The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Back to feedPost

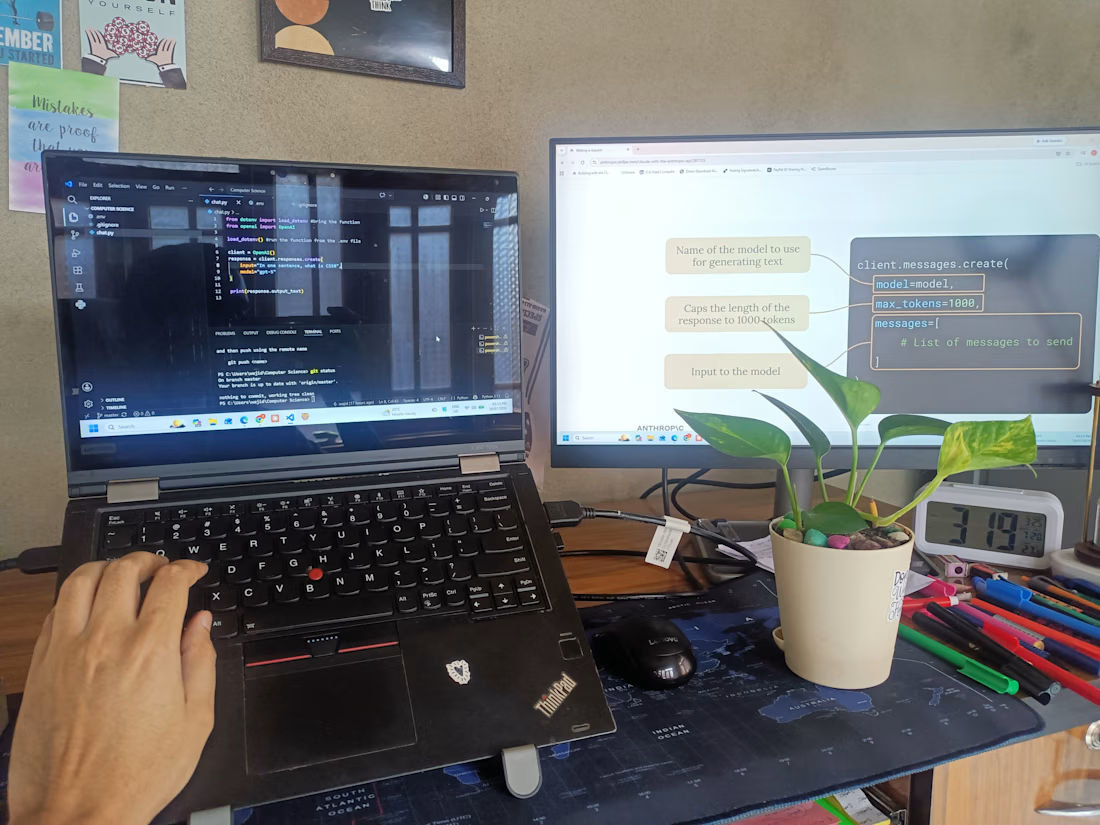

Most retail traders try to predict the market. After building a few production bots on Polymarket, I'm convinced that's the wrong game.

The right game: don't predict — follow. Specifically, follow the market makers.

Why? In high-frequency venues like Polymarket's BTC 5-min markets, MMs aren't betting on direction — they're managing inventory, hedging, and reacting to flow. When their quotes shift, that's information. When order book pressure changes, that's information. Reading those signals and reacting in milliseconds is a different game than picking up vs down.

So I shipped a signal terminal that does exactly that:

🟢 Real-time WebSocket feed from the Polymarket CLOB

🟢 Low-latency signal engine in Go — Python was too slow for the hot path; every millisecond matters when you're trying to enter before the move is priced in

🟢 Confidence tiers and cooldowns (CONFIRMED_NORMAL, CONFIRMED_ACCELERATED) to filter noise

🟢 Live chart with signals overlaid as they fire

Three takeaways from this build:

1) Latency is the strategy. You can have a perfect model — but if you're 200ms late, you're paying the spread to someone who's at 20ms. The choice of language and architecture is the alpha.

2) Stop trying to predict markets. Detect what's already moving and ride it. Inventory pressure beats vibes, every time.

3) For data analysts who've spent 10+ years in Python — the game is changing. Evaluation used to be a "cold" job: batch, offline, after the fact. Today it has to be precise AND on the hot path — accurate in real time. Locking yourself into a Python-only stack stops being smart at that point. Adding Go for the hot path exceeded my expectations — I'm not abandoning Python, but I am rebalancing where it sits in the stack.

Live demo (press DEMO and watch real signals fire against the real order book):

The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Trending

Claude

Claude has entered the design space. How are you using it?

Contra University

Learn from expert creatives how to earn more using next-gen AI tools.

Brand Design

The best brand designers are on Contra. Scroll to see what's trending in brand design. What are you building?

creativeaiflow

Creative AI workflows are evolving. What tools do you use, and what are their strengths and weaknesses?

freelancerlife

Freelancer life is wins, pivots, and everything in between. What’s yours right now?

Related posts

The journey started with pen and paper. I used the same kind of notebook that I use to keep a diary. I had only heard of REST APIs. A little. Like what they were... And slowly, over the next 6 months, I picked up the structural understanding and shipped a consumer intelligence platform.

I am now building an MCP wrapper for Signalwatch. The right internship even pays $20 - $30 per hour. Previously, the highest I earned per hour was $2.2.

It was not earning more dollars that got me on this path. It was a clique that probably played a prank and told me that a person from wher I come from should not handle queries from certain big clients. long story..., and a positive outcome.

It is a lifetime journey now.

Now I want to know what Rest API’s are… I don’t know if it’s related to my field

🤖 Introducing ResumeAI Pro - Built for the #EnvatoChallenge

Theme: Human by Design

AI generates the content, but HUMANS shape the story.

My tool lets you:

✅ Add YOUR real achievements

✅ Choose YOUR tone & style

✅ Make it personal & powerful

Built with:

🐍 Python + FastAPI

🎨 Three.js 3D UI

🤖 OpenAI GPT-4

📄 PDF Export

AI writes the words. Humans tell the story.

#envatochallenge #Python #AI #OpenAI

There is no image!

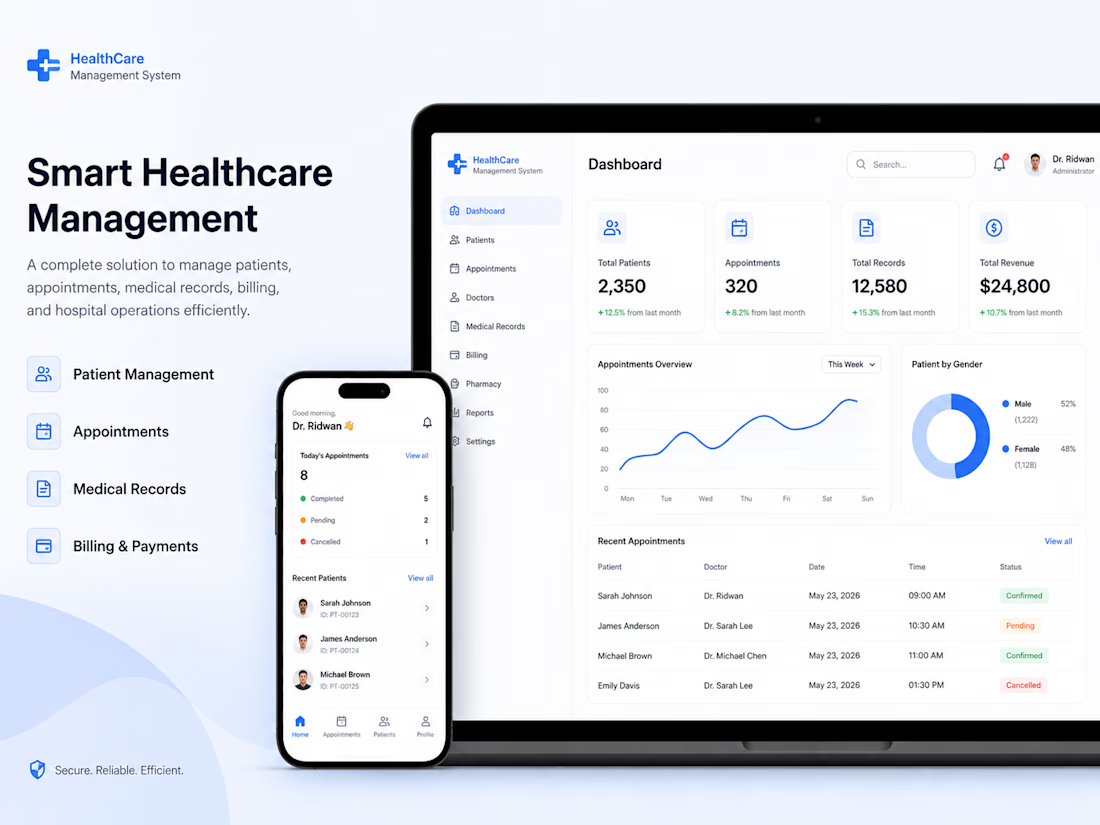

Healthcare Management System

About the Work

I designed and developed a modern Healthcare Management System that streamlines hospital operations, patient management, appointment scheduling, and medical record administration. The platform was built to reduce manual processes, improve communication between healthcare professionals and patients, and provide a secure, user-friendly experience across desktop and mobile devices.

The system combines an intuitive interface with a scalable architecture, enabling healthcare providers to manage day to day operations efficiently while maintaining accurate patient records and improving the overall quality of care.

The Challenge

Many healthcare facilities still rely on disconnected systems, paper based records, and manual administrative processes. These challenges often result in:

Difficulty accessing patient information.

Long appointment scheduling times.

Inefficient communication between departments.

Increased risk of data errors.

Limited reporting and operational insights.

Poor user experience for both patients and healthcare staff.

The goal was to build a centralized digital platform that simplifies healthcare management while ensuring security, scalability, and ease of use.

The Solution

I designed and developed a comprehensive Healthcare Management System that centralizes patient records, appointment scheduling, billing, staff management, and reporting into a single platform.

The solution focuses on usability, performance, and security, allowing healthcare providers to access critical information quickly while reducing administrative workload.

Key features include:

Patient Registration & Profiles

Appointment Scheduling

Electronic Medical Records (EMR)

Doctor & Staff Management

Secure Authentication

Prescription Management

Billing & Payment Tracking

Analytics Dashboard

Responsive Web Interface

Role Based Access Control

How I Solved It

1. Discovery & Research

I analyzed common operational challenges faced by healthcare providers and identified opportunities to improve workflow efficiency, accessibility, and patient management.

2. Product Strategy

I structured the platform around the daily workflow of hospitals and clinics, ensuring that each feature solved a specific operational challenge while remaining simple to use.

3. UI/UX Design

Designed a clean, intuitive interface with a strong emphasis on accessibility, clear navigation, and responsive layouts to support healthcare professionals working across different devices.

4. Full Stack Development

Developed a scalable architecture with secure authentication, optimized database structures, API integrations, and responsive frontend components to ensure reliability and future scalability.

5. Performance Optimization

Optimized loading times, improved database efficiency, enhanced application responsiveness, and implemented best practices for secure healthcare data management.

6. Deployment & Testing

Conducted extensive testing across different devices and user scenarios to ensure stability, security, and a seamless experience before deployment.

Results

The completed Healthcare Management System provides healthcare organizations with a secure, centralized platform that simplifies patient management, improves operational efficiency, reduces administrative workload, and enhances the overall patient experience. The scalable architecture also allows the system to grow alongside the needs of healthcare providers.

My Role

Product Strategy

UI/UX Design

Full Stack Development

Frontend Development

Backend Development

Database Design

API Development

Authentication

Performance Optimization

Deployment

Technologies

React

Next.js

TypeScript

Node.js

Supabase

PostgreSQL

Tailwind CSS

Key Features

Patient Management

Electronic Medical Records (EMR)

Appointment Scheduling

Doctor Dashboard

Billing & Payments

Analytics Dashboard

Role-Based Access

Secure Authentication

Responsive Design

Performance Optimization