The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Back to feedPost

How Foreign Investors Can Legally Minimize U.S. Tax Using Portfolio Interest Exemptions

Cross-border lending is one of the most powerful — and most misunderstood — tools available to foreign investors doing business in the United States. When structured correctly, interest income earned by a non-U.S. lender on a U.S. loan can be completely exempt from federal withholding tax. Achieving this requires meticulous portfolio interest loan documentation to ensure the debt meets all regulatory registration requirements. That exemption, known as the portfolio interest exemption, can mean the difference between a transaction that works and one that quietly erodes returns year after year.

But the benefits don't come automatically. They come from precision — in documentation, in structure, and in legal execution.

What Is the Portfolio Interest Exemption?

Under U.S. tax law, interest paid to a foreign person is generally subject to a 30% withholding tax. That rate can be reduced by a tax treaty, but treaties are not always available or advantageous depending on where the investor is domiciled.The portfolio interest exemption offers an alternative path. When specific legal requirements are met, interest paid on certain debt obligations to foreign lenders is fully exempt from U.S. withholding tax — no treaty required.

To qualify, the loan must meet several criteria:

The debt must be in registered form — meaning it is not payable to bearer and ownership is tracked through a formal registration systemThe lender must be a foreign person — a non-U.S. individual, corporation, or other entity not treated as a U.S. tax residentThe lender must not own 10% or more of the borrower's voting stock — this is a critical threshold that disqualifies related-party arrangementsThe interest must not be contingent on the borrower's income or profits — so-called "contingent interest" breaks the exemptionProper certification must be provided — the lender must certify its foreign status, typically using IRS Form W-8BEN or W-8BEN-EWhen all of these boxes are checked, the withholding obligation disappears entirely. The lender receives the full interest payment, and the borrower avoids the administrative burden of withholding and remitting tax to the IRS.

Why Documentation Is Everything

The portfolio interest exemption is not self-executing. It requires a deliberate documentation framework that begins before the first dollar changes hands and must be maintained throughout the life of the loan.

Proper portfolio interest loan documentation typically includes:

A loan agreement or promissory note that explicitly reflects the registered form of the debtA bondholder registry or equivalent tracking mechanism to evidence registered ownershipIRS Form W-8BEN or W-8BEN-E, properly completed and signed by the lender before the first payment is madeA certification of foreign status that must be updated when circumstances change or upon the IRS's requestWire transfer records and payment schedules that correspond cleanly to the documented loan terms

Legal opinions, where appropriate, confirming that the transaction qualifies for the exemption

Missing or improperly completed documentation doesn't just create administrative headaches — it can expose the borrower to full 30% withholding liability, plus penalties and interest, for every payment made during the gap. The IRS has consistently held that the exemption is only as valid as the paperwork supporting it.

Structuring the Transaction: Where Legal Strategy Becomes Critical

Beyond the documents themselves lies the more complex work of transaction structuring. The 10% ownership rule, the contingent interest prohibition, and the registered form requirement each introduce potential traps for the unwary.

For example, a foreign investor who holds equity in the borrowing entity — common in venture or real estate deals — may inadvertently disqualify the interest from the exemption if their stake approaches the 10% threshold. In family office or related-party lending situations, attribution rules can further complicate the analysis.Contingent interest provisions, such as profit participations, equity kickers, or interest tied to revenue milestones, can poison an otherwise qualifying loan. Identifying and separating these elements before closing is essential.This is where an experienced portfolio interest structuring lawyer becomes not a luxury but a necessity. The goal is not simply to draft documents — it is to design a transaction architecture that achieves the client's economic objectives while surviving IRS scrutiny.

Working With Leticia Balcazar

At Leticia Balcazar, we work with foreign investors, family offices, private lenders, and their U.S. counterparts to structure cross-border lending transactions that are legally sound, tax-efficient, and built to last.Our practice focuses on international tax planning and transactional law, with deep experience in exemption qualification, treaty analysis, and the kind of meticulous documentation frameworks that protect clients long after a deal closes.Whether you are entering your first U.S. cross-border loan or restructuring an existing lending arrangement that may not be optimally positioned, we provide clear, strategic counsel tailored to your specific situation.

The portfolio interest exemption is one of the most valuable tools in international tax planning. Used correctly, it opens significant opportunities. Used carelessly, it creates significant risk.

The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Related posts

Navigating Global Wealth: Why Specialized Counsel Matters

Cross-border investments and international business expansion bring immense opportunity—but they also bring complex regulatory traps. From managing FBAR filings to structuring offshore assets, the difference between a successful venture and a costly audit often comes down to the expertise of an International Tax Attorney.

Relying on general tax advice can lead to missed exemptions or inadvertent non-compliance with evolving global standards. A specialist ensures your wealth is protected, your structures are optimized for tax efficiency, and your peace of mind remains intact across every border you cross.

For strategic guidance and sophisticated tax solutions tailored to your unique global footprint, consult with Leticia Balcazar.

Portfolio Refining Era: Big changes coming this June. ✨

Starting next month, I am officially transitioning to partial freelancing! YAY!!

To get ready for the launch, I’ve been deep in my portfolio refining era 🧠

Before I open the doors for new projects, I’d love to get some fresh eyes on it.

Drop your honest feedback or just say hi below! Check out the live link here:

https://idrequestlab.framer.website/

Great job 👏

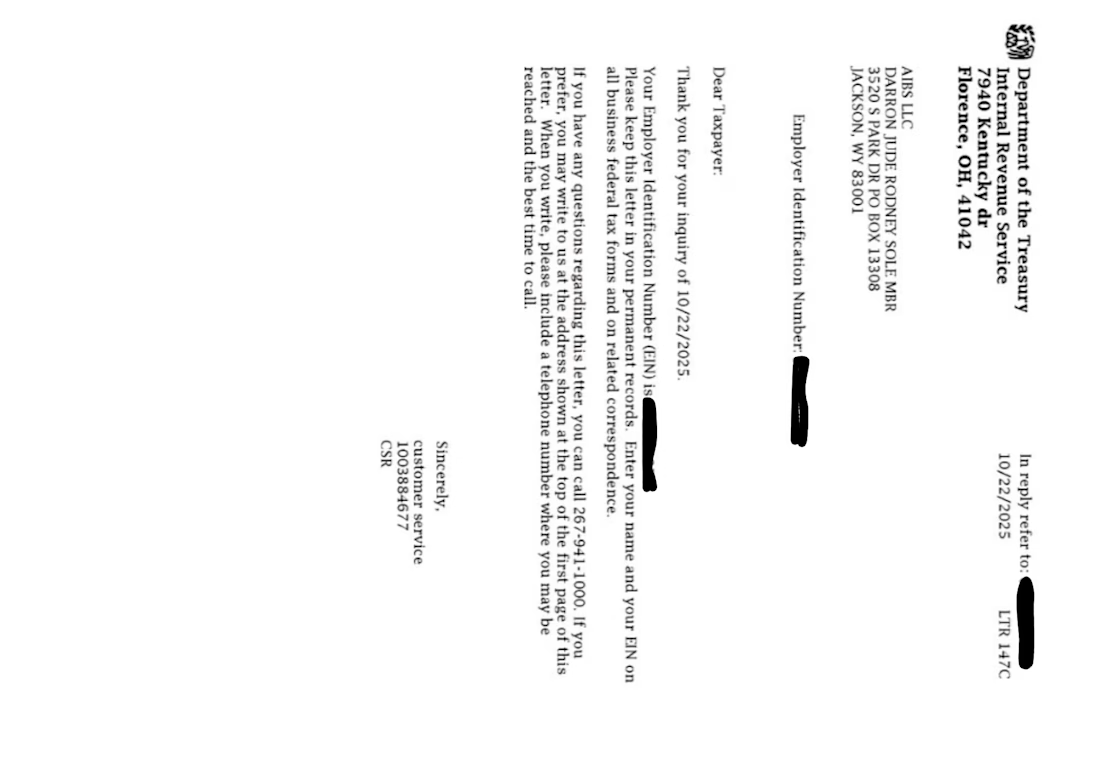

I assisted the client in successfully obtaining an Employer Identification Number (EIN) for AIBS LLC, ensuring the business met all federal tax registration requirements in the United States.

The project involved preparing and submitting the EIN application with the Internal Revenue Service while ensuring the accuracy of the company’s legal and responsible party information. I guided the client through the process and ensured the application complied with IRS regulations to avoid delays or rejection.

After submission, the EIN was successfully issued, allowing AIBS LLC to establish its federal tax identity. This enables the business to open a U.S. business bank account, process payments, hire employees if needed, and comply with federal tax reporting requirements.

This project highlights my experience in U.S. business compliance, EIN registration, and tax identification services for startups and international entrepreneurs.

Trending

Claude

Claude has entered the design space. How are you using Claude Design?

Contra University

Learn from expert creatives how to earn more using next-gen AI tools.

creativeaiflow

Creative AI workflows are evolving. What tools do you use, and what are their strengths and weaknesses?

portfolioreview

The best portfolios tell a story, not just show a grid. Share yours for feedback.

freelancerlife

Freelancer life is wins, pivots, and everything in between. What’s yours right now?