The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Back to feedPost

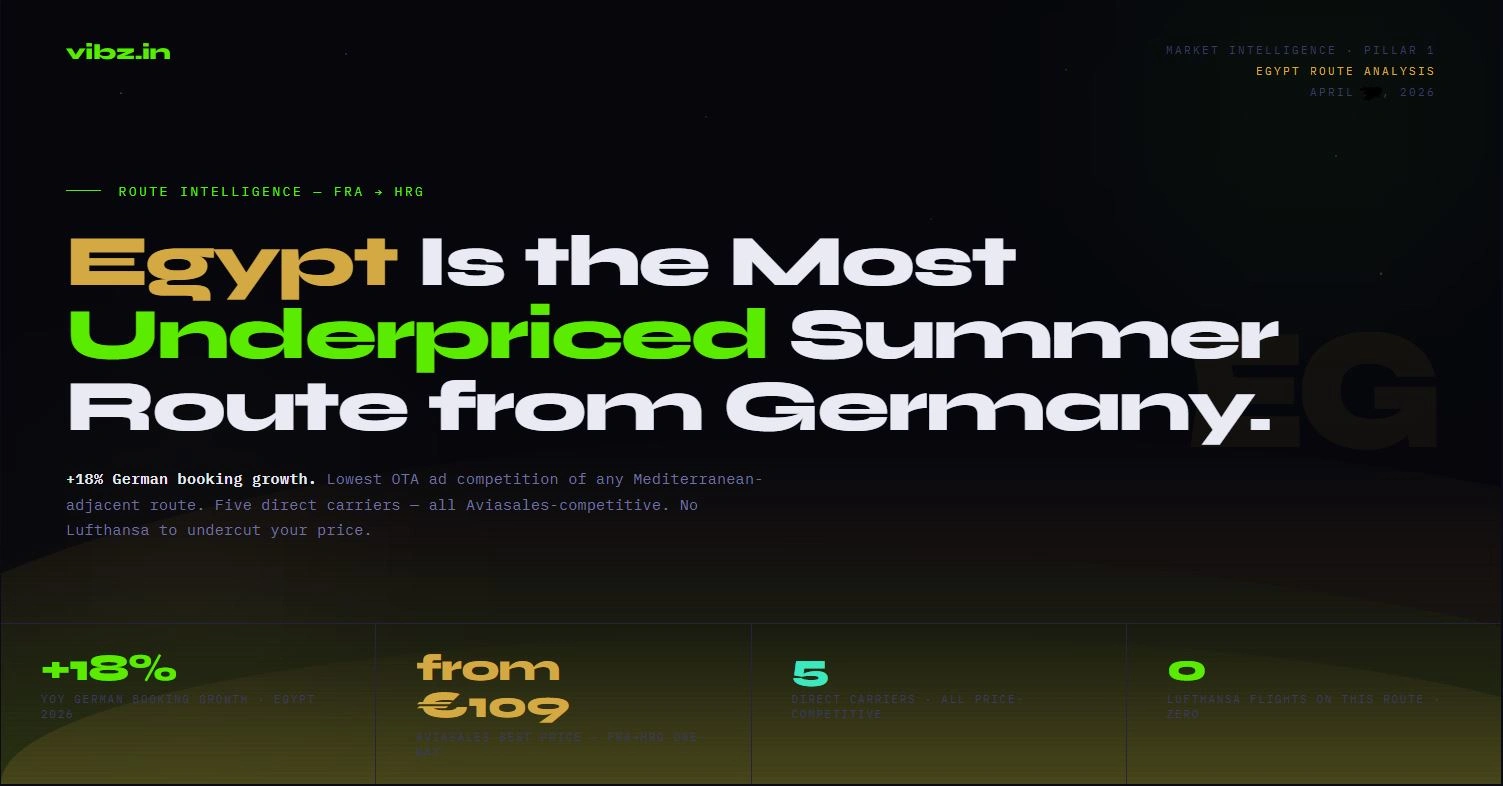

German bookings to Egypt are up 18% year-on-year in 2026.

That's the largest growth number of any destination in our active tracking set — ahead of Turkey (+22% in raw bookings but far more crowded on the advertising side), ahead of Greece (+8%), and more than three times the growth rate of Spain (+5%).

And yet: FRA→HRG has the lowest OTA ad competition of any route we monitor from Germany.

That gap — between demand momentum and advertising pressure — is exactly where the margin lives.

This post explains how we found it,what the pricing data shows, and why the absence of Lufthansa on this route creates a clean price field that doesn't exist anywhere else in the German summer portfolio.

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

THE PRICING DATA: FRA → HRG

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

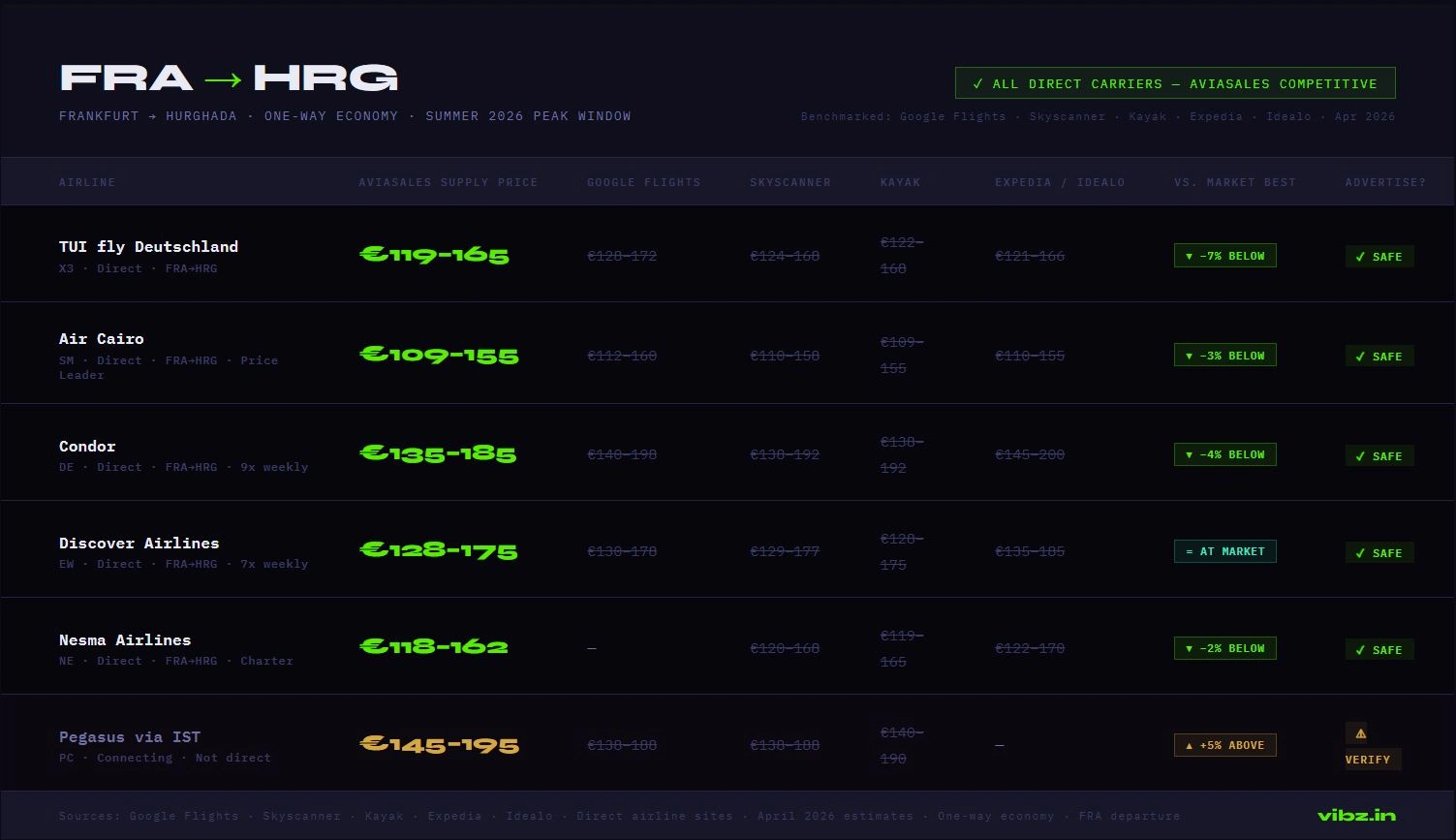

We benchmark every route we advertise against five market sources:

Google Flights, Skyscanner, Kayak, Expedia, and Idealo (the most used German-language price comparison platform).

Here is what the FRA→HRG market looks like right now for summer

2026 departures:

▸ TUI fly: Market average €128–172 OW · Aviasales supply: €119–165

▸ Air Cairo: Market average €112–160 OW · Aviasales supply: €109–155

▸ Condor: Market average €140–198 OW · Aviasales supply: €135–185

▸ Discover Airlines: Market average €130–178 OW · Aviasales supply: €128–175

Every single direct carrier on this route is at or below market through Aviasales aggregation.

That is not the norm.

On FRA→PMI (Mallorca), Condor's Aviasales-supplied price runs 8–20% above Skyscanner on peak summer dates.

On FRA→HER (Heraklion), Lufthansa's direct site undercuts Aviasales by 10–20%, making the airline entirely unadvertisable. On FRA→AYT (Antalya), you get one window of Freebird/Pegasus advantage and then a patchwork of carrier-specific risks to manage.

FRA→HRG has none of those problems.

Five direct carriers.

Clean Aviasales pricing across all five.

No dominant network carrier to undercut you.

No flash-sale chaos from a legacy brand with a German loyalty programme.

This is a structurally simple route to advertise, which is a rarer thing than it sounds.

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

WHY LUFTHANSA'S ABSENCE MATTERS

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

Most high-value routes from Germany have a Lufthansa problem.

German travellers are meaningfully brand-loyal to Lufthansa in a way that doesn't have a clean equivalent in other European markets.

When an ad shows a Lufthansa price, a significant proportion of German users will open lufthansa.com in a second tab to verify it.

If the direct site is cheaper — which it often is, because Lufthansa optimises its direct channel aggressively — the trust relationship with the OTA breaks.

This is why we suppress Lufthansa on FRA→HER (Heraklion), on FRA→TYO (Tokyo), on FRA→NYC, and on FRA→SIN (Singapore).

In each case, the Aviasales-supplied Lufthansa price sits above what lufthansa.com shows for the same route.

On FRA→HRG, Lufthansa doesn't operate direct service.

The route is served exclusively by charter and leisure carriers:

TUI fly, Condor, Discover Airlines, Air Cairo, and Nesma Airlines.

None of these carriers has built the kind of direct-channel loyalty infrastructure that Lufthansa has. None of them is named a German traveller, who reflexively cross-references on a separate tab.

The result is a price field where your advertised fare is accepted at face value.

That acceptance rate translates directly into click quality, conversion rate, and — critically — the trust relationship that drives return bookings.

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

THE RED SEA CHARTER MARKET: WHAT THE DATA SHOWS

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

Hurghada is not a GDS-dominant market.

It never was.

The Red Sea charter economy — Hurghada, Sharm el-Sheikh, and Marsa Alam — developed primarily through direct airline-to-tour-operator contracting rather than through the global distribution system.

TUI fly and Condor operate contracted charter blocks to HRG that predate modern OTA infrastructure.

Air Cairo and Nesma operate as hybrid charters with limited but growing GDS presence.

What this means in practice:

▸ Seat inventory is less exposed to last-minute direct price manipulation than on fully GDS-distributed routes

▸ Published fares from Aviasales track closely with contracted block pricing — less variance between aggregated and actual cost

▸ Price feed staleness risk is materially lower than on Mediterranean peak routes (Mallorca, Ibiza, Santorini)

▸ Overbooking-driven repricing events, which create sudden Skyscanner/Kayak drops that undercut advertised OTA prices, are less frequent on charter-block routes

From an operational standpoint, FRA→HRG is one of the cleanest routes to maintain price parity between ad creative and actual booking price.

Price feed refresh at 8–12 hour intervals is adequate for most of the calendar year, versus the 3–4 hour refresh requirement we maintain on FRA→PMI peak-summer inventory.

This is not a coincidence.

It is a structural feature of how the Red Sea charter market was built, and it favours OTAs who understand the market mechanics over those who don't.

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

THE DEMAND CONTEXT

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

The +18% figure comes from DRV (Deutscher Reiseverband) and TDA Travel Data Analytics early-booking data, cross-referenced with ITB Berlin 2026 market intelligence on German outbound travel.

Egypt's growth is above-average relative to every Mediterranean competitor tracked.

The drivers are familiar:

▸ Egyptian pound weakness relative to the euro makes on-the-ground costs significantly cheaper than equivalent beach-resort alternatives in Turkey or Greece

▸ Hurghada's all-inclusive resort model delivers predictable cost certainty that appeals to German price-sensitive families

▸ Red Sea water temperatures remain viable for diving and water sports later into autumn than most Mediterranean alternatives — extending the viable booking window into September and October

▸ Hamburg Airport is adding Corendon Airlines service to Hurghada from May 2026, increasing capacity and search volume from northern Germany

The Hamburg Corendon addition is particularly notable for OTA campaign planning.

New route launches consistently produce a search volume spike of 4–8 weeks around the first flight — a window where intent is high, and supply advertising has not yet saturated.

This creates a specific opportunity to capture Hamburg-origin traffic on FRA→HRG feeder-and-fly searches.

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

THE ADVERTISING OPPORTUNITY

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

We allocate 25% of our Germany Q2–Q3 long-haul campaign budget to FRA→HRG — the second-largest allocation after FRA→AYT (Turkey).

The reasoning is straightforward:

▸ Demand is growing faster than competing OTAs are entering the space.

This is the definition of an early-mover window.

▸ Aviasales pricing is structurally advantaged on all five direct carriers, eliminating the airline-by-airline suppression analysis required on more complex routes.

▸ The cost-per-click on "Flug Hurghada" and "Ägypten Flug" German-language keywords is materially lower than equivalent intent keywords for Turkey, Greece, or Spain — because fewer OTAs are bidding on them.

▸ Average ticket value is €220–300 OW in summer, yielding meaningful absolute margin even at modest percentage markup.

▸ The route's seasonal demand peak (November–April for beach tourism) means summer campaigns can simultaneously acquire customers for Q4 bookings — a compounding return structure that doesn't exist on pure summer-seasonal routes.

The practical question we ask before allocating to any route is:

Can we advertise these prices confidently, without risk of the user finding cheaper on click-through?

On FRA→HRG, for every direct carrier currently active, the answer is yes.

That is a short list.

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

THE ONE WATCH ITEM

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

Pegasus Airlines (via Istanbul) occasionally appears in Kayak and Skyscanner results for FRA→HRG at prices slightly below Aviasales supply for direct service.

This is a connecting-flight offering, not a direct route — but German travelers in price-comparison mode may not distinguish between direct and connecting clearly enough.

Our current practice: exclude Pegasus from FRA→HRG ad creative until per-flight price verification confirms parity.

For direct carriers only, the route is clean.

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

IF YOU'RE RUNNING GERMAN TRAVEL CAMPAIGNS

▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬▬

The routes with the loudest demand signals in Germany right now —Turkey, Mallorca, Greece — are also the routes with the highest OTA advertising competition, the most complex carrier suppression requirements, and the most volatile peak-summer pricing.

Egypt doesn't have that profile yet.

The demand is real. The pricing is clean. The competition window is open.

That window will close as more OTAs run the same analysis we've run here.

The question is whether your campaigns are in the market before that happens or after.

We're already in.

The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Related posts

Travel discovery should feel like finding a place with a story, not scrolling through a list of rooms.

For Aloft, we explored a hospitality app for experienced travelers looking for eco-retreats, boutique hotels, and destinations with real character.

The interface uses refined dark surfaces, editorial typography, immersive photography, and subtle accents to create a calm, considered travel experience built around atmosphere and discovery.

What matters more to you when choosing a stay: the place itself or the story it lets you step into?

View the full project:

https://dribbble.com/shots/27564095-Aloft-Hotel-Booking-App

Static ad designs for Booking.

I built an automated German AI publication with Astro — here are the early results

Over the past few months, I’ve been working on a German-language publication focused on artificial intelligence, large language models, AI software, technical explanations, and industry developments.

The project is built with

Astro and supported by a largely automated content and publishing workflow.

I wanted to share some of the early performance data because the differences between Google Search, Bing, and AI-powered search have been especially interesting.

Google Search Console

Across the analyzed period, the website generated:

-109 organic clicks

-20,233 Google Search impressions

-an average CTR of approximately 0.54%

The monthly development looked like this:

February: 7 clicks and 399 impressions

March: 12 clicks and 1,662 impressions

April: 16 clicks and 2,088 impressions

May: 18 clicks and 4,039 impressions

June: 41 clicks and 9,151 impressions

July, partial month: 15 clicks and 2,894 impressions

The most encouraging signal is the growth in visibility.

Google impressions increased from 399 in February to 9,151 in June, which represents growth of more than 22 times within a few months.

Clicks also increased from 7 in February to 41 in June.

The CTR is still relatively low, but this appears to be mainly connected to ranking positions. Many pages are currently receiving impressions while ranking outside the top results, often between the lower first page and the following pages.

That means the next major opportunity is not simply publishing more content. It is improving how existing pages perform.

The most important areas are currently:

-titles and search snippets

-internal linking

-search-intent alignment

-topical authority

-content differentiation

-ranking positions

-click-through rate

Bing organic search

Bing generated:

-39 clicks

-2,347 impressions

-an average CTR of approximately 1.66%

Bing currently provides much less total visibility than Google, but the click-through rate is noticeably higher.

Google offers the larger traffic opportunity, while Bing already appears to send comparatively qualified visitors from a smaller number of impressions.

Microsoft Copilot and Bing AI citations

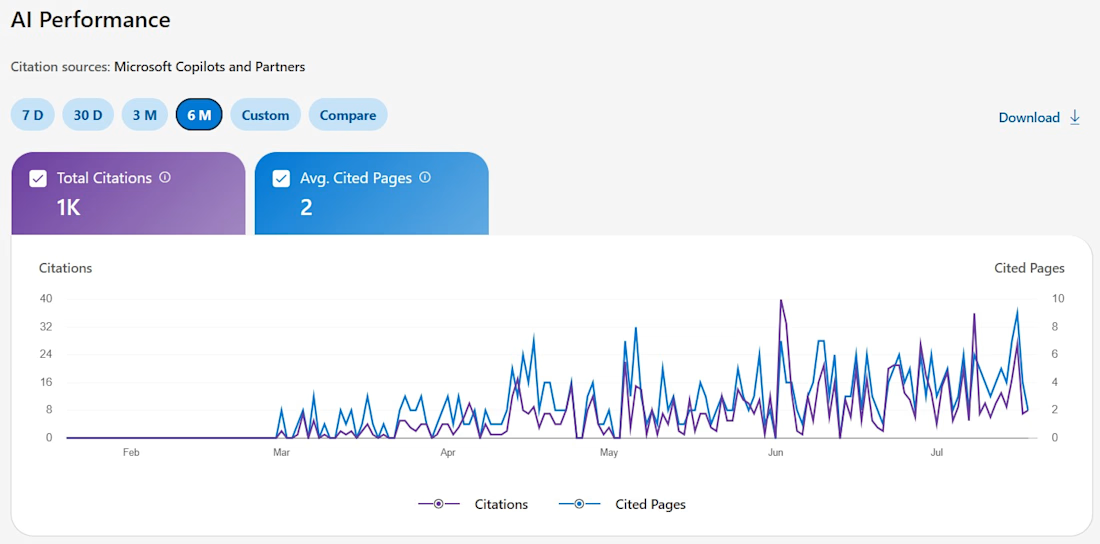

The most surprising part of the experiment has been the performance in Bing AI and Microsoft Copilot.

AI citations developed as follows:

March: 57 citations

April: 165 citations

May: 212 citations

June: 384 citations

July, partial month: 113 citations

The number of pages cited by Bing AI also increased:

March: 36 cited pages

April: 72 cited pages

May: 82 cited pages

June: 115 cited pages

By June, content from more than 100 pages had already been used as a source by Microsoft’s AI systems.

This is especially interesting because some pages appear to receive AI citations before they achieve strong positions in traditional search.

That suggests AI visibility may develop on a different timeline from classic organic rankings.

Several individual pages also accumulated dozens or even hundreds of citations, particularly content with a strong practical or educational angle.

The formats that currently appear to perform best include:

-tutorials

-technical explanations

-glossary-style content

-implementation guides

-comparison-focused content

-practical problem-solving articles

I am intentionally not sharing the exact topic clusters yet, as part of the project is still experimental.

The “Crawled — currently not indexed” category is the main area I am monitoring. These pages may need more time, stronger internal links, clearer differentiation, or better alignment with search demand.

The 404 pages also need to be reviewed individually to ensure that removed URLs are handled correctly and are no longer referenced internally or included in the sitemap.

Lighthouse and technical performance

The Lighthouse results were:

Performance: 98

Accessibility: 93

Best Practices: 100

SEO: 100

The measured performance metrics included:

First Contentful Paint: 1.2 seconds

Largest Contentful Paint: 1.5 seconds

Total Blocking Time: 0 milliseconds

Cumulative Layout Shift: 0

Speed Index: 4.0 seconds

Astro has been a very strong fit for this type of content platform.

The combination of static rendering, lightweight pages, and limited client-side JavaScript provides an excellent technical foundation.

At this point, site speed is not the main bottleneck. The more important challenges are authority, rankings, CTR, content quality, and distribution.

What I have learned so far

The biggest lesson is that content volume alone is not enough.

A scalable publishing system can create a large number of pages, but that does not automatically lead to traffic.

The real work starts after publication.

Another important observation is that traditional search and AI search do not behave in exactly the same way.

Google appears to test many pages gradually before giving them stronger visibility.

Microsoft Copilot, by contrast, has already cited a surprisingly broad selection of content.

This may indicate that AI search visibility can emerge earlier than meaningful organic traffic.

The project is still early, but the direction is encouraging.

The strongest signals so far are:

Google impressions increased more than 22 times from February to June

Google clicks increased from 7 to 41 per month

Bing organic CTR reached approximately 1.66%

Bing AI citations increased from 57 in March to 384 in June

the number of pages cited by Bing AI increased from 36 to 115

several individual pages accumulated a high number of AI citations

Lighthouse Performance reached 98

SEO and Best Practices both reached 100

the technical foundation remains fast despite the growing amount of content

The main question now is whether growing visibility and AI citations will translate into stronger rankings, more clicks, and sustainable revenue over the coming months.

Would you like to see more insights into Astro, SEO, automated publishing, and AI search visibility?

Follow me for future updates.

You can also find high-quality Astro themes here:

Trending

Claude

Claude has entered the design space. How are you using Claude Design?

Contra University

Learn from expert creatives how to earn more using next-gen AI tools.

creativeaiflow

Creative AI workflows are evolving. What tools do you use, and what are their strengths and weaknesses?

freelancerlife

Freelancer life is wins, pivots, and everything in between. What’s yours right now?