The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Back to feedPost

💰 Understanding Double-Entry Accounting Through a Conversation

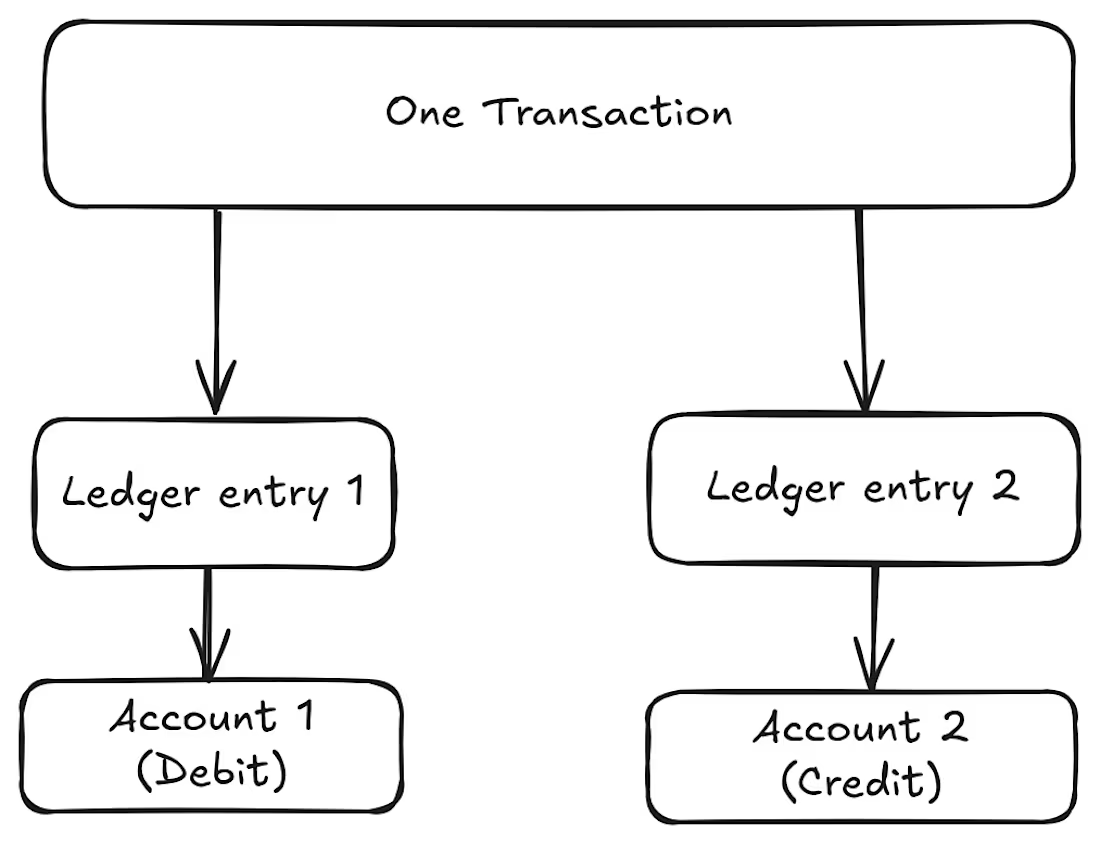

A common misconception is that an account owns transactions.

It doesn't.

An account only owns a copy of the transaction's effect on its balance.

The real owner of the story is the Transaction.

👨💼 Auditor: "Transaction, what happened here? 😳"

🧾 Transaction: "A user deposited some cash."

👨💼 Auditor: "Interesting... but where did the money go? 💸"

🧾 Transaction: "Ledger, can you bring out the entries connected to me? (transaction.entries[])"

📒 Ledger: "Right here."

➕ Entry #1: Credited the user's account.

➖ Entry #2: Debited the source account.

📒 Ledger: "As you can see, every movement has an equal and opposite movement. Everything balances."

👨💼 Auditor: "Perfect! Now I can explain exactly what happened to the administrator. 😊"

🧾 Transaction: "Happy to help, boss."

This is why every financial transaction creates at least two ledger entries:

✅ One entry shows where the money came from.

✅ Another entry shows where the money went.

The Transaction tells the story.

The Ledger provides the evidence.

The Auditor reconstructs the truth.

And because every debit has a matching credit, the books always stay balanced.

📚 That's the beauty of Double-Entry Accounting.

The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Trending

retrofuturism

Share your favorite designs from the past exploring the distant future. Or your own take on the aesthetic 🚀

halftone

Dots. Texture. Grain. Let's see your designs using the halftone technique.

Midjourney

Creatives are showing off what they're making with Midjourney.

colorgrade

Video editors sound off: How do you enhance the mood of your video in color grading?

Related posts

Duvo Studio's first case is up. Fintech feature launch — one card, any bank app, cashback comes with it. Storyboard to final grade, delivered as a full launch set.

Clean launch set. The card visuals feel premium and the motion looks super polished.

Being a freelancer and a business owner makes me think a lot about money, income and how to be more efficient.

Sometimes it’s not about that, life is more than money, it’s about the experiences and people you surround yourself with. And that is worth more than saving a few bucks.

life is more than money, when you have enough money to live.

Title: Market Action Tracker — Real-Time Multi-Timeframe Breakout & Alert Dashboard

Summary:

A live market monitoring dashboard that tracks 20 forex and commodity pairs across multiple timeframes (3min / 5min / 15min) simultaneously, automatically detecting trend state — consolidating vs. breakout — and firing instant alerts the moment structure shifts.

What it does:

Continuously scans price action across each pair and timeframe in parallel, classifying every pair as consolidating or in an active breakout (bullish/bearish) in real time

Live-updating alert feed logs each breakout the instant it triggers — resistance/support breaks, timestamped to the second

Multi-timeframe view surfaces structure shifts as they cascade from short to longer windows, instead of flipping between charts

Auto-refresh with a visible "MARKET LIVE" status and last-updated timestamp, so there's no ambiguity about data freshness

Notification system surfaces new alerts without needing to babysit the screen

Clean, dark-mode trading-desk UI built for fast scanning — color-coded states (green breakout, orange consolidating, red breakdown) so you can read market posture at a glance

Why it matters:

Manually watching 20 pairs across 3 timeframes for structure breaks doesn't scale — this collapses that into a single glanceable view with alerting doing the watching for you, so you only look up when something's actually happening.

This dashboard sounds like a game-changer for traders—how does it handle false breakout alerts?