The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Back to feedPost

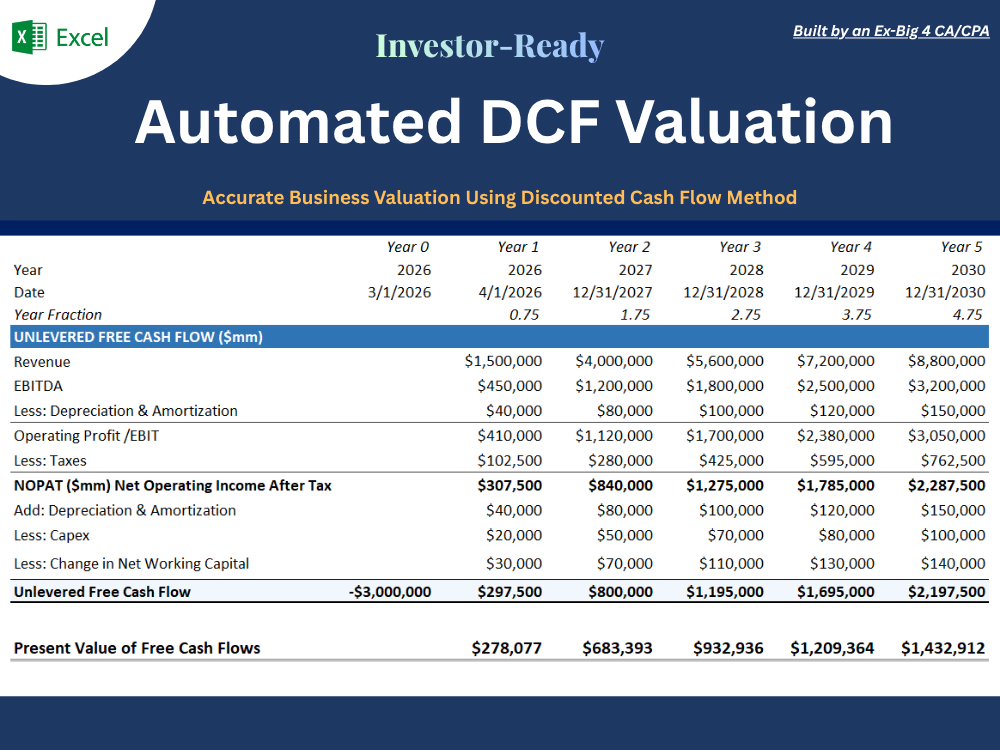

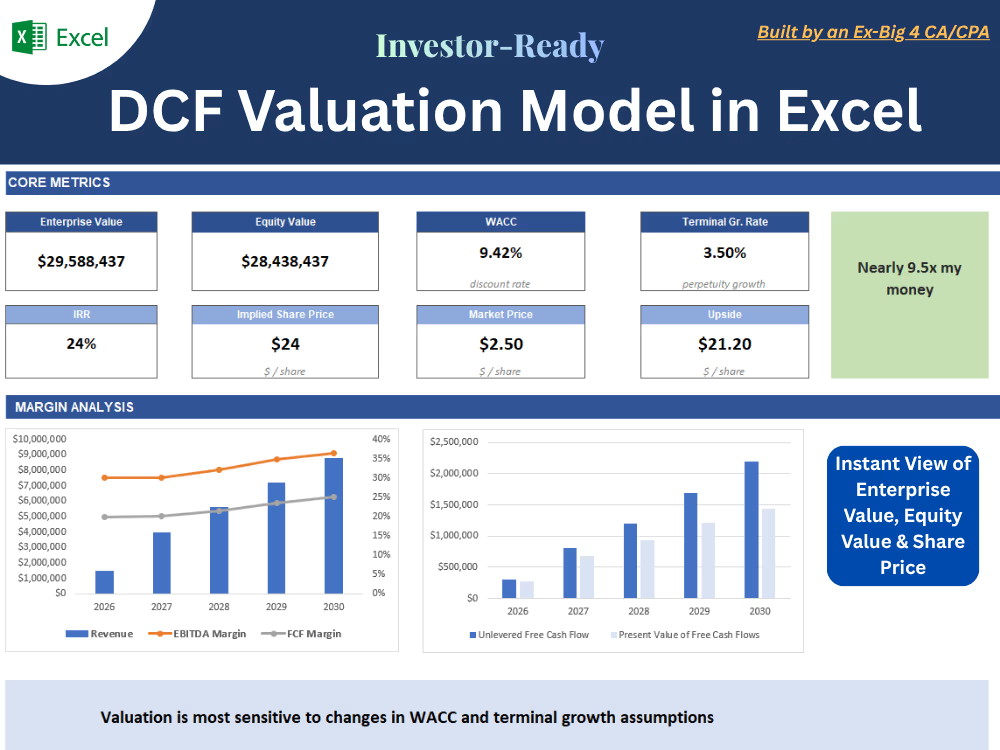

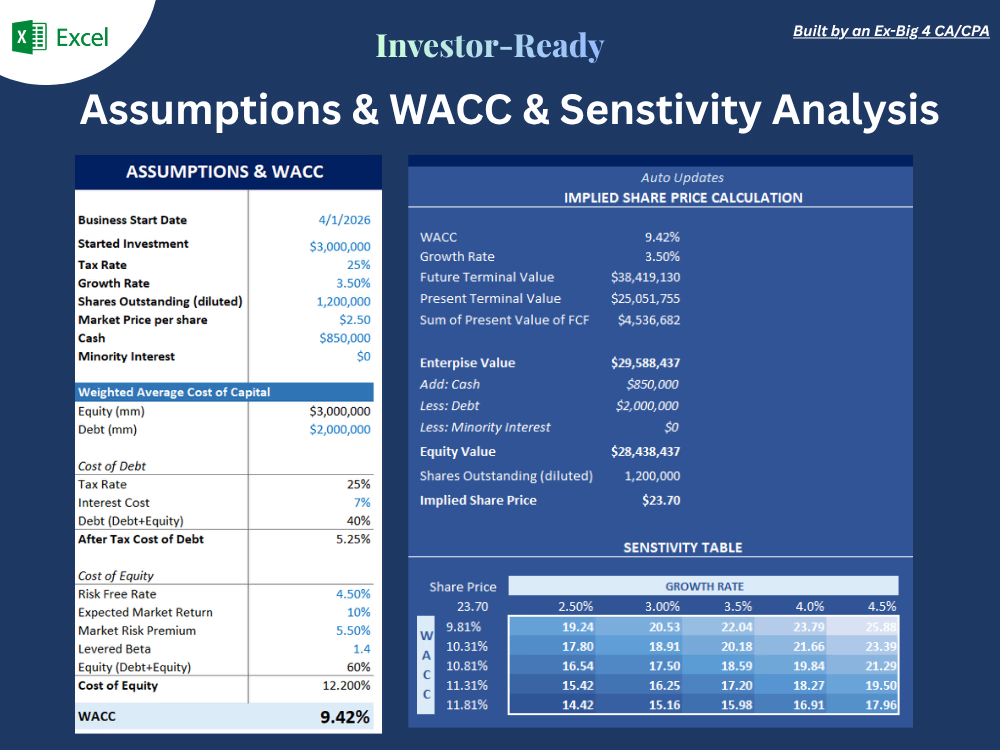

Built a 5-year DCF valuation model for a revenue-generating B2B company preparing for a seed round. Deliverables included Unlevered Free Cash Flow projections, WACC calculation (cost of equity via CAPM, after-tax cost of debt), terminal value, implied share price, XIRR-based investor IRR, and a sensitivity table across WACC and growth rate scenarios. Final dashboard surfaced EV, Equity Value, IRR, and investor return multiple. Model designed to withstand investor diligence scrutiny. (Numbers used are hypothetical)

The network for creativity

Join 1.25M professional creatives like you

Connect with clients, get discovered, and run your business 100% commission-free

Creatives on Contra have earned over $150M and we are just getting started

Related posts

A modern fintech SaaS landing page

designed to simplify payments, automate

savings, and improve cash flow management.

This design focuses on creating a clean and

intuitive user experience while maintaining a strong

visual hierarchy and conversion-driven layout.

The goal was to make financial tools feel simple, fast, and accessible for modern businesses.

Key highlights include a bold hero section,

structured feature blocks, data visualization, and

a clear call-to-action strategy to guide users effortlessly

through the product.

Ideal for fintech startups, payment platforms,

and SaaS products looking to improve usability and

user trust through design.

Headline: 🚀 My Technical Portfolio is officially LIVE on Contra!

I’m excited to share that I’m officially open for new remote opportunities as a Technical Project Manager.

I specialize in bridging the gap between complex engineering and business operations. Whether it's optimizing Odoo ERP workflows or architecting automated SQL databases using Python, I focus on building systems that actually scale.

🛠 Check out my featured projects:

Odoo Kanban Logic Optimization

Relational Database Automation (ETL Pipeline)

I’m looking to partner with forward-thinking teams on AI and data-driven projects. Let’s build something efficient together!

View my full profile & services here: [https://contra.com/noor_fatima_princess_6nc5bks0?referralExperimentNid=DEFAULT_REFERRAL_PROGRAM&referrerUsername=noor_fatima_princess_6nc5bks0 ]

#TechnicalProjectManager #RemoteWork #Python #SQL #Odoo #AI #FreelanceLife

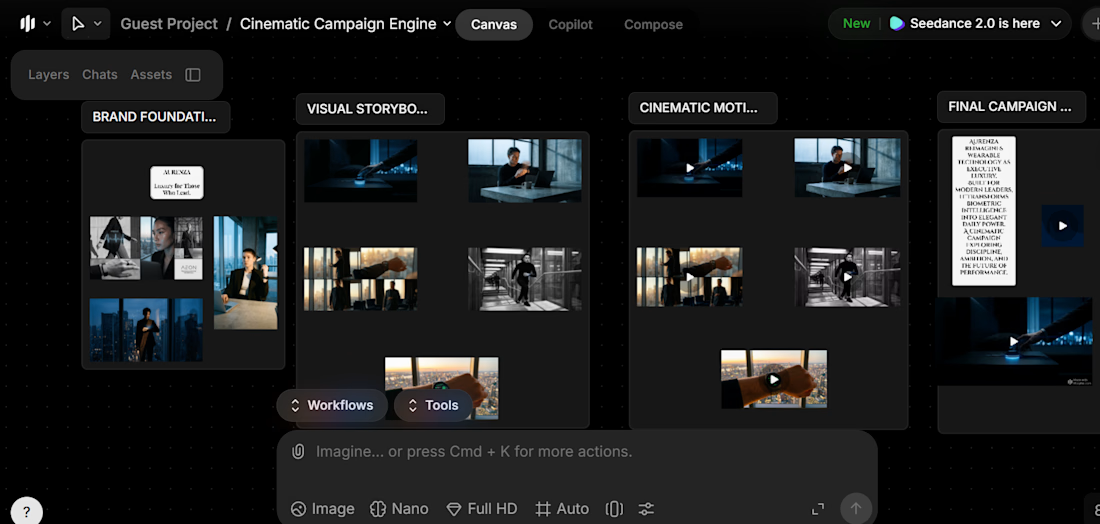

Workflow Title: Workflow Title: Concept to Commercial AI Engine

Description:

Concept to Commercial AI Engine is a 4-step premium Morphic workflow that transforms a raw product or brand idea into a broadcast-ready cinematic campaign.

Built for founders, marketers, agencies, and creators, the workflow combines strategy + visuals + motion + final film production in one streamlined system.

The workflow process:

Brand Foundation :

Generates brand DNA, audience positioning, emotional core, moodboard, and archetype visuals.

Visual Storyboard :

Creates campaign concept, messaging, and a connected 5-scene luxury storyboard.

Cinematic Motion System :

Animates scenes into polished motion sequences using cinematic transitions, pacing, and camera movement.

Final Campaign Film :

Adds score, voiceover, sound design, and final ad-film direction for a launch-ready commercial.

This workflow solves a real problem: turning early-stage ideas into premium campaign assets quickly without needing a full creative team.

I tested it using a luxury wearable-tech concept called Aurenza, producing a complete high-end campaign from one input.

Try it with your own brand idea and see it become a full campaign world.

Social Links:

LinkedIn:https://shorturl.at/vX3S8

X: https://rb.gy/hua47d

Trending

Runway

AI video generation is exploding. What are you dreaming up in Runway?

Contra University

Learn from expert creatives how to earn more using next-gen AI tools.

creativeaiflow

Creative AI workflows are evolving. What tools do you use, and what are their strengths and weaknesses?

portfolioreview

The best portfolios tell a story, not just show a grid. Share yours for feedback.

freelancerlife

Freelancer life is wins, pivots, and everything in between. What’s yours right now?