The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Back to feedPost

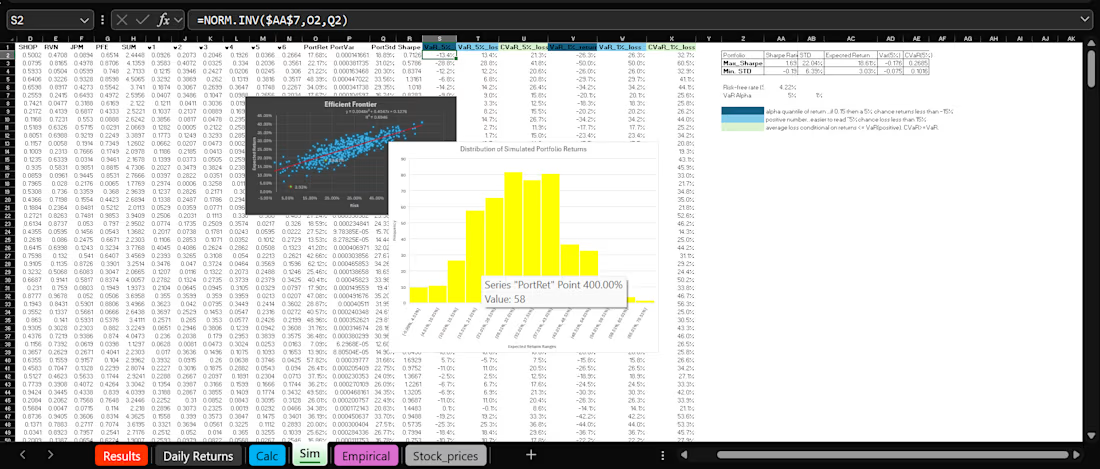

Portfolio Optimization: Maximizing Sharpe Ratio using Monte Carlo Simulation and Solver

Just wrapped a rigorous asset allocation model for a portfolio of six stocks using Monte Carlo Simulation and solver.

Problem Statement: How to find the most efficient allocation for an institutional-grade portfolio.

Solution: Identified the Max-Sharpe Portfolio with an Expected Annual Return of 25.95% and Volatility of 16.90% (Sharpe 1.29) using Monte Carlo Simulation.

Need a data-driven strategy for wealth management or asset allocation? Let's build your next optimal portfolio.

The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Trending

Claude

Claude has entered the design space. How are you using Claude Design?

Contra University

Learn from expert creatives how to earn more using next-gen AI tools.

creativeaiflow

Creative AI workflows are evolving. What tools do you use, and what are their strengths and weaknesses?

freelancerlife

Freelancer life is wins, pivots, and everything in between. What’s yours right now?