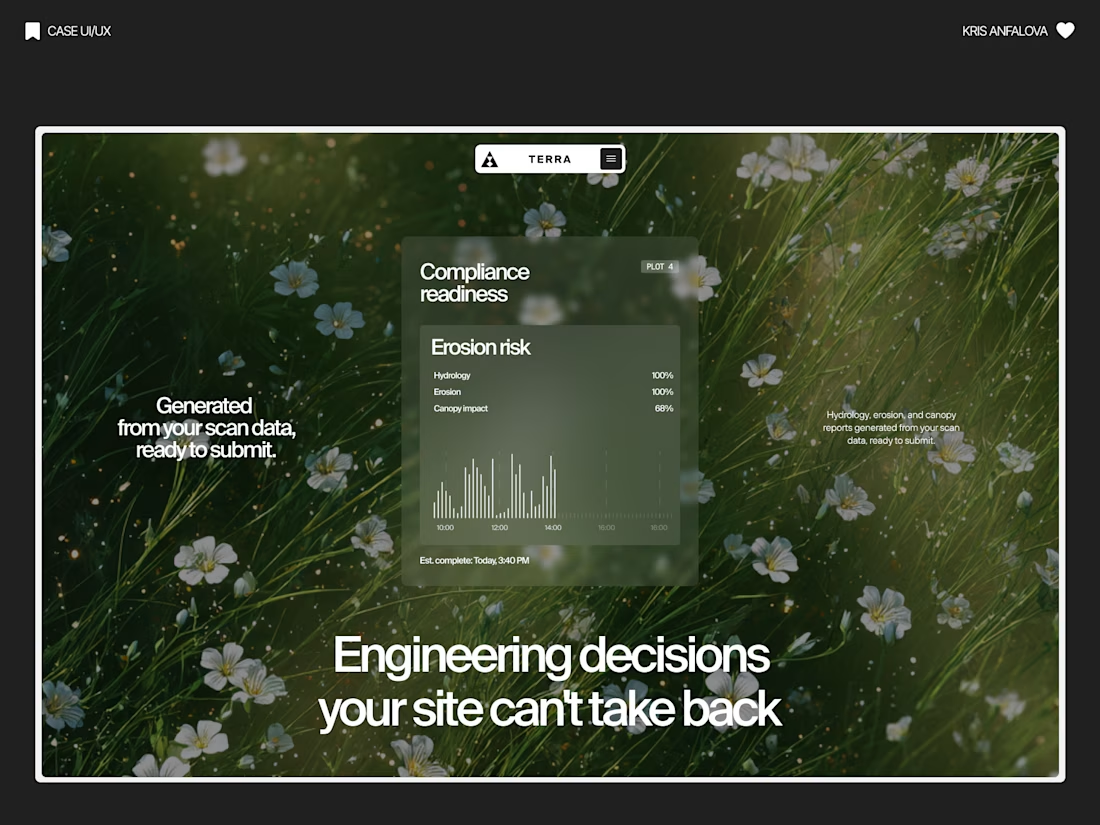

Terra — AI Environmental Risk Platform

Designed the landing page and product UI for Terra — a platform that helps land developers and engineering teams see environmental risk (soil stability, tree canopy loss, water table depth) before breaking ground.

The challenge:

Development decisions are usually based on estimates, not real ground data — and by the time issues show up, it’s often too late to reverse them. The interface needed to make complex sensor/AI data feel immediate and trustworthy, without losing emotional weight.

The solution:

Raw, organic photography (wildflowers, grass, natural terrain) paired with clean glass-panel data cards — creating a visual tension between “nature” and “precision engineering.” Bold editorial typography carries the emotional message, while translucent metric cards surface real numbers: soil stability, canopy loss %, water table depth.

A strong example of turning dense environmental data into something a non-technical stakeholder can understand in seconds.

Nice one

This isn't just a desk with a view.

It's a reminder.

Dreams don't need a fancy office.

They need consistency.

Every late night.

Every failed prototype.

Every redesign.

One day, they become a product people love.

Building Inspo AI has taught me that the best view comes after the hardest climb. 🏔️

Love the perspective. The products that endure usually aren't built in a single breakthrough, they're shaped through consistent iteration and learning over time.

Trending

Claude

Claude has entered the design space. How are you using Claude Design?

Contra University

Learn from expert creatives how to earn more using next-gen AI tools.

creativeaiflow

Creative AI workflows are evolving. What tools do you use, and what are their strengths and weaknesses?

freelancerlife

Freelancer life is wins, pivots, and everything in between. What’s yours right now?