The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Back to feedPost

Beyond the Credit Card: Enterprise Retailers Slash Payment Costs with Direct A2A Settlement

The transition to an A2A (account-to-account) payment method is a strategic decision; it directly affects a company’s bottom line, liquidity, and operations. Changing a company’s financial infrastructure can disrupt day-to-day operations. A payment is done through a sequence of authorisation, clearing, and settlement, digitally, with a fee that could be different from method to method.

Comparing business payment methods

A company’s financial officers deal with every critical step of payments and always aim to get low-cost transactions and focus on ROI payments, which means they use a strategic approach in which a payment is not treated as an administrative expense but as a revenue driver or cost optimiser. This method optimises payment performance by maximising transaction approval rates, reducing processing and interchange fees, minimising cross-border costs, and automating fraud and dispute management to decrease manual labour.

Optimising DSO (days sales outstanding) and capital efficiency are the main factors to consider when choosing a payment method for clients and other businesses.

How credit cards work in business

In earlier days, credit cards were used as high-velocity capital tools and had diverse structural steps, fees, and timelines for completing business transactions.

A payment within the country

A system with the identical currency is easy to deal with, as buyers, sellers, and banks operate quickly through a single financial system.

The cash flow commenced by entering the card details with the supplier's checkout system, which can be a VISA business card or Mastercard Corporate.

After this, the digital process started. The bank sends a request to transfer the money through the issuing bank.

After checking the limits and card amounts, they approve it and fund the supplier.

This process takes 1 to 2 business days, and no fee is charged for the transaction. But getting a business card incurs 1% to 3% additional charges. (Seaman, 2024) Credit card holders also have to maintain the minimum amount, the disruption of which leads to additional payments in the form of interest. (Credit Card Interest Rates and Minimum Payments, 2023)

Overseas Card Payments (cross-border payments)

Overseas businesses deal with different currencies with fluctuating exchange rates. There are some issues noted as currency volatility, import-export charges and many more things.

It takes 3 to 5 business days to complete an overseas payment, a long time due to the time zone differences and banks' security checks.

The International card is already a premium-fee-charged card issued by a bank. There are two types of fees charged on an international transaction: one is a cross-border fee, which is 1% to 1.5% charged by the card network, and the second one is a foreign transaction fee, which is 1% to 3% charged by the issuing bank. The total fee can range from 4% to 6%. The global transaction method is commonly known as SWIFT.

How A2A payments slash payment costs

This is made possible by open banking technology. Setting up an A2A payment method typically starts with the user signing up on a fintech app with basic details like name and date of birth, then linking their bank account by entering information such as the account number and bank branch code. A one-time password (OTP) is sent to the user's registered number to confirm the connection, after which the user sets up a payment PIN to authorise future transactions. In India's UPI system, for example, this PIN is known as a UPI PIN, but the same basic pattern (bank linking, OTP verification, PIN authorisation) applies across most A2A systems globally.

A2A payments within the country

B2B payment portals and banking API is used to send and receive funds directly, and it only takes a minute to remit funds.

Digital apps that provide the facility of transferring funds in the meantime charge no fee on any transaction.

Example: UPI in India, ACH in the US and SEPA in Europe.

Overseas A2A payments

Modern fintech local-routing rails take minutes and hours to complete the international transaction, which is way cheaper, as often under 0.5% to 1%, which is only the foreign exchange markup.

Example: Airwallex, Tipalti, Nium and XFlow

A2A payment method is safer as it doesn’t provide the 16-digit number, CVV, and expiry date to include in any payments; it simply uses the user’s biometric and the data is protected.

Warning: Still, a safer place also has a loophole, as in this method, payment is strictly done in minutes, which is a drawback because if a payment is made, you can’t reverse it. In any business, finance is a very critical department; a minor mistake leads to millions in losses.

Conclusion: A2A payments are permanently disrupting credit card domination and building a real-time ecosystem by eliminating card fees, instant fund transfer, radical fraud reduction and open banking maturity. There are many upcoming strategic steps like integrating real-time APIs, incentivising checkout behaviour and bridging the rewards gap.

The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Related posts

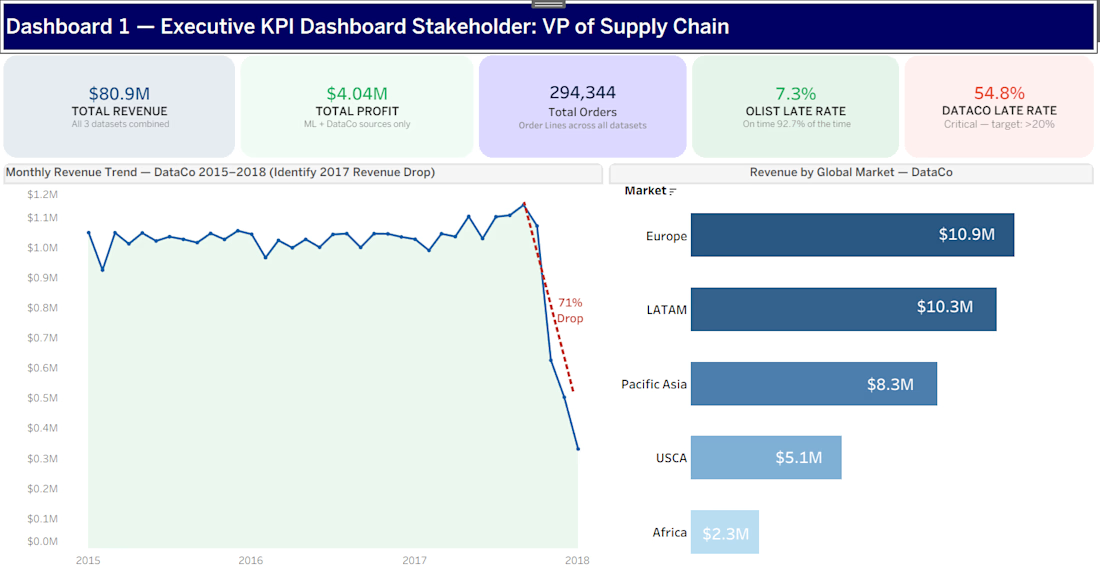

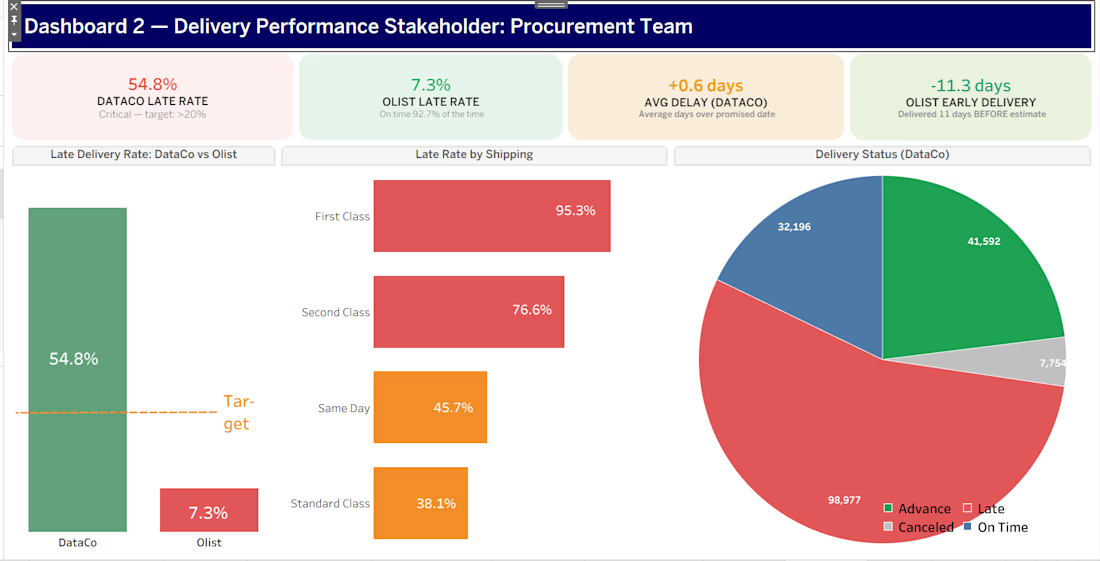

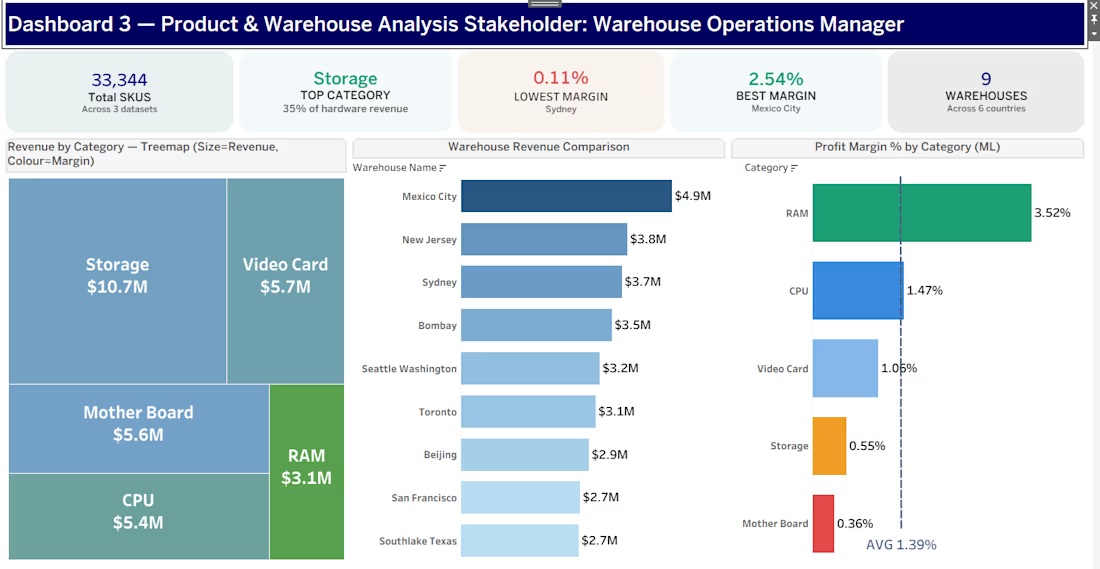

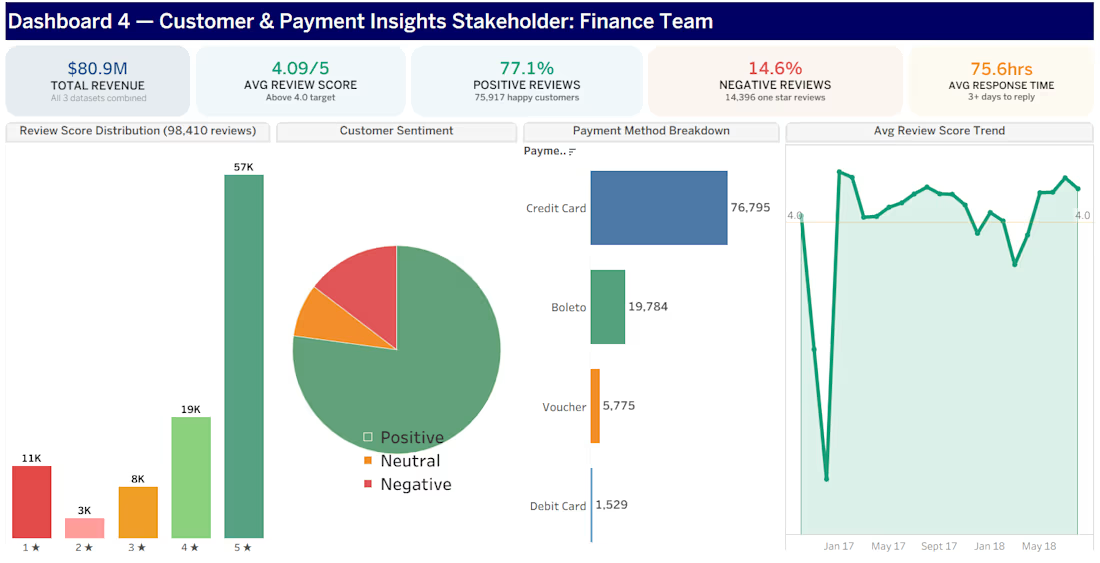

Built a 4-part Power BI dashboard suite analyzing $80M+ in revenue for supply chain & e-commerce data — designed for 4 different stakeholders.

📊 Executive KPI Dashboard (VP of Supply Chain) — Revenue, profit & a 71% revenue drop identified in 2018

🚚 Delivery Performance (Procurement Team) — 54.8% late delivery rate flagged, broken down by shipping class

📦 Product & Warehouse Analysis (Warehouse Ops) — 33K SKUs across 9 warehouses, revenue vs. margin comparison

💳 Customer & Payment Insights (Finance Team) — Sentiment, review scores & payment method breakdown

Tools: Tableau, SQL, Excel, Python

Bank Wallet App | Digital Banking App

Here is my new UI/UX exploration for Digital Banking App design, You Can Buy Only 5$ Digital Banking Wallet App UI Design In Figma.

Need design help? DM

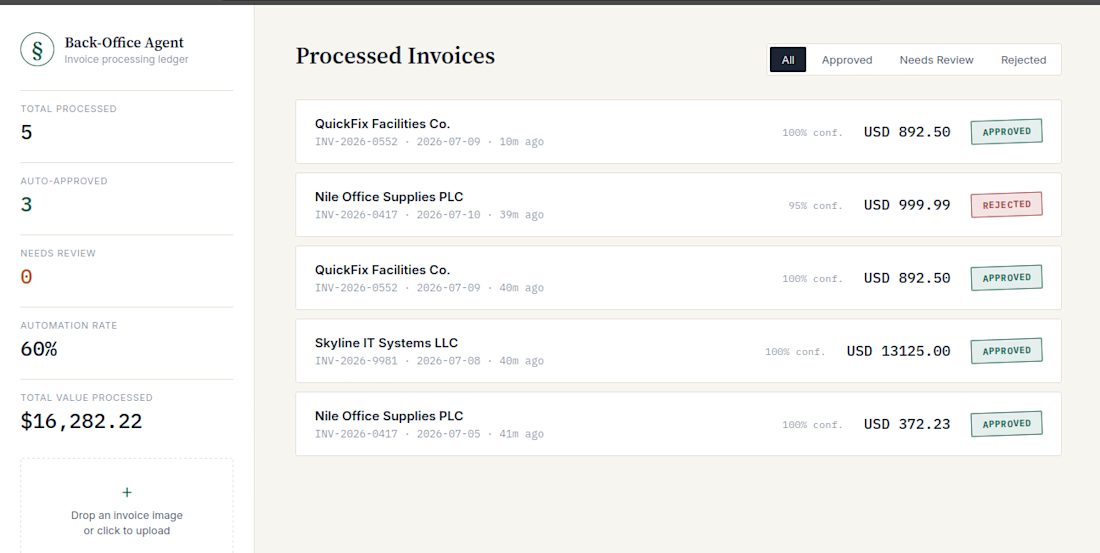

An AI agent that automates invoice processing end-to-end. It reads incoming documents using vision-based OCR, extracts structured data (vendor, amount, date, line items), and checks each one against a vector database to catch duplicate payments before they happen.

Runs on a FastAPI backend that orchestrates the pipeline and writes clean records to a database. Fully tested against real invoice data, and hardened by fixing a credential-exposure issue — moved to a local embedded vector setup for better security and easier deployment.

Result: manual invoice entry replaced with a pipeline that runs unattended and only flags what needs a human.

Challenges

View allTrending

Claude

Claude has entered the design space. How are you using Claude Design?

Contra University

Learn from expert creatives how to earn more using next-gen AI tools.

fifaworldcup2026

The World Cup is here and the whole world's watching. How are you designing for the world stage?

creativeaiflow

Creative AI workflows are evolving. What tools do you use, and what are their strengths and weaknesses?

freelancerlife

Freelancer life is wins, pivots, and everything in between. What’s yours right now?